- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 2 of 13

Contributed By:

The following is a summary of a video recording and may contain errors in spelling or grammar. Although IBKR has edited for clarity no material changes have been made.

Hi, welcome to ARK Invest’s Big Ideas 2026 deep dive. I’m Brett Winton, the Chief Futurist, and I’m going to start right on Slide 4, which is titled the Great Acceleration.

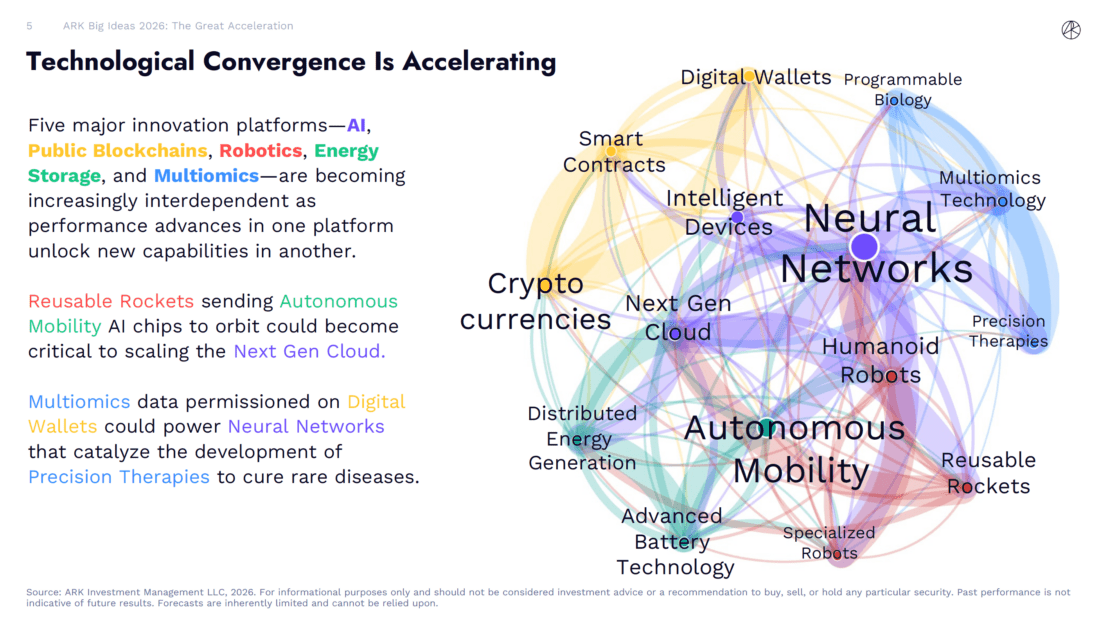

The core thesis both in this section and across the entire deck is that AI is the central dynamo, the spinning wheel of magic that is accelerating you know all the five major innovation platforms that we focus on and igniting a new era of macroeconomic growth.

So, the five major innovation platforms:

Each of these are technology platforms that are following steep cost declines. They’re cutting across sectors and they’re themselves platforms on top of which other innovations can be built.

On the right you can see kind of the innovations that we focus on today, the technologies that we focus on today. In AI, its neural nets, intelligent devices, and NextGen cloud and robotics.

It’s humanoid robots, reusable rockets, and specialized robots. In energy storage, its autonomous mobility, distributed energy generation, and advanced battery technology. In public blockchains, its cryptocurrency, smart contracts, and digital wallets; and in multiomics, it’s the multiomic technology, the core sequencers, precision therapies, and programmable biology.

This visualization on the right is the how these technologies interconnect and catalyze growth one to another. So just emerging over the latter half of 2025 was the idea that reusable rockets would be sending chips that also power Tesla’s autonomous vehicles into orbit to power the NextGen Cloud which is required for neural nets to operate and scale. Similarly, multiomic data will live in users’ digital wallets which then will be used to kind of train neural nets to better understand biological data and help to catalyze the growth of precision therapies. So, these technologies are increasingly interconnected and accelerating. We go through a scoring exercise called convergent scoring to look at what degree is one technology likely to cat or to catalyze the growth in another and how much growth should we anticipate that it’ll catalyze and that’s increased over time. So that’s visualized on the bottom actually year‑over‑year, there’s a 35% increase in the network density.

I think this is the degree to which technologies are likely to enhance each other, and if you look at on the right side, it’s at the innovation platform basis. You know, robotics has seen the most growth and then neural networks and AI, as I described, is the most important technology.

