- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 6 of 13

Contributed By:

The following is a summary of a video recording and may contain errors in spelling or grammar. Although IBKR has edited for clarity no material changes have been made.

Hello everyone. I’m David Puell, a Research Trading Analyst and Associate Portfolio Manager for Digital Assets here at Ark Invest. And today we’re going to go through the Bitcoin section of Big Ideas 2026.

So, our main focus for 2026 as it regards to Bitcoin was just seeing it mature as an institutional asset across not only the ETF cohort but also digital asset treasuries and just as an ever constant and ever important part of portfolio for most investors going forward.

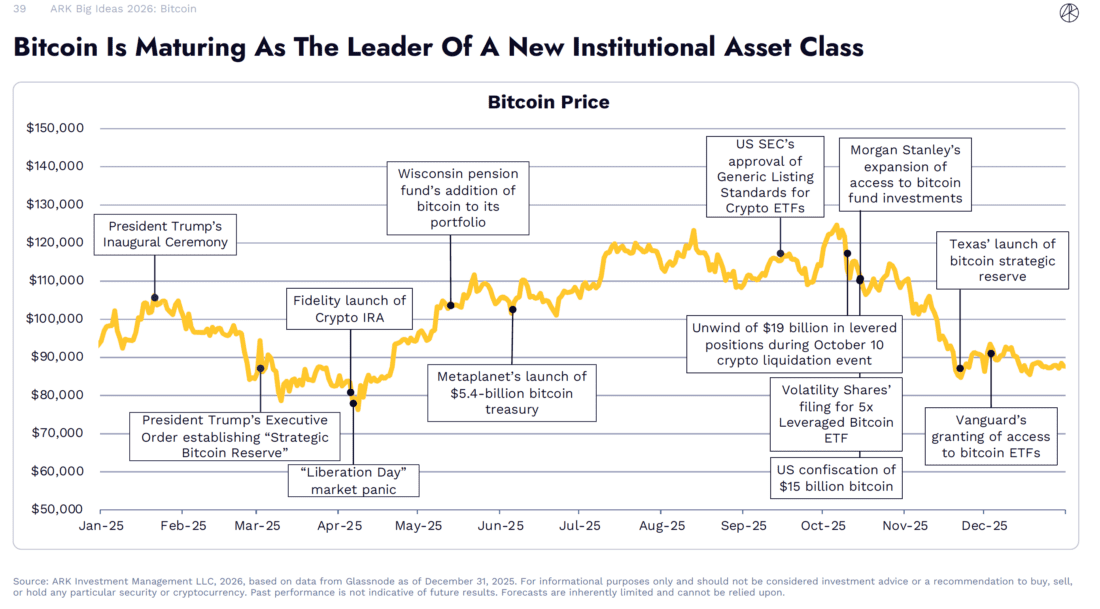

So, we’re going to go through the slides. A quick recap on price action here. We saw major developments under the Trump administration regarding Bitcoin and crypto adoption broadly. After the inaugural ceremony, we saw the establishment of Trump Federal Bitcoin strategic reserve which as opposed to buying is let’s say just holding Bitcoin out of different issues in criminal cases over time. This is very optimistic and a very neutral stance from a governance perspective. that signals government adoption quite well into the future.

Next, we have several developments in the institutional front where you see entities like Fidelity, Vanguard, Morgan Stanley leading the way in terms of Bitcoin adoption and developing Bitcoin products for their clients.

And we also see a lot of adoption across states. So, for instance, the Wisconsin pension fund included Bitcoin in their portfolio. And we also saw for the first time US state Texas adopting Bitcoin and actively buying it as part of their reserves.

We go to the next line the next slide. Talking about Bitcoin adoption broadly, especially amongst institutions, we saw it a continued adoption on the ETF front and also increasingly so on the digital asset treasury aka that front as well. So, if you add the AUM or balance of Bitcoin between those two types of structures or entities ETFs and that today or as of the end of 2025, they now add up about 12% of total Bitcoin supply which is quite significant and this this is an increase from an 8.7% of total supply back at the end of 2024. So, it’s over 3 percentage point increase over a single year which is quite significant.

