- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 28, 2026 at 1:49 pm

Core thesis: LLMs will not kill all alpha. They may, however, compress the shelf life of copyable alpha by making the same data, same indicators, and same backtesting logic easier for more participants to industrialize at the same time.

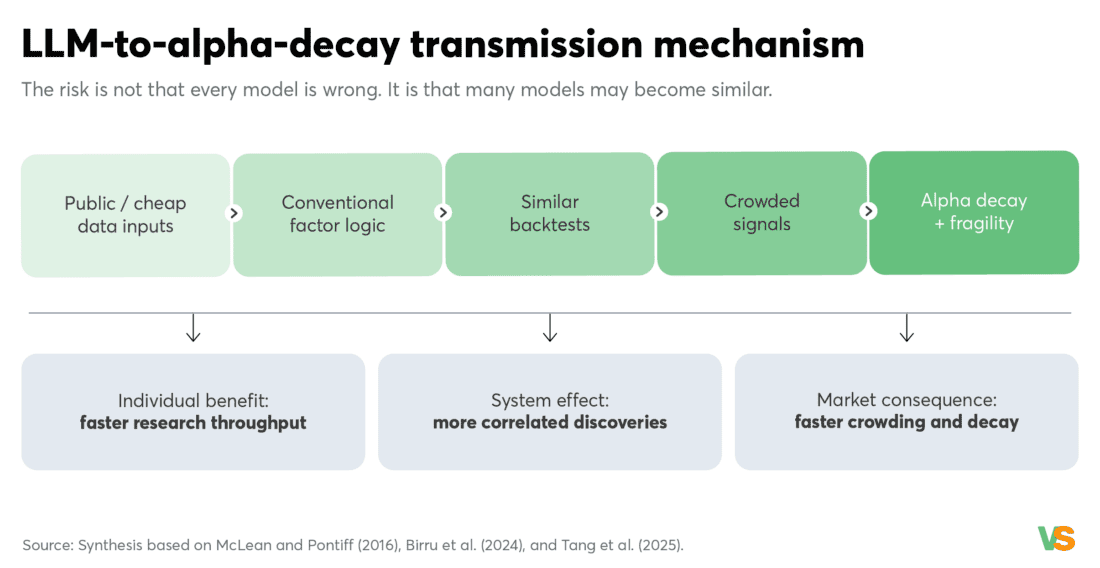

LLMs might accelerate alpha decay in trading. The mechanism is not mystical, and it does not require assuming that AI systems are better investors than humans. It only requires a more modest assumption: many users will ask similar models similar questions, use similar public data, trust similar top-of-mind indicators, and fit similar backtests. The result can be faster research throughput for each participant, but also a more homogeneous research frontier in aggregate.

This matters because alpha is not just discovered; it is competed away. A trading signal with a clear economic rationale, low implementation friction, and broad visibility can move through a life cycle: discovery, replication, capital allocation, crowding, decay, and sometimes a residual risk premium. LLMs can shorten the path from discovery to replication. For strategies built on public data and conventional factor logic, the edge may be harvested faster and exhausted sooner.

This article focuses on alpha decay rather than volatility. The two are related. If many players converge on the same trade, expected returns can fall as capital arrives. The same crowding can also make the remaining trade more fragile when positions are unwound together. But alpha decay is the first-order research problem: if copyable signals now spread faster, the operating model for systematic trading has to change.

Figure 1. LLM-to-alpha-decay transmission mechanism. Source: Synthesis based on McLean and Pontiff (2016), Birru et al. (2024), and Tang et al. (2025).

The strongest evidence starts before the LLM era. Bowles, Reed, Ringgenberg, and Thornock study when anomaly returns actually occur around the release of accounting information. Their Journal of Finance paper, Anomaly Time, finds that anomaly returns are concentrated in the first month after information release dates and decay soon thereafter [1]. This is important because it reframes many anomalies as information-processing opportunities rather than permanent structural premiums.

A follow-up paper from the same author group pushes the timing problem even earlier. Predicting Anomalies shows that anomaly signals derived from financial data can themselves be predicted before the formal signal is released. A trading strategy based on predicted anomaly signals earns 2.80% annualized in the quarter before release, and the authors report that recent returns are increasingly earned several quarters earlier [2]. That is a life-cycle story: pre-release anticipation, a short post-release monetization window, and then decay.

Figure 2. The anomaly life cycle around information release. Source: Bowles et al., Anomaly Time; Bowles et al., Predicting Anomalies.

The classic benchmark is McLean and Pontiff. They study 97 return predictors and find that portfolio returns are 26% lower out-of-sample and 58% lower after publication. The 32 percentage-point gap is interpreted as a lower-bound estimate of publication-informed trading. They also document higher correlations among published-predictor portfolios after publication [3]. In plain English: once an anomaly becomes known, it is more likely to be traded, and more likely to behave like other known anomalies.