The fact that AI is accelerating so quickly is why the entire technology cycle is accelerating quickly because it’s feed stock into all of these innovation platforms and so this is an example of a new example of convergence that we think is going to meaningfully increase demand for an underlying technology. So, throwing lofting satellites with computer chips on them in order to power AI training and inference, we think, is going to be you know cost competitive and actually even potentially better in unit cost than going through the effort of building a data center on the ground. The way to think about this is like all of the material that goes into the data center on the ground exclusive of the chips.

Instead, you package it into the satellite, and you don’t have to deal with negotiating for land rights, and you know getting permits to operate in that specific area or finding you know pumping natural gas to that area and buying natural gas turbines to power that plant. Instead, it’s all powered by solar, and it lives in space. So, we think it’ll be cost competitive with that assumption, given the volumes of AI compute demand that there are that are out there relative to our prior expectations for what SpaceX was going to need to loft for its Starlink opportunity.

We think there could be a 60x increase in kind of demand for their core technology for reusable rocket. So, here’s an example where the demand from neural networks for tokens is powering demand for NextGen cloud and SpaceX by meeting that demand could yield you know a 60x increase in kind of the demand for its underlying technology.

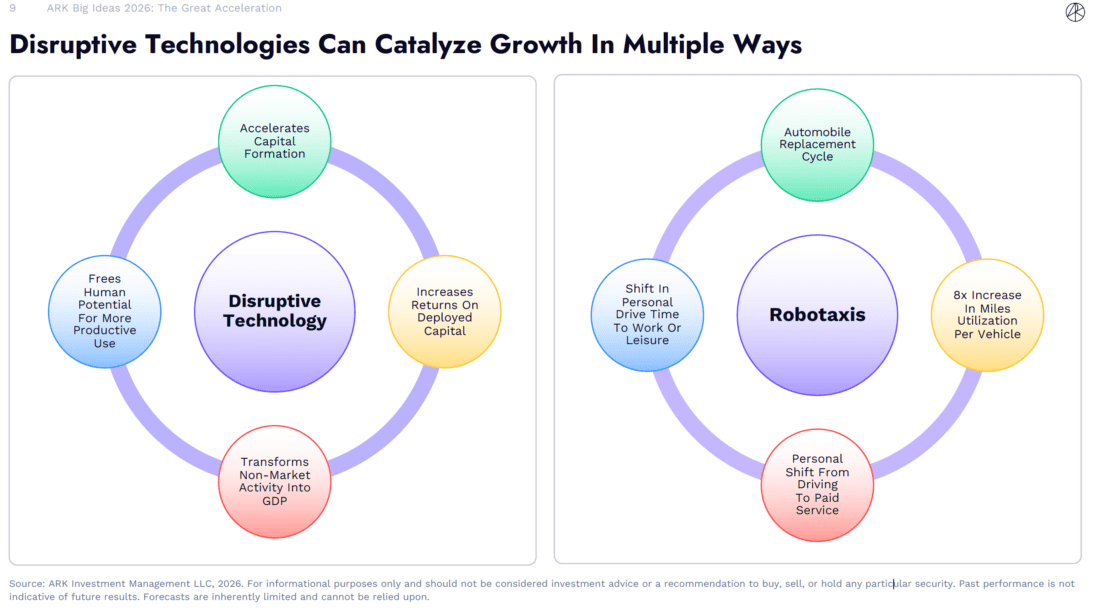

So, you know all of this acceleration is feeding into a radically a historic investment cycle between data centers, software, you know robotaxis and then into the 2030s humanoid robots. We think the investment in the underlying foundational assets that power technology is going to exceed any period in history even going back to the railroad where the you know building out the railroads consumed a large or contributed a large portion to GDP at that time, and so when technology when disruptive technology enters the economy, you actually get four kinds of macroeconomic acceleration from that entry first you accelerate capital formation.

What do I mean by that? I mean the dollars go into building the underlying infrastructure you need to use the technology. So that’s the data centers, that’s investing in kind of the software that’s going to run inside the enterprise and learn how to operate in the enterprise. That’s purchasing the vehicles that become the robotaxis.

Prior to the introduction of the technology that capital might have been kind of sitting in cash. Look at the big tech large cap tech balance sheets. They were sitting on cash. Now they’re realizing, “Oh, to compete, we have to build these data centers, okay”. Then once you bring the capital in, if the technology really is transformative, you should actually have a superior return on capital relative to what it was doing before. So, the data centers, and we believe this to be true, will return kind of a better ROI. They’ll return more cash relative to the amount invested both to the owners and macroeconomically than you would otherwise get. So, you get the foundation of economic growth and then you get the returns on that foundation improving part of the way those returns improve is they take non‑market activity, and they transform it into market activity.

