- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 10 of 13

Contributed By:

The following is a summary of a video recording and may contain errors in spelling or grammar. Although IBKR has edited for clarity no material changes have been made.

Hey everyone. My name is Sam Korus and I am a Director of Research at ARK joined today with Akash. My name is Akaash TK. I am the Research Associate here at ARK covering the robotics and autonomous technologies. And today we’re going to dive into the robotics big ideas section. So, let’s kick it off.

And really, automation, broadly speaking, is leveraging human labor. If we’d had no automation, we’d likely still all be working on farms and just spending all day getting enough energy to survive. So, this is something that we should want a lot. But the reality is anytime you mention robotics or automation, the normal discourse goes to, But what about jobs?

And really, you know, historically, technology frees workers from low productivity and less interesting tasks. And so, you know, generally speaking, I would say the burden of proof on technological unemployment lies with those saying it will occur because it has not occurred through any innovation in the past here. But obviously things can change.

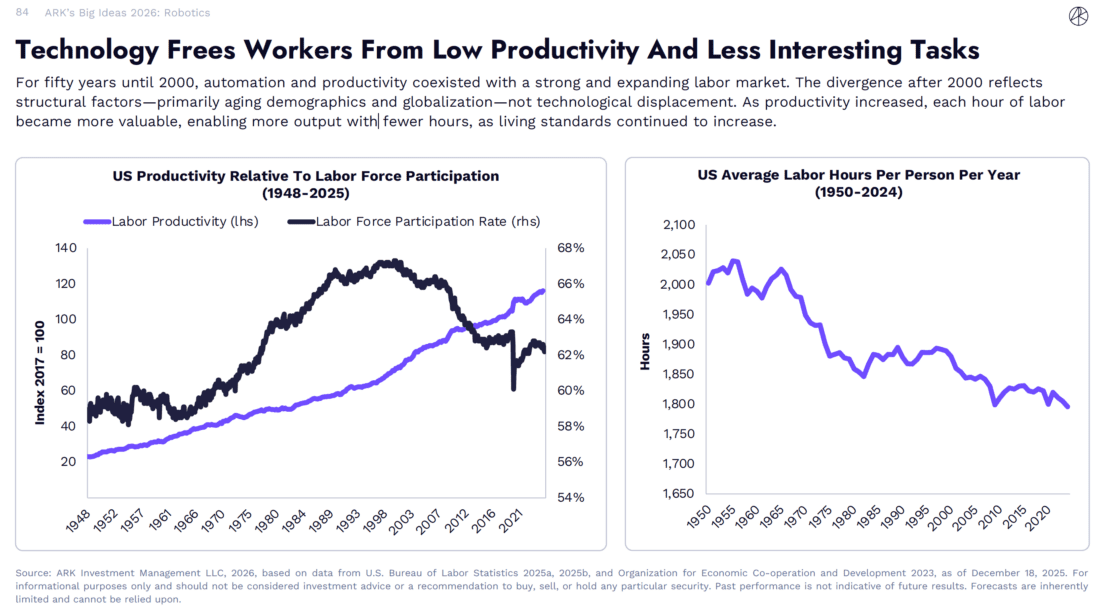

And so, let’s look at some of the data here, which is that, you know, for the 50 years until 2000, automation and productivity coexisted with a strong and expanding labor market. And then in 2000, there is a divergent, but we think that that’s largely because of structural factors, including aging, demographics and globalization, not technological unemployment. And you can see this because labor productivity continues to grow, labor force participation still above where it was from the 40s through the 70s.

But I think an interesting thing to look at here is that, you know, from the 50s all the way through today, the number of Labor hours worked per person per year has been coming down. And so, this trend we believe should continue. And that’s fine because you’re going to be more productive with each hour you work. But at some point, in the future, could this reach 0? That’s really where a lot of the debate comes about.

I don’t think it will necessarily hit zero at any time in the near future. But even on the way from working four days a week, three days a week, two days a week to, you know, amazing abundance, there’s a lot of productivity that will occur. And I think in important thing here is really to understand where we are in the history of robotics and industrial automation, broadly speaking. And that is really inning one of all of this.

And so up until, you know, really the past year or two, everything has been structured in terms of automation and industrial automation. And here you can see, you know, one of the most automated companies in the world is Amazon, and they have a robot density, which is, you know, the number of robots per 10,000 employees of 6,400 up significantly from a decade ago.

But then you look at the most automated industry, which is automotive, and those are far below where Amazon is, though having increased significantly over the past 10 years. And then you look at something like manufacturing, and that’s even less than the sub industry of, you know, automotive specifically. And so, we’ve had, you know, decades and decades of automation. It’s still improving, but you can see that relative to the best company in the world, we’re really nowhere. And so, there’s a lot of open space for innovation.

