- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 29, 2026 at 1:14 pm

Continued disagreements between Washington and Tehran are prolonging the Strait of Hormuz blockade, sending WTI crude north of $107 this morning as commodity traders worry about a dire supply outlook. The oil surge has materially raised inflation expectations and is lifting global interest rates on an eventful week for monetary policy decisions. The US yield curve jump is being led by the short-end while the 30-year maturity nears the critical 5% level as fixed-income observers slightly open the door to a potential hike in 2026 as the path for a cut has essentially closed. Meanwhile, the move in Treasuries can be altered in either direction during this afternoon’s FOMC meeting, the last for Chair Powell, as investors are eager to hear if the committee is turning increasingly hawkish in light of accelerating cost pressures amidst stable employment trends. Despite the macro headwinds, which are currently severe, stocks are hanging in there, as four of the mag7 names are scheduled to report after the bell while a fifth delivers tomorrow following the close. Equity bulls are hoping that robust results alongside rosy guidance can keep the benchmarks near their records. Indeed, it’s only the tech and energy equity sectors that are working today, with all of the other nine major categories sinking as cyclical momentum gets battered as shown by the Dow Jones Industrial and Russell 2000 indices retreating. Elsewhere, the greenback is strengthening, volatility protection instruments are being picked up, cryptocurrencies are benefiting from Nasdaq enthusiasm, prediction markets are catching bids, however, non-energy commodities are getting crushed in consideration of significant slowdown concerns and prospects of tighter financial conditions.

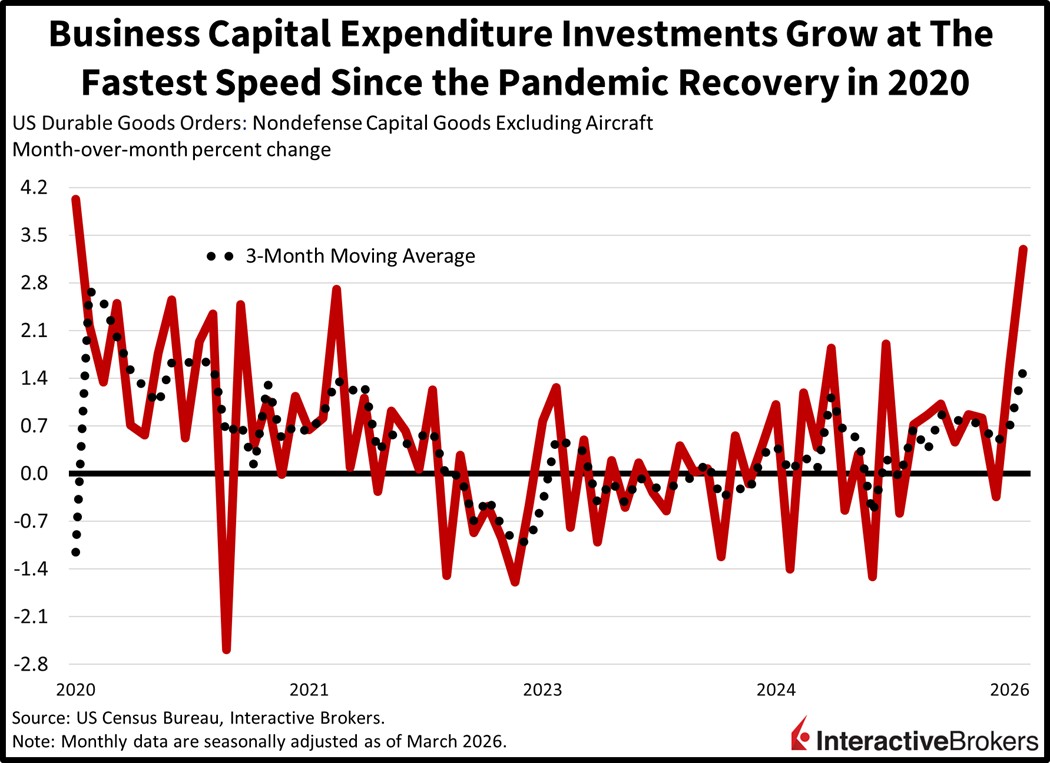

Durable goods orders crushed expectations last month as the business investment category jumped to a 69-month high that was established during the pandemic recovery in June 2020. The headline figure depicting a 0.8% month over month (m/m) climb beat the 0.5% projected and reversed February’s 1.2% decline. Corporate capital expenditures expanded 3.3% m/m, well ahead of the 0.5% estimate and the prior month’s 1.6%. Defense aircraft, computers/electronics and motor vehicles were the strongest gainers across individual categories, growing transactions 16.9%, 3.7% and 1.3% m/m, while the machinery, appliance, primary metals, other and fabricated metal products segments rose less than 1%. Passenger jet purchases were the most significant drag, falling 21.1% during the period.