Marrow and Nagel add a real-time lens. They track prominent return-based anomalies as a hypothetical Bayesian researcher would, updating beliefs through time. Their conclusion is that many prominent anomalies weaken substantially around their publication dates, suggesting a decline in ex-ante expected returns rather than merely a statistical artifact [4]. Brogaard, Nguyen, Putnins, and Zhang point to a complementary channel: anomaly decay appears to occur primarily around structural increases in market liquidity, with liquidity changes explaining a large share of decay relative to publication and general market changes [5].

Figure 3. Normalized return predictability around publication. Source: McLean and Pontiff (2016).

LLMs change the research stack because they reduce the cost of translating an idea into code, tests, documentation, and variations. That is useful. But for copyable alpha it also creates a crowding channel. A large share of model-assisted research will begin with public price history, public financial statements, familiar technical indicators, common factor libraries, standard portfolio sorts, and familiar train-test splits. The research output can look diversified in code while remaining similar in economic logic.

The LLM-for-trading literature recognizes this problem. The 2025 AlphaAgent paper argues that LLM-based alpha mining can rely too heavily on existing knowledge, producing homogeneous factors that worsen crowding and accelerate decay [10]. That sentence is unusually direct. The risk is not simply that an LLM hallucinates bad code. The deeper risk is that it produces plausible, well-written, highly conventional code that many other users can also produce.

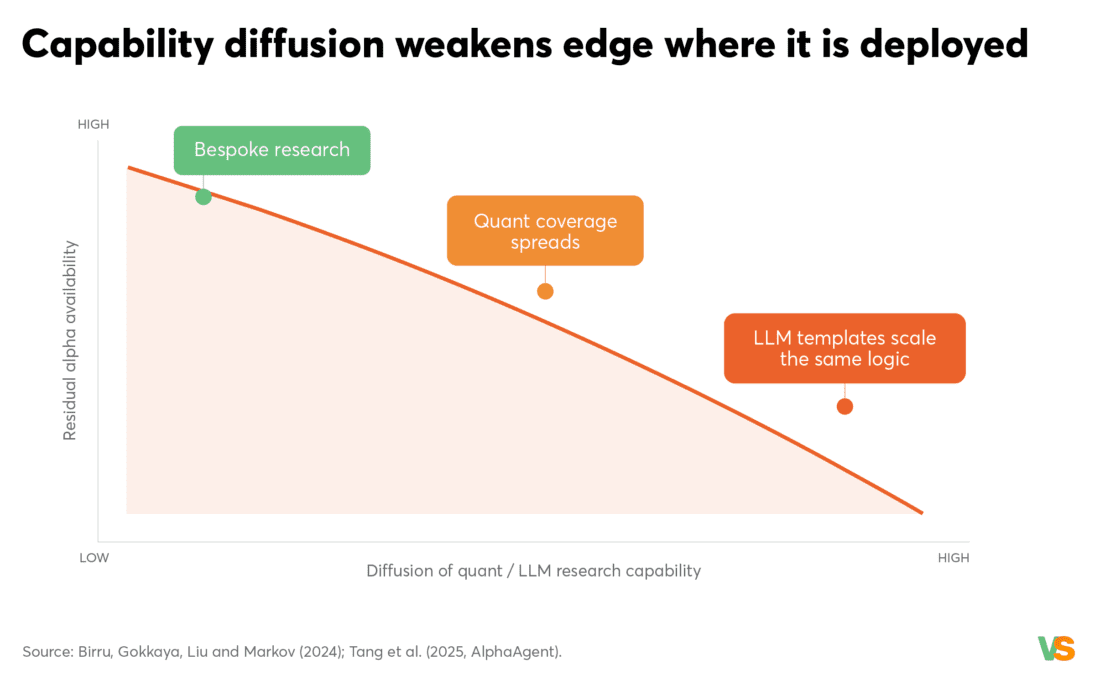

There is also a pre-LLM precedent. Birru, Gokkaya, Liu, and Markov find that analysts and mutual fund clients with greater access to Quants make recommendations and trades that reveal greater knowledge of anomalies. More importantly, cross-sectional return predictability is weaker in stocks with higher quant-linked analyst coverage or mutual-fund ownership, and strengthens when brokerage closures reduce access to Quants [6]. If concentrated quant capability weakened anomalies where it was deployed, broad LLM-assisted capability could plausibly do the same for the most accessible signals.

Figure 4. Capability diffusion weakens edge where it is deployed. Source: Birru et al. (2024); Tang et al. (2025).