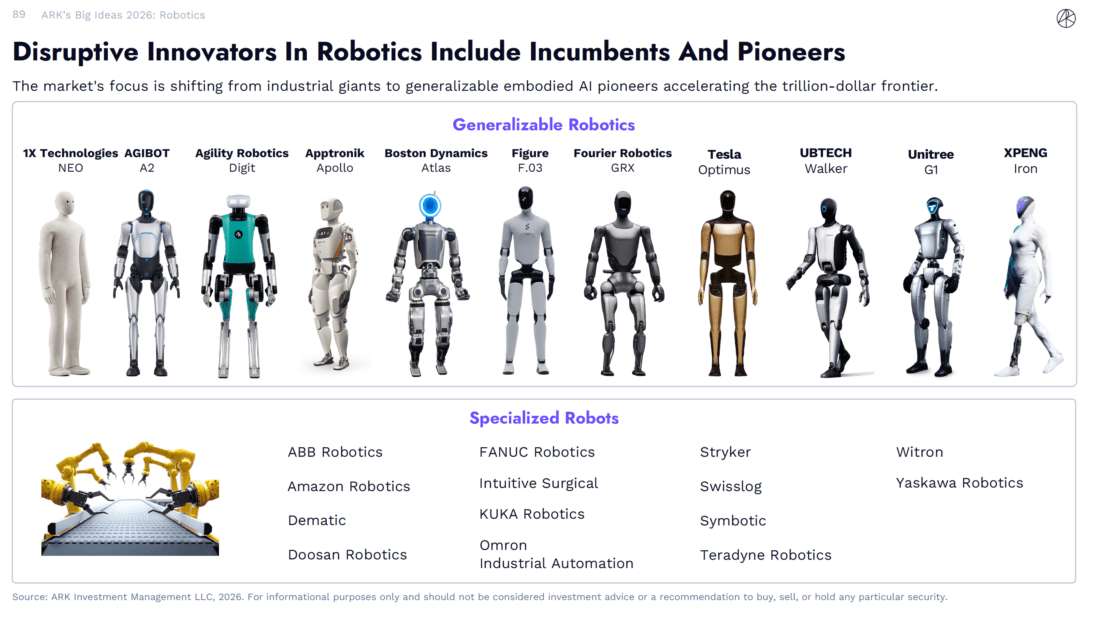

And a lot of this only opens up through unstructured robotics, which is why, you know, generalizable robotics, humanoid robotics are so exciting. And it’s an incredible opportunity. You know, broadly speaking, we think this is a $26 trillion opportunity split roughly equally between manufacturing and household robotics.

We can get into that breakdown, but really, if you get a humanoid robot that can perfectly, one to one replace a human, then you fundamentally change what the economy is. And so, you know, even though $26 trillion is a huge opportunity, if you reach that level of capability, you know, you fundamentally change everything.

And so, what’s the manufacturing opportunity? Well, you’ve got roughly 32 trillion in global manufacturing GDP as our forecast. We think that conservatively humanoid robot could add 100% productivity uplift and as a take rate, you could take like 35% of that productivity uplift and that gets to roughly $13 trillion in opportunity.

On the household side, you have a 2.8-billion-person workforce, 2.3 hours of unpaid work per day, a global average, salary of $12.00 an hour and people valuing their free time at half of their paid wage and that gets to a $13 trillion on the household side.

Then, you know, just going back to this chart on the left here, it really another demonstration of how early we are in this unstructured robotics side of things. And so, on the left there industrial robots. Those are, you know, the robot arms that you’re probably thinking of when you think of industrial robots. There’s only been 7 million of those sold since the 1960s again. So, you see that there is a cap on how structured an environment can constrain, how useful these things are, despite all of the amazing things we’ve done so far.

But then you look at the quadrupeds in the humanoids that are far more recent and, 10s of thousands. So again, just reiterating how early we are right now, but not to say that things aren’t moving extremely quickly.