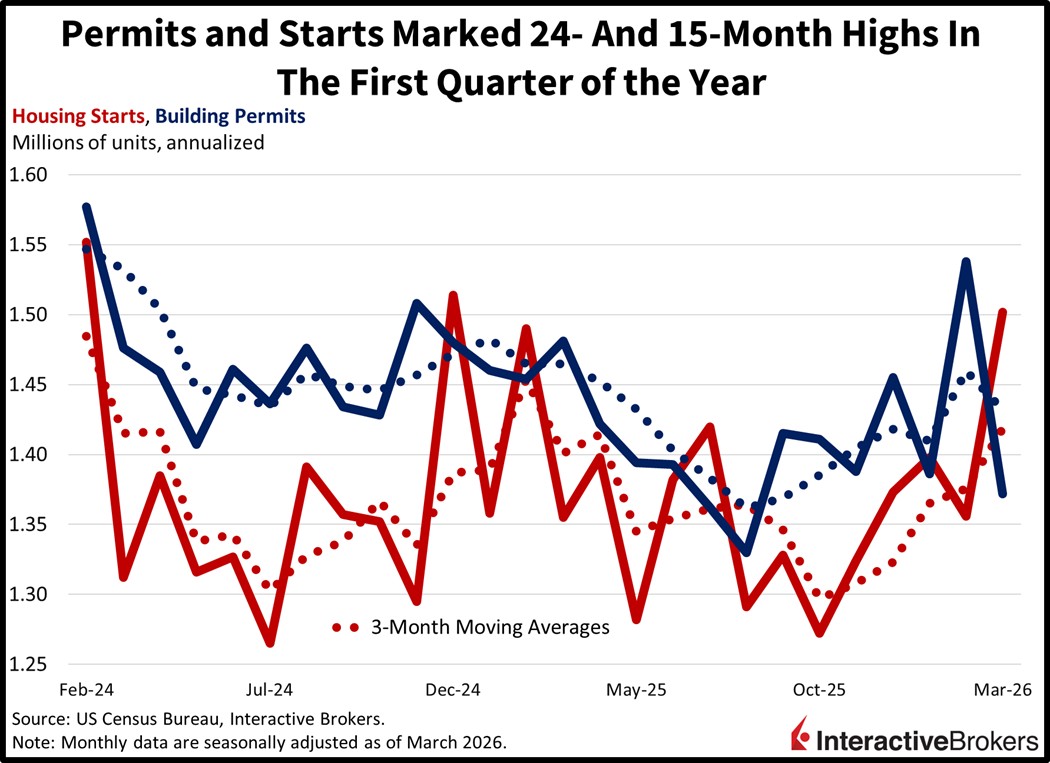

Building permit issuance and housing starts marked 24- and 15-month highs during the last two months of the first quarter although overall momentum remained near trends as elevated mortgage rates, heavy valuations, pricey materials and labor shortages prevented much progress. This morning’s print reflected February and March figures since data collection and analysis were delayed due to the extended government shutdown. Generally speaking, the multifamily segment performed better than singles as the rental market continues to be stronger than the one for purchasers.

Macroeconomic risks are significant at this juncture, but stock market bulls are hoping that a rosy path ahead for artificial intelligence can continue to offset cyclical weakness. If earnings, capital expenditures and outlooks are buoyant, investors could remain sanguine even as the threat of a slowdown in overall activity, loftier borrowing costs and widening credit spreads raise eyebrows. After a historic advance amidst equity benchmarks still near records, this afternoon will be monumental regarding monetary policy, the path for interest rates and whether the rally in technology has further room to run. Meanwhile, one could argue that the landscape is worse today than it was at the market lows of March 30 and that the S&P 500 hasn’t had a 10% correction this year despite the substantial dangers right in front of us. Against this backdrop, the final days of April and the beginning of May could offer the bears an opportunity to at least retest some of the closely watched intermediate- and longer-term moving averages on the major benchmarks as softening profit expectations, soaring bond yields and a new Fed Chair spark meaningful volatility in the current quarter.

Australia’s headline inflation picked up in March according to both year-over-year (y/y) and m/m results of the Consumer Price Index, although a trimmed measure that excludes items with volatile prices was slightly less severe. The overall Consumer Price Index was up 1.1% m/m and 4.1% y/y. In February, the indicator depicted no monthly change and a 3.7% y/y jump. For the m/m print, transportation costs led the gains, climbing 9.2% in response to higher gasoline prices caused by the Iran War. Other categories that became more expensive and the extent of their changes were as follows:

Meanwhile, the following categories became less expensive as stated:

Trimmed mean inflation, which excludes items with the largest price increases, repeated February’s 3.3% y/y rate.

The Bank of Canada decided today to maintain its key interest rate at 2.25% but warned that inflation could peak at 3% before easing to the organization’s 2% target next year. Earlier this month, Canada’s CPI depicted prices climbing 2.4 y/y. When announcing the decision to hold, Bank of Canada Governor Tiff Macklem said the surge in gasoline prices and elevated food costs are likely to push up headline inflation, but he cautioned that the outlook is heavily dependent on the Iran War and associated oil prices. Looking ahead, the bank left its GDP growth estimate unchanged. It believes the economy will expand by 1.2% this year and 1.6% in 2027.

The Economic Sentiment Indicator (ESI) fell 2.9 points to 93.5 in the European Union this month with weakness occurring across various metrics. Separately, the Employment Expectations Indicator (EEI) fell 4 points to 93.2. Within the ESI, consumer confidence and views of managers in services and retail trade deteriorated, although confidence in construction and industry was fairly stable. Confidence in the services sector sank 3.4 points with past business situation and demand in the past and expected demand all worsening. Retailers, meanwhile, lowered their expectations for the future business situation, causing the sector’s overall score to sink 1.7 points. Regarding consumers, confidence fell four points, a result of weaker results for households’ past and future financial situations, intentions to make major purchases and expectations about the economy.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!