- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 16, 2026 at 10:33 am

The article “Second Chance: Life with Less Student Debt” was originally published on Alpha Architect.

Student debt is often treated as a personal issue. Individuals borrow, replay, and manage their own financial outcomes. But in reality, debt burdens shape much more than individual balance sheets. They affect credit markets, labor mobility, and long-term economic opportunities. This paper introduces a new perspective. Debt relief is not just redistribution. It changes behavior, incentives, and financial stability. The result is a powerful mechanism. Reducing debt burdens improves both financial and labor market outcomes and targeted relief can reshape economic trajectories for distressed borrowers.

Debt relief improves overall financial health

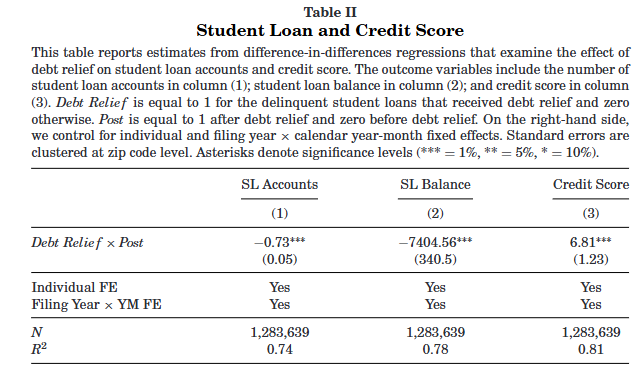

The paper shows that borrowers who receive student debt discharge reduce their total liabilities and improve credit outcomes. Rather than increasing borrowing, they deleverage. Lower balances, reduced utilization, and higher repayment rates all point to improved financial discipline following relief.

Spillover effects extend beyond student loans

Debt relief does not operate in isolation. Borrowers who receive relief experience significantly lower delinquency rates across other forms of debt, including credit cards and mortgages. This highlights positive externalities, where improving one part of the balance sheet strengthens the entire financial position.

The costs of default matter as much as the relief

A key insight is that both treated and control groups drive the results. While treated borrowers benefit from discharge, control borrowers face wage garnishment and collections. These enforcement mechanisms tighten liquidity constraints and worsen outcomes, amplifying the relative gains from relief.

Debt overhang distorts economic decisions

When borrowers expect future income to be seized through garnishment, incentives to work, move, or pursue better opportunities decline. Removing debt alleviates this distortion, restoring incentives for income growth and long-term decision-making.

Mobility increases after debt discharge

Borrowers who receive relief are more likely to change residence, switch jobs, and move across industries. This suggests that debt acts as a constraint on geographic and professional mobility, limiting access to better opportunities.

Income rises following debt relief

Treated borrowers experience higher income growth and earn approximately $3,000 more over three years. This reflects both improved labor incentives and increased productivity following relief from financial distress.

Psychological effects play a meaningful role

Financial distress reduces cognitive function and productivity. Debt relief alleviates stress, leading to improved work performance. This is reflected in higher variable pay, such as bonuses and overtime, and increased labor supply.

Debt burdens affect more than consumption

Student debt influences not only spending but also borrowing behavior, credit performance, and labor market outcomes. Advisors should consider debt as a key driver of long-term financial trajectories.

Recognize spillover effects across balance sheets

Reducing one liability can improve overall financial stability. Lower delinquency and reduced leverage suggest that debt relief can strengthen household balance sheets more broadly.

Incorporate labor income dynamics

Debt overhang and financial distress can affect income growth and career decisions. Portfolio construction should account for the interaction between human capital and financial constraints.

Understand heterogeneity in outcomes

The benefits of debt relief are strongest for distressed and liquidity-constrained borrowers. Targeting matters. Blanket conclusions may overlook these differences.

“Student debt doesn’t just affect what people owe. It affects how they live and work. When debt becomes too burdensome, it can limit job opportunities, reduce income growth, and increase financial stress. When that burden is reduced, people tend to improve their financial situation. They pay down other debts, become less likely to miss payments, and are more able to pursue better job opportunities. The benefit goes beyond the loan itself and improves overall financial stability.”

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

We exploit an episode of plausibly random debt discharge due to the loss of paperwork for thousands of defaulted borrowers to examine the effects of private student debt relief on borrower outcomes. We find that borrowers who receive debt relief (treated) experience declines in debt balances and delinquency rates on other accounts, and increases in mobility and income relative to those who bear the costs of default like wage garnishment and collections (control). Borrowers in both groups contribute to our findings through different mechanisms. While our estimates may not directly apply to blanket student loan forgiveness, they speak to the benefits of forgiveness in reducing the consequences of debt burden for distressed borrowers.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!