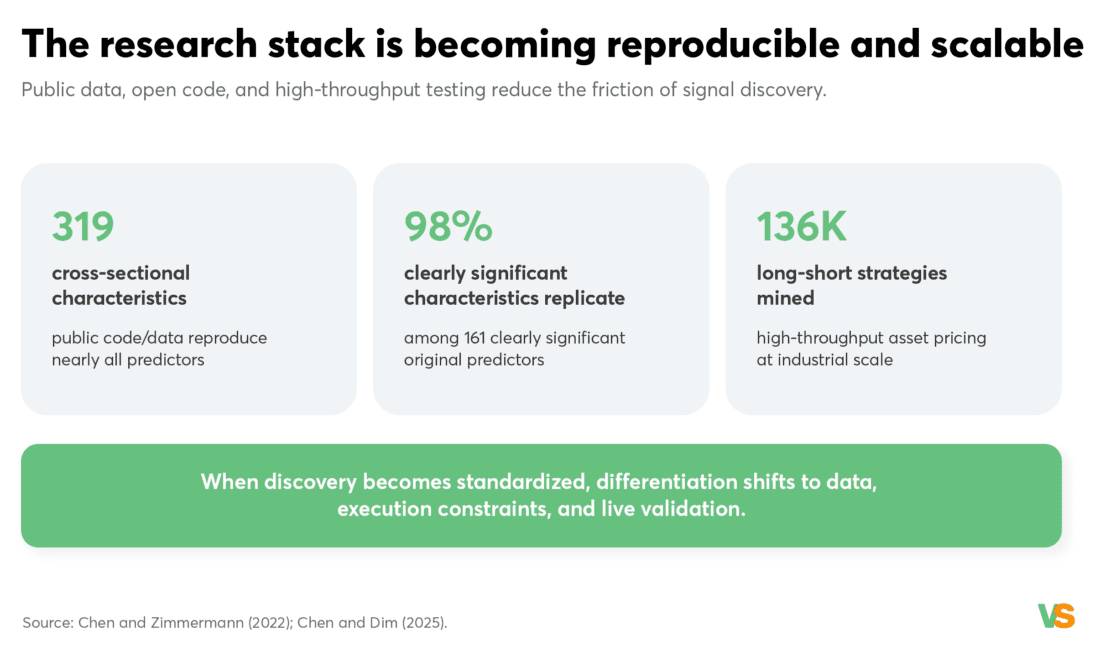

Two additional papers show why the LLM effect could be powerful. Chen and Zimmermann provide public data and code that reproduce nearly all cross-sectional stock-return predictors across 319 characteristics; for the 161 characteristics that were clearly significant in the original papers, 98% of their long-short portfolios have t-statistics above 1.96 [7]. Chen and Dim then mine 136,000 long-short strategies from accounting ratios, past returns, and ticker symbols, showing that high-throughput asset pricing can match the out-of-sample performance of top journals [8].

This is not an argument that backtests are useless. It is a warning about what backtests measure. Martin and Nagel show that in high-dimensional settings, standard in-sample tests can reject no-predictability with high probability even when investors use information optimally in real time; out-of-sample tests retain the economic meaning [9]. In an LLM environment, where a user can generate thousands of variations quickly, this warning becomes more important. The bottleneck is no longer idea generation. The bottleneck is evidence quality, implementation realism, and differentiation.

Figure 5. Public data and high-throughput research make signal discovery more scalable. Source: Chen and Zimmermann (2022); Chen and Dim (2025).

Crowding is not just a return problem. Chincarini, Lazo-Paz, and Moneta find that anomaly risk-adjusted returns are primarily generated by the most crowded long-leg stocks and the least crowded short-leg stocks, and they argue that crowding adds crash-risk considerations to anomaly investing [11]. This means that the remaining alpha in a crowded trade can be more conditional, more capacity constrained, and more exposed to unwind dynamics.

For practitioners, the issue is not whether LLMs will eliminate alpha. They will not. Private information, better data engineering, differentiated feature construction, execution quality, and portfolio design still matter. The issue is that public, familiar, easily prompted alpha may have a shorter half-life. A signal that looks attractive in a simple historical backtest may already be near the end of its economic life by the time it becomes popular enough to be requested, coded, and shared widely.

