- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 30, 2026 at 11:15 am

We spent last week traveling in Austria with friends. The impact of the Iran War felt closer – and not just because an Iranian missile could theoretically hit Vienna. This part of the world is highly energy dependent. They rely on imports for just over half of their primary energy, and about the same share of their natural gas, with the US being the biggest provider. Half of its electricity comes from hydropower.

We saw wind turbines covering the countryside on a day trip to Bratislava. Wind provides about 12% of Austria’s power. However, since electricity is only 11-12% of their primary energy, wind is around 2.5% of that. Like most countries, they’ve found that it’s easier to increase renewables than to boost electrification.

EVs were often seen in Vienna, but we didn’t see any of the 3,000 charging stations operated by Wien Energie. Electricity prices are 80% higher than the US average and double Florida’s, unburdened as it is by blue state policies.

