- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 5 of 13

Contributed By:

The following is a summary of a video recording and may contain errors in spelling or grammar. Although IBKR has edited for clarity no material changes have been made.

Hi, my name is Jozef Soja. I’m a Research Analyst on the Next Generation Internet team here at ARK Invest. And today we’re going to be going through the AI productivity section of Big Ideas 2026.

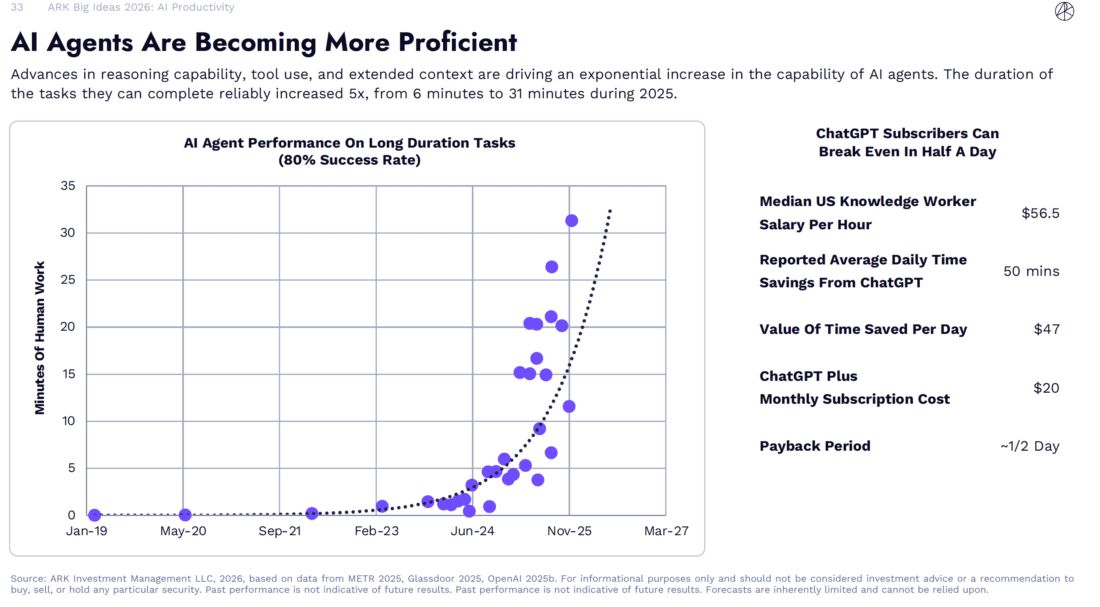

2025 was the year that chatbots began to mature into AI agents with reasoning models becoming much more performant and developers building more comprehensive tools and frameworks on top of these models. At the beginning of 2025, AI agents could only reliably perform tasks that would take a human 5 to six to complete. By the end of the year, agents could complete tasks that would take a human over 30 to complete on their own. This reflects a significant increase in the value workers are getting out of AI, while the price of these subscriptions to AI services have largely stayed consistent.

For example, after discounting for an 80% success rate on tasks, a study from OpenAI suggests that the average knowledge worker using ChatGPT saves about 50 min per day. At an average US knowledge worker salary of $56 per hour, ChatGPT on average produces $47 per day of value. At a cost of $20 per month, ChatGPT effectively pays for itself after about half a day of use. As top performing models push the frontier of what AI can do, the price for the best of the best has stayed relatively stable.