You can see on the right we’re highlighting how robotaxis fit into this framework. Well, across the US, we drive so much manually driving that it’s in excess of $4 trillion of unpaid imputed wages driving. That’s just not recognized in GDP. So, if you deliver a robotaxi, people won’t pay the full freight for what they would have been paid if they were paid to drive, but they’ll pay a discount to that in order to have a service drive them around. So that’ll go from imputed wages that weren’t recognized into a value that gets recognized into GDP. Then finally, they have additional time while they’re doing that. Since they’re not pulling paying the full wage out, people who are riding around in robotaxis have additional time where they could work, they could work at their full wage rate.

And so, then that’s economically productive. Or they could watch Netflix, which they’ll likely do. And that’s macroeconomically productive, too. Because when you do not watch Netflix, that means you’re paying for Netflix and so you’re doing something else with your money or time.

Just to make this a little more tangible, here’s a here’s a specific example of how disruptive technology impacts the technology. Here we’re looking at a single robot level. So, on the left is what happens today. Right now, for a homeowner in the US, on average, they’re paying $2,600 out to people who come in, like electricians or, housekeepers or, somebody that comes in to like a handyman to fix up a cabinet and they do a lot of work on their houses.

In fact, if you look at the imputed labor cost of the work they’re doing, it’s $65,000 at average wages across the US in annual work that they’re doing and not paid for. They’re doing it just to keep up their home. So, if you introduce a single humanoid robot to that household, we think because they’re saving much so much time in labor, people will pay a lot for that.

In fact, if you amortize it over the life of or a five-year life of the robot, we think they’ll pay $20,000 essentially per year for access to that robot. You can think they no longer need the car because they’re getting driven around by robotaxis. So, then they’ll buy the robot so then the robot does the work that would otherwise be done by people in the household and by the work that they’re doing. and that costs $3,600 in operating costs for the robot on electricity and maintenance. Then the homeowner is willing to pay the free labor time is worth $30,000. And then there’s other work that would otherwise not be done by the robot, which otherwise wouldn’t be done by the homeowner. So, think of the sock drawer that’s disorganized, the vacuuming that doesn’t get done, that’s worth $7,000, and so, you end up with a $60,000 contribution per year to the economy for a humanoid robot that gets recognized into GDP where previously only 2600 appeared. And there’s also kind of like the labor hours, the value of the leisure hours where you’re able to watch Netflix instead of vacuuming. And your household is better organized. So, you just feel better and maybe you’re healthier because things are cleaner. You are more easily able to find that set of socks you were looking for to do well on that sales pitch you were going to do and so there’s other surpluses that aren’t captured here but the change is a more than 30-fold increase in GDP just for a single humanoid robot.