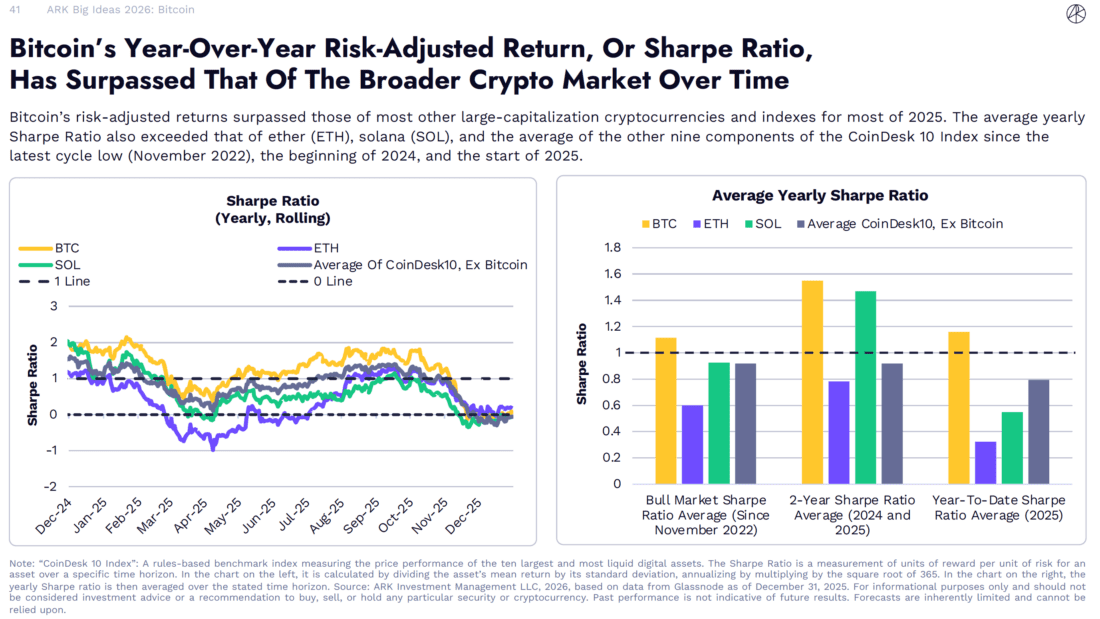

Next, we also noticed how especially in terms of risk adjusted returns which are one of the primary mechanisms where investors gauge a sense of risk versus return or portfolio placement at any given time. We also noticed that if when you measure Bitcoin’s risk adjusted returns, in this case just simply a sharp ratio over a yearly horizon and roll it over, if you average the role, you get a sense that for the most part, Bitcoin was the winner here when you measure it against Ethereum, Solana and other components of major indices like let’s say the CoinDesk 10 Index. So, across the board, Bitcoin seems to be very steady and reliable and leading the way for institutional adoption across mainly in this case a very healthy risk adjusted return pattern.

Next, we also noticed and this can be measured through several in several ways, but I think this chart gets a good point across which is Bitcoin’s volatility is obviously diminishing and perhaps even more importantly its drawdowns are less aggressive. This is particular to this last cycle that initiated in late 2022 or so bull cycle.

What we noticed for instance here is that when you measure the draw down from all-time highs at any given time as you see in the chart in the green line here if you take it and average it out over different time horizons in this case 5 years, three years, one year and 3 months when you average it you get a sense of not only the draw down but it also gives you a sense of frequency duration and depth of drawdowns over the time horizon you’re measuring with.

So, if we factor that in, we notice that in 2025 at a point in time every single average the five years, three-year, one-year, three months hit a much more muted drawdown compared to the past. So, you can for the most part claim that on average the maxim draw down of Bitcoin was the least severe in 2025 across all the all of Bitcoin’s history.

