- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 1, 2025 at 10:15 am

We have held for some time the view that long-run global geopolitical and fiscal trends have the potential to drive a very powerful bull market in gold.

Geopolitically, the world has been moving from a globalising “Washington consensus” towards multi-polarity and great power rivalry for some time. Fiscally, very high sovereign debt and long-run untenable domestic deficits (in the US, in parts of Europe and in China) are a potent cocktail that history tells us usually ends in currency debasement, inflation and fiscal dominance.

These trends already held the potential to create a situation where multiple pockets of global capital attempt to acquire gold, as a “safe” monetary metal, simultaneously. As we have often repeated, the gold market is simply not large enough to absorb such a simultaneous global bid without much higher prices. President Trump is accelerating and super-charging the potential for that simultaneous global bid.

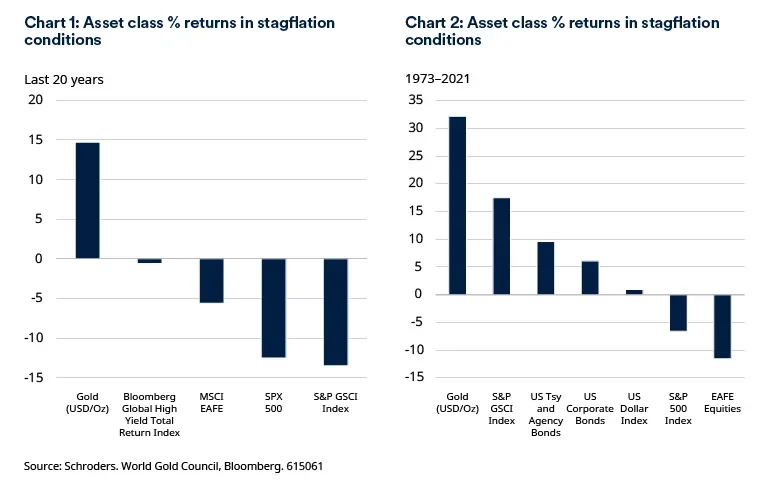

Trump’s protectionist agenda is cyclically stagflationary as a base case.

The Schroders Economics Team places the impact of “Liberation Day” tariffs on US inflation at 2% with a hit to growth of almost 1%, before accounting for any retaliatory tariffs. As charts 1 and 2 below demonstrate, stagflation can be painful for risk assets but tends to be very supportive for gold.

Note: MSCI EAFE (Europe, Australasia and the Far East). Past performance is not a guide to the future and may not be repeated.

The bigger picture is potentially much more seismic. By proposing heavy tariffs based on the size of deficits (not actual trade barriers) Trump is making it clear that the US wants not free trade but balanced trade. This rejection of deficits is the starkest rejection yet of globalisation but also can be seen as a de-facto rejection of the US dollar-centric global monetary regime that the global economy has lived under since the end of Bretton Woods in 1971.

Since then, the US dollar has acted as the primary global reserve currency, dominating official reserves and dominating international trade and finance, far beyond US share of global GDP. It has underpinned an open and rules based global trading system, complemented by steadfast geopolitical alliances.

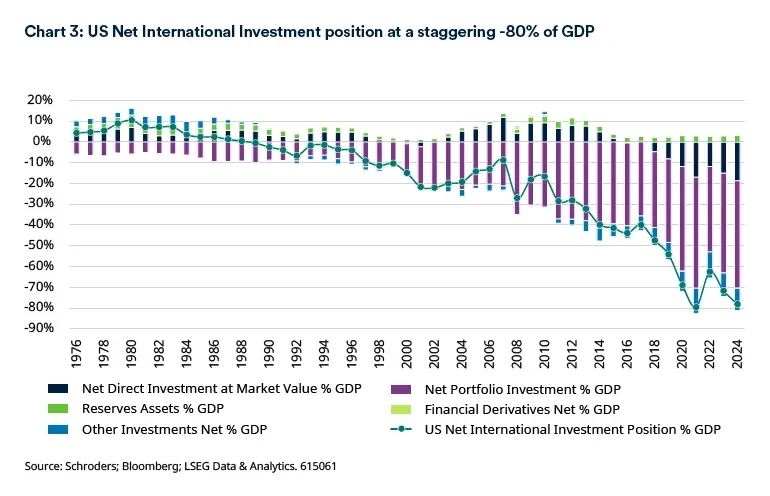

One of the largest effects of this dollar standard status quo has been the recycling of dollar revenue into US dollar assets, mainly Treasuries, which are seen as “safe” assets and the bedrock of the global financial system. Foreign holdings of US equity and private credit assets are also enormous. This cumulative flow now leaves the US with a net international investment position of a negative US$26 trillion, as Trump himself quoted in his 2 April address.

It does not take a Nobel Prize in economics to work out that the current tariff-based assault on the global trading system might, in turn, lead to significant repatriation flows amid a questioning of just how “safe” dollar assets now are or how bright the relative US economic outlook is. With such a dearth of credible alternatives, expecting gold to be a major beneficiary of such a repatriation trend is common sense to us.

Since finally “breaking out” in early 2024, gold prices have rallied by over US$1,000/Oz. Gold has had a particularly good run recently through Q1 2025, with prices reaching $3,150/oz in early April.

This brief note is not the place for a detailed dive into gold supply and demand but it is worth stating again that in a scenario where already strong central bank demand is joined by strong global investment demand, gold prices could easily move much higher to generate the increase in recycled supply and destruction of jewellery demand necessary to balance the market. Mine supply cannot respond quickly even at much higher prices. Despite already record high prices, mine supply is basically flat on 2018 levels.

Gold at $5,000/oz by the end of the decade did not feel an outlandish scenario twelve months ago. It feels frankly conservative now.

For gold equities, we think current prices are very likely to translate into the largest growth in earnings and free cash flow of any sector in the broad equity market.

Despite this, investors have on aggregate responded by selling passive exposure to the gold equity sector at the fastest rate we can see on record. In 1Q 2025 alone US$2.4 billion has been liquidated from passive products. To us, this is astonishing, and very bullish from a sentiment perspective.

No other major commodity is anywhere near its all-time real high, let alone above it. This is because gold is rallying as a monetary asset, not as a commodity asset. The rest of the commodity complex (for example, diesel, steel, fossil fuel derived consumables) is a big driver of gold producers’ operating and capital costs. Cost inflation from these areas, and from labour, is far more limited than in 2021/22. With gold prices at record highs, this translates into record profit margins for gold producers.

—

Originally Posted on April 21, 2025 – Gold: an alternative to “safe” dollar assets?

The views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

U.S. Spot Gold trading through IB LLC accounts is only available to legal residents of the United States that do not reside in Arizona, Montana, New Hampshire, and Rhode Island.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!