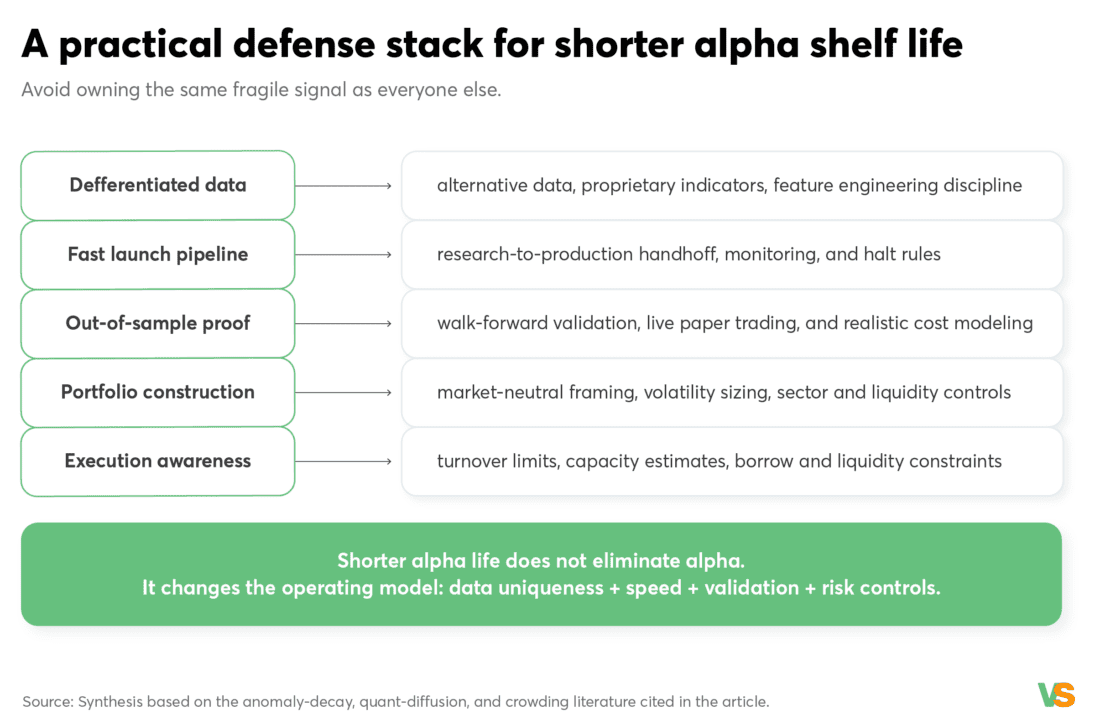

The response is not to avoid AI. The response is to build a research process that assumes faster decay. First, accelerate the research-to-launch pipeline, but pair it with strict monitoring and halt rules. If alpha windows are front-loaded, speed matters; if alpha decays quickly, exit discipline matters even more. Second, reduce dependence on public-factor templates. Alternative data, proprietary indicators, cleaned data layers, and domain-specific feature engineering become more valuable when generic signal discovery becomes cheaper.

Third, make portfolio construction part of the edge. Market-neutral design, beta control against an SPX or index-futures framework, sector and industry constraints, volatility-based position sizing, turnover limits, and realistic execution costs can decide whether a signal survives contact with live trading. Fourth, treat out-of-sample evidence as the minimum standard. Walk-forward tests, live paper trading, small-capital pilots, and capacity analysis should matter more than elegant in-sample t-statistics.

In short: launch faster, but trust slower. LLMs can help generate candidates, code tests, document assumptions, and monitor decay. They should not be allowed to turn a familiar public-data workflow into a false sense of originality.

Figure 6. Practical defense stack for shorter alpha shelf life. Source: Synthesis based on the cited anomaly-decay, quant-diffusion, and crowding literature.

The likely future is not an alpha-free market. It is a market in which easily described alpha becomes more perishable. LLMs make research faster, but speed is a double-edged sword: it helps individual teams discover and implement ideas, while also helping competitors converge on the same ideas. For copyable alpha, the scarce resource shifts from basic signal discovery to differentiated data, robust engineering, validation discipline, execution realism, and portfolio construction.

The practical implication is simple. Do not compete in the most crowded lane of the research stack. Use AI to move faster, but build the data and validation infrastructure that prevents the strategy from becoming just another public-factor clone.

Visit Visual Sectors for info on data processing via API and MCP access.

Selected references

| [1] Bowles et al. (2024), Anomaly Time. Link | [5] Brogaard et al. (2023), What Drives Anomaly Decay? Link | [9] Martin and Nagel (2022), Market Efficiency in the Age of Big Data. Link |

| [2] Bowles et al., Predicting Anomalies. Link | [6] Birru et al. (2024), Quants and Market Anomalies. Link | [10] Tang et al. (2025), AlphaAgent. Link |

| [3] McLean and Pontiff (2016), Does Academic Research Destroy Stock Return Predictability? Link | [7] Chen and Zimmermann (2022), Open Source Cross-Sectional Asset Pricing. Link | [11] Chincarini et al., Crowded Spaces and Anomalies. Link |

| [4] Marrow and Nagel (2024), Real-Time Discovery and Tracking of Return-Based Anomalies. Link | [8] Chen and Dim (2025), High-Throughput Asset Pricing. Link |

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Visual Sectors and is being posted with its permission. The views expressed in this material are solely those of the author and/or Visual Sectors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!