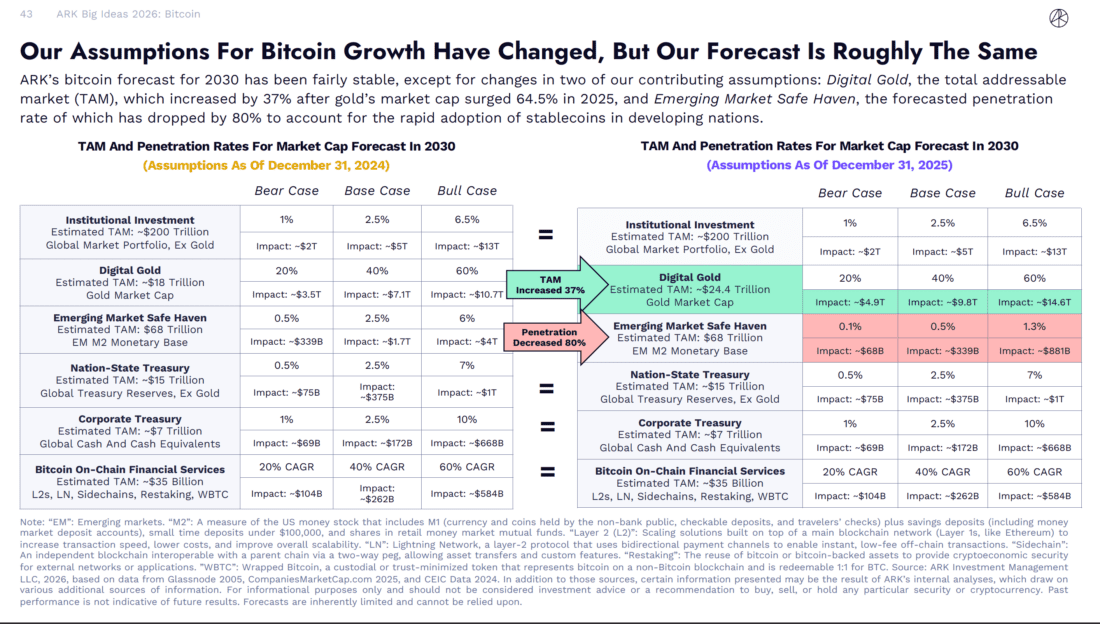

So, in this slide we did some tinkering in terms of our market cap estimates for 2030, end of 2030 for Bitcoin and basically, they were relatively similar to what we published back at the beginning of 2025. So basically, a year ago and although our estimates in terms of market cap have remained roughly the same, they have their components have shifted a little bit here.

So, in this slide we pretty much emphasize the changes we’re noticing here. On the one hand, we have the digital gold value accrual for Bitcoin being increased just for the fact that gold appreciated during 2025 giving us perhaps a higher total addressable market where Bitcoin can accrue some value out of into 2030.

So, on that front the TAM, Total Addressable Market, for Bitcoin as a digital gold saw an increase of about 37% which is relatively impactful. And on the on the other hand, we saw a decrease in our category for emerging market safe haven for Bitcoin and this is because we have been noticing much wider adoption of stable coins versus bitcoin in emerging markets.

What we feel is happening there is that citizens in emerging economies are preferring the stability of the US dollar as a defensive mechanism for savings and even portfolio management versus bitcoin for the time being which is perfectly natural.

We expect this perhaps to sustain to some extent but also change as bitcoin’s volatility keeps decreasing over time. So, in this bucket the penetration rate is what changed not the TAM. The penetration rate meaning is our assumption on how out of the total addressable market how much Bitcoin is going to penetrate and take out of that TAM and contribute to ultimately to its market cap. So from that front the penetration rate decreased by 80% meaning we expect that Bitcoin as opposed to holding a hypothetical 100% of emerging market safe haven it’s going to decrease by 80% to a 20% of the of the previous total into 2030 which is perfectly reasonable and it aligns with some data we’ve noticed out of chain analysis in Latin America sub-Saharan Africa and so on.