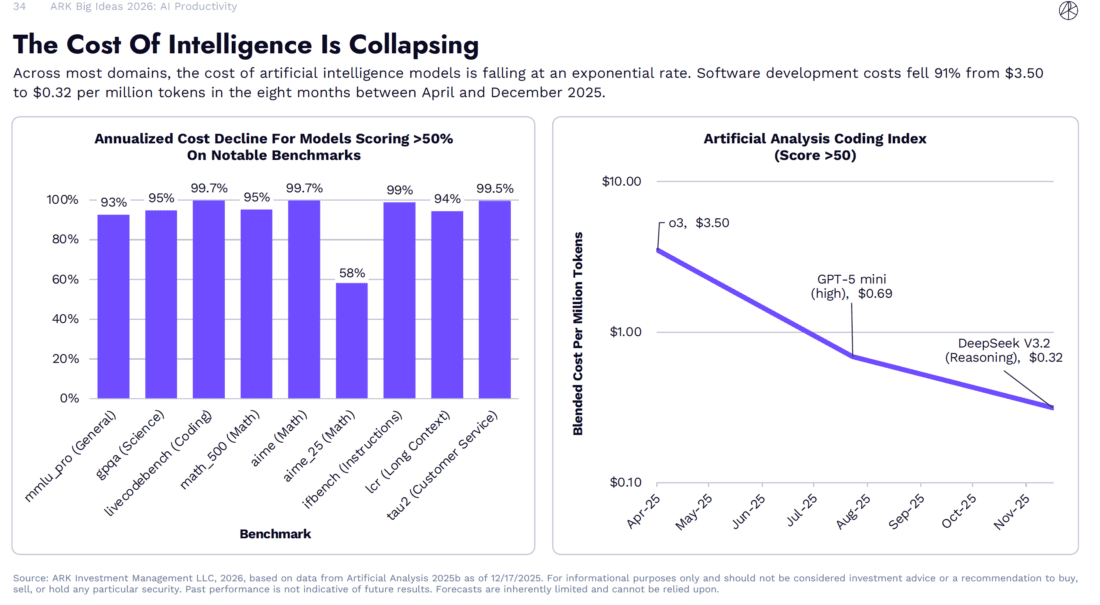

However, the price for fixed performance is dropping dramatically. If you want the equivalent of Frontier performance from a year ago, it’s now over 90% cheaper in most cases. Models that reach a score of at least 50% on many benchmarks, including coding, science, and general instruction following, can now often be had for 1% to 10% of what you would have paid for similar models in early 2025. These declines have accompanied a significant increase in the demand for tokens inferenced, with tokens inferenced on platforms like Open Router growing 25-fold since December of 2024.

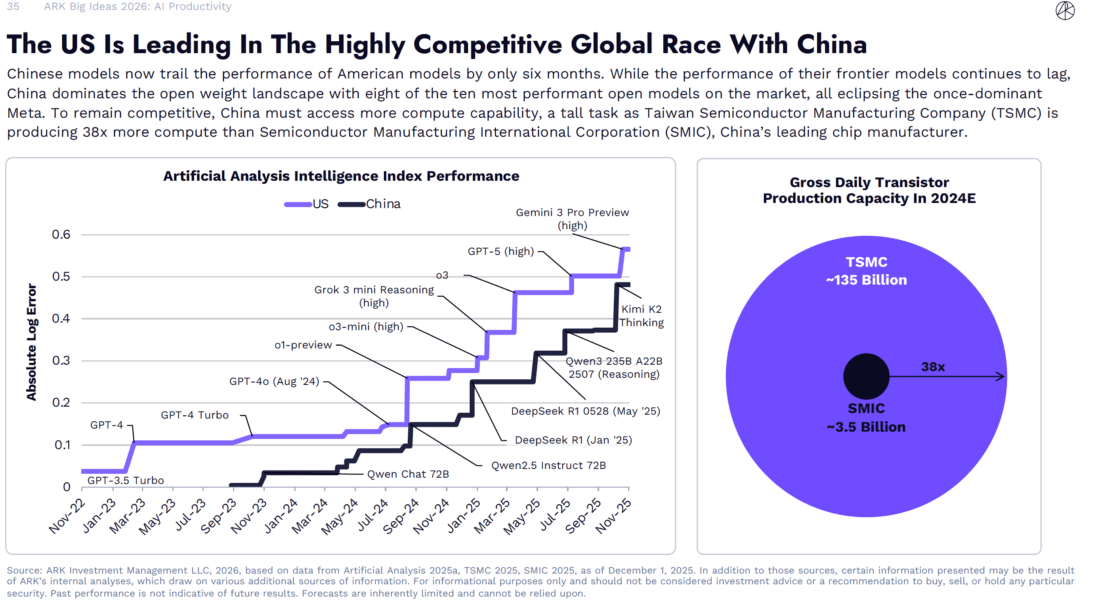

These performance gains and cost declines are not only limited to US-based labs. Chinese firms made waves in early 2025 by accelerating some of these cost declines with models that lagged top performers from the US by about 6 months in terms of performance but were often much cheaper to run. However, if China wishes to continue this progress in 2026 and beyond, they need a lot more compute. Much of China’s internal semiconductor technology lags the cutting edge by 3 to 5 years with many of their fabs being able to produce 7 nanometer chips at best and they produce those chips on a considerably smaller scale than countries like Taiwan. We estimate that in 2024, the most recent year for which we have full data, TSMC, Taiwan’s leading fab was outpacing SMIC, which is China’s leading fab by about 38-fold when you adjust for the quality of compute being produced. But if China can ramp internal compute sources or increase access to foreign chips like Nvidia’s H200s, which they are pushing to do so, they can certainly remain in a competitive uh position in coming years. Zooming back out to the impact of the cost declines that we’re observing, the increased value for money is driving a lot of spend on AI tools.