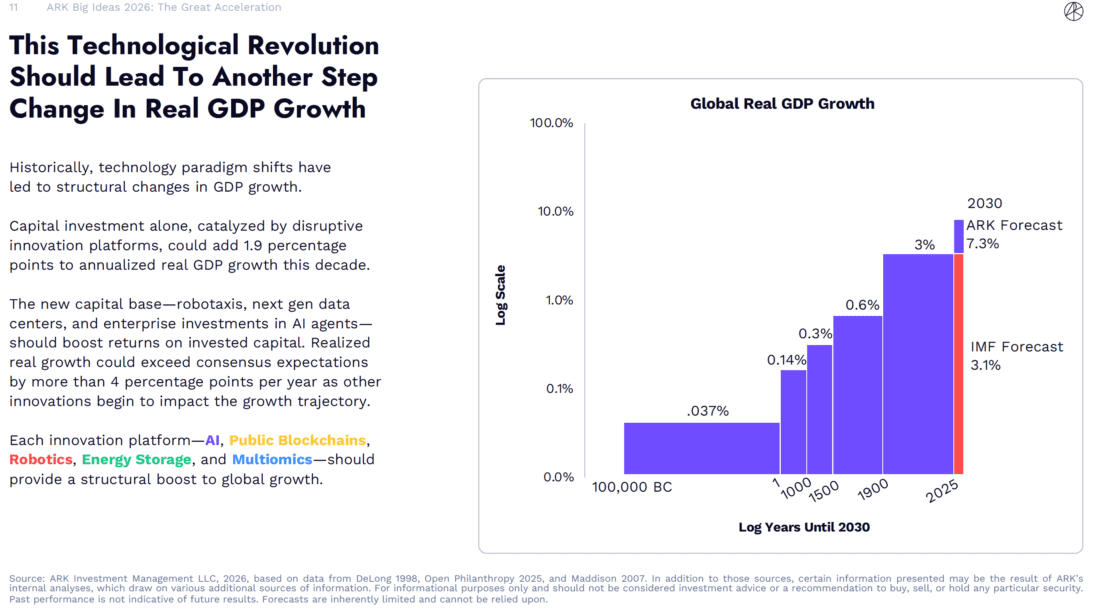

So if you were to penetrate the market, go from basically 0 to 80% penetration over a business cycle over five years that alone could accelerate GDP from the 2% to 3% per year to the 5% to 6% per year level and in aggregate the influx of these technologies consistent with history we think it’s going to change the equilibrium level of GDP growth. Actually, over the latter half of this decade, we think we’re going to average more than 7% real growth, up from basically 125 years of roughly 3% growth.

In prior technological periods, you had structurally lower growth. What does this mean? It means everybody is going to get a lot wealthier. This is great and it means that it’s catalyzed driven by the technologies that we see being introduced today across AI, public blockchains, robotics, energy storage and multiomics. All of these contribute to this transformation and growth, and you know markets will follow the macros.

But before we get to that people often ask, well what about quantum computing? What about fusion?

You know, there are technologies that are interesting and at some point, in the future, they may be disrupted, but the work that we’ve done suggests, at least in the quantum computing case and in the fuel cell case and in the fusion power case, not yet. It is not time yet, so disruptive technologies require steep cost decline unit economic cases across multiple sectors that prove compelling and that allows them to commercialize and get to scale and serve as platforms for additional technological innovation.

Quantum computing’s cost decline has actually been modest. I mean you you’ve doubled cubits over four years for the leading player in Google. Even if you assume they accelerate to a Microsoft style case, we think the big meaningful application of quantum computing, cracking RSA encryption won’t happen until the mid 2040s and more likely even with an acceleration to you know unit doubling every three years, it would be in the 2050s before it happens. Now there’s a lot that’s going to happen between now and 2044. So, for us it’s just not interesting from an investing perspective.

But there are plenty of technologies that are interesting. And as I said, the macroeconomic growth is going to in our view yield kind of market appreciation and so if you look at the long history of innovation market cap versus non‑innovation market cap as shown on the left you know we have had a period of inflection.

Inflections and growth in innovation and we think that’s going to accelerate. So, from 2015 to 2020 innovation compounded at 18%, 2020 to 2025 20% and we think it’s going to accelerate as these technologies deliver a more meaningful marginal share of economic growth over time. And by contrast it could be that you know non‑innovation market cap so incumbent companies that are in all of the indices will shrink over the next five years. So, imagine a period where you have accelerating GDP, you have a set of companies that are accruing massive enterprise value and if you’re not successfully innovation exposed, you produce negative returns in your portfolio. What a nightmare. I think everybody needs to make sure that they are positively exposed to innovation in a meaningful way given the point we are in the technological cycle.

And you can see on the right; we think that across crypto as well as private and public that innovation is going to make up more than 60% of global market cap in our view by 2030. And while that may sound like outrageous and extreme and large, well, it matches our underlying modeling for the individual technologies and the way they’re accelerating, it also matches historical time frames where there have been big bursts of investment and innovation.

Actually, if you go back to 1870, railroads made up more than 60% share of equity market cap in the late 1800s and it was because they prompted this huge wave of capital investment that had higher than normal returns because traveling by rail was so efficient. It allowed non‑market activity, know having to walk from place to place or ride horses from place to place into something that was measured into the economy and it freed up people’s time to do more productive activity and served as a platform on which other innovations can be built. Much of the buildout of the west depended on the railroad. Well, much of the buildout of the future world will depend upon the radical capability that we think AI is going to deliver to us over these five years and the decades to come. So, that’s a dive into the Big Ideas Great Acceleration portion from ARK Invest. I hope you enjoyed it.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from ARK Invest and is being posted with its permission. The views expressed in this material are solely those of the author and/or ARK Invest and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. For more information about the risks surrounding the trading of Digital Assets please see the "Disclosure of Risks of Trading Digital Assets".

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!