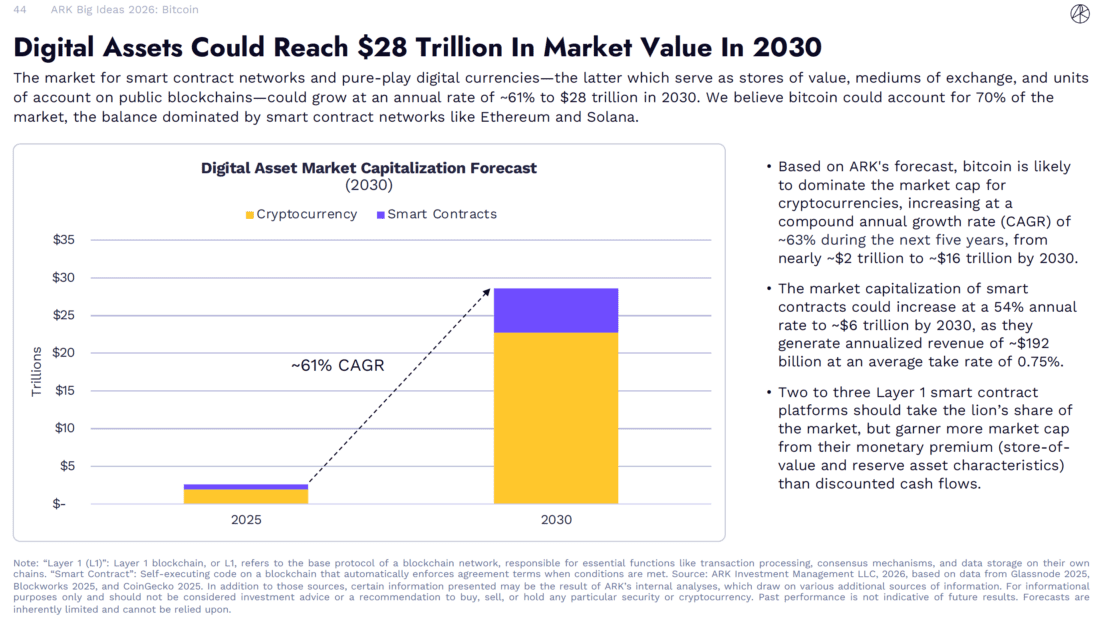

So, on our last slide on the Bitcoin section, we thought it would be very helpful to refresh investors on how we see the market not only in the Bitcoin monetary only cryptocurrency cohort, but also in the smart contracts industry as it’s developing over time.

So here what you see is basically two main drivers or categories for digital assets. One is cryptocurrency which are a pure play monetary based value accrual over time. This is mainly speaking of bitcoin excel in its monetary policy of 21 million cap supply and so on and on the other hand, we see the smart contract angle of things led in the industry by Ethereum, Solana and other tokens over time. So basically, what you see here is a target of about roughly 28 trillion by the end of 2030 across both cryptocurrency and smart contracts, and if we separate them a little bit here, we see an market cap total estimate for cryptocurrencies or monetary based digital assets from 2 trillion into 16 trillion by end of 2030.

This is mainly going to accrue into Bitcoin at least on a 70% dominance over competitors and on the other hand, we also think that part of that ultimate 28 trillion target is going to come out of the market cap capitalization of the smart contract cohort led by Ethereum and Solana. This more or less would target about roughly a six trillion target by end of 2030, and it’s based on a generative annualized revenue of about 192 billion at an average take rate of 0.75% during the period on average. So, aggregate them to together cryptocurrency or monetary digital assets and smart contract assets the expectation is we can see a growth of up to roughly 60, 61% CAGR between now and the end of 2030.

So that was a recap for our Bitcoin section and Big Ideas 2026. Please feel free to reach out on social media and we look forward to your comments and feedback on our latest research.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from ARK Invest and is being posted with its permission. The views expressed in this material are solely those of the author and/or ARK Invest and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. For more information about the risks surrounding the trading of Digital Assets please see the "Disclosure of Risks of Trading Digital Assets".

Trading Bitcoin involves significant risk. Bitcoin prices can be highly volatile and may fluctuate rapidly, potentially resulting in substantial losses. Because Bitcoin operates on a decentralized blockchain, network congestion or technical issues may occasionally delay transaction settlement. Regulatory frameworks for digital assets are still evolving and could impact availability, liquidity, or pricing. When trading through Interactive Brokers, execution and custody are facilitated by regulated partners such as Paxos or Zero Hash; however, these arrangements do not eliminate the possibility of operational or counterparty risk.

Cryptocurrency based Exchange Traded Products (ETPs) are high risk and speculative. Cryptocurrency ETPs are not suitable for all investors. You may lose your entire investment. For more information please view the RISK DISCLOSURE REGARDING COMPLEX OR LEVERAGED EXCHANGE TRADED PRODUCTS.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!