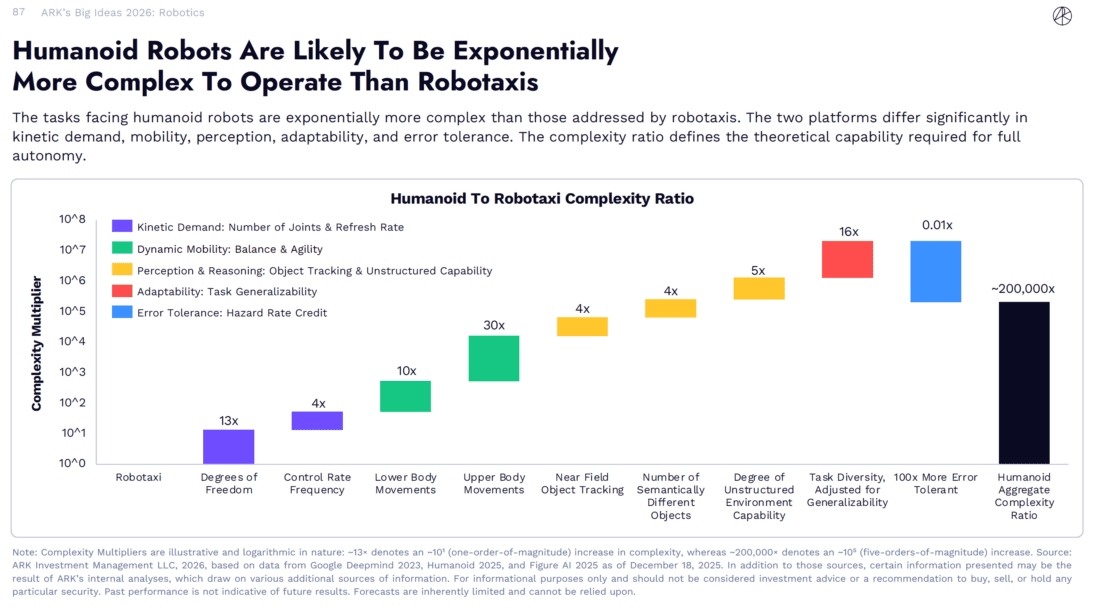

Now I’m going to pass it over to Akaash to talk about, you know, how hard is it to get to unstructured capability? As Sam mentioned, the tremendous opportunity there is for generalizable robots. I’m going to dive a little bit deeper into how complex it is to realize that opportunity and what that pathway actually looks like. Our research suggests that humanoids are around 200,000 times more complex than a robot taxi.

The best way to think about this is that a robotaxi has basically a singular goal taking you from point A to point B, and all of the actions that it principally takes are translated into its wheels, which moves in four directions, side to side and front and back.

Whereas for humanoid robot, it has multiple goals that it has to complete like such as like you know, the best way to think about it is like unloading a dishwasher. It has to take the mugs and then put it back into a cabinet, but then it has to move towards the cabinet and then put it over there. So, it doesn’t just act on its foot or wheels, but it has multiple joints such as its hips, arms and legs and fingers. All of these actually compounds as it effectively acts together to create a seamless motion.

But one thing does work in the in favor of humanoids, it’s error tolerance. Given it’s not a two-ton hunk of metal that is moving at 60 mph in a freeway, a little stumble as it moves around the counter wouldn’t be as catastrophic as a robot taxi moving at 60 mph.

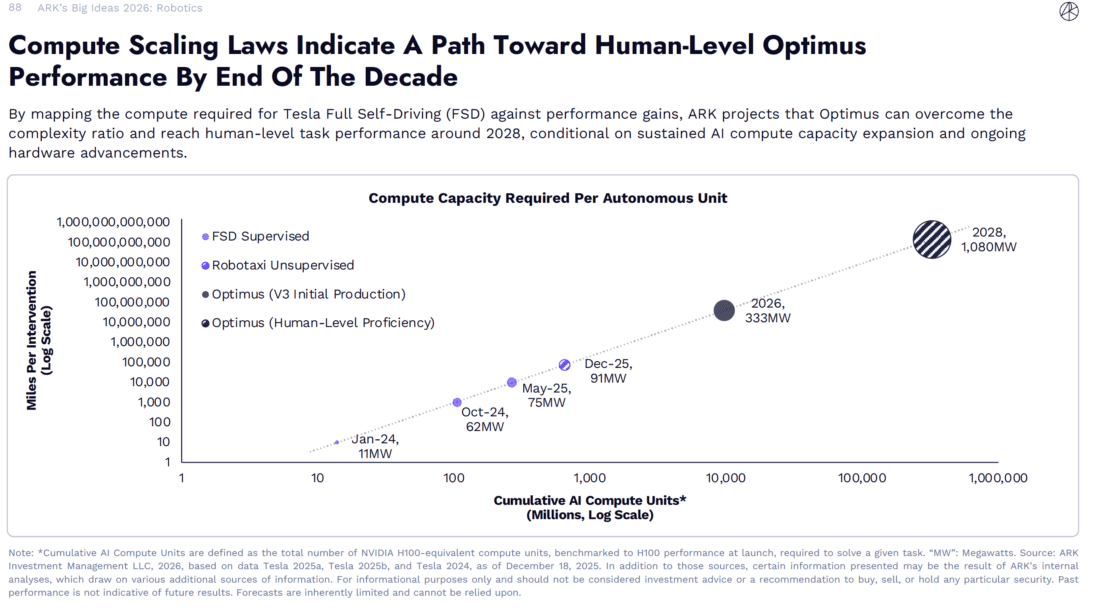

Now, hearing all this, one might think that it like if it’s 200,000 times more complicated than robotaxi and robotaxis are just getting to a point where they’re like, you know, commercializing at this point in time, we are probably like decades away until humanoids actually like become a reality.

But here at ARK, when we are using the Wrights law curve to see the rate of improvement in AI hardware as well as its software, we see a clear pathway in achieving this Herculean task of like, complexity ratio that’s more than 200,000 times.

Looking at Tesla’s training compute capacity and its FSD’s performance gains, we can see a clear linear pathway that we could chart. And using that, we think humanoids will get to a point where it will be commercializable just like how robotaxis are today by 2028.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from ARK Invest and is being posted with its permission. The views expressed in this material are solely those of the author and/or ARK Invest and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!