OpenAI’s annual revenue run rate has grown at a 250% annual rate over the past two years to roughly $20 billion, and Anthropic’s revenue has grown 850% over the past two years to a $9 billion run rate. New specialized startups like Curser, Harvey, Open Evidence, and Sierra found it in the past three years are hitting milestones of 100 million or even a billion in Annual Recurring Revenue (ARR).

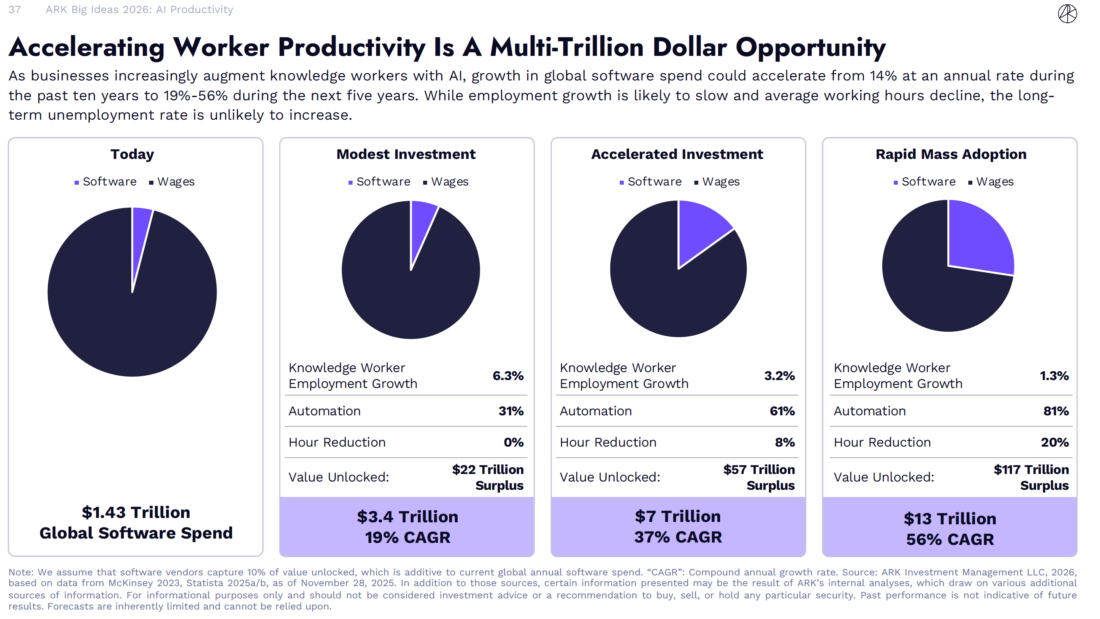

We believe these trends will accelerate software spend growth to between 19% and 56% depending on how aggressively enterprises adopt AI. At the midpoint, this would imply roughly similar levels of software spend growth seen during the pandemic with spend scaling to $3 trillion in the case of modest investment in AI or almost 7 trillion in the event of accelerated investment. To put this amount of spend in context, the global number of knowledge workers has historically grown at roughly 6% annually from 2011 to 2023. Assuming steady continued wage growth, this trend implies that enterprise spend on knowledge worker wages could continue to scale from about $30 trillion estimated today to over $45 trillion by 2030. In the event of an accelerated adoption of AI, we think some of that large potential increase in labor spend would flow through to automation software instead, resulting in that annual 7 trillion of global spend on software. In that accelerated scenario, we still assume over 3% growth in knowledge worker employment. So, it is assuming some offsetting of labor market growth in a strongly growing economy.

In summary, as costs fall and performance scales, we’re seeing more and more enterprises and knowledge workers automating portions of their workloads. We think that their investments in these automations are going to scale significantly as more performance gains are unlocked, eventually driving trillions of dollars of investment in not only software but also AI platforms and infrastructure.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from ARK Invest and is being posted with its permission. The views expressed in this material are solely those of the author and/or ARK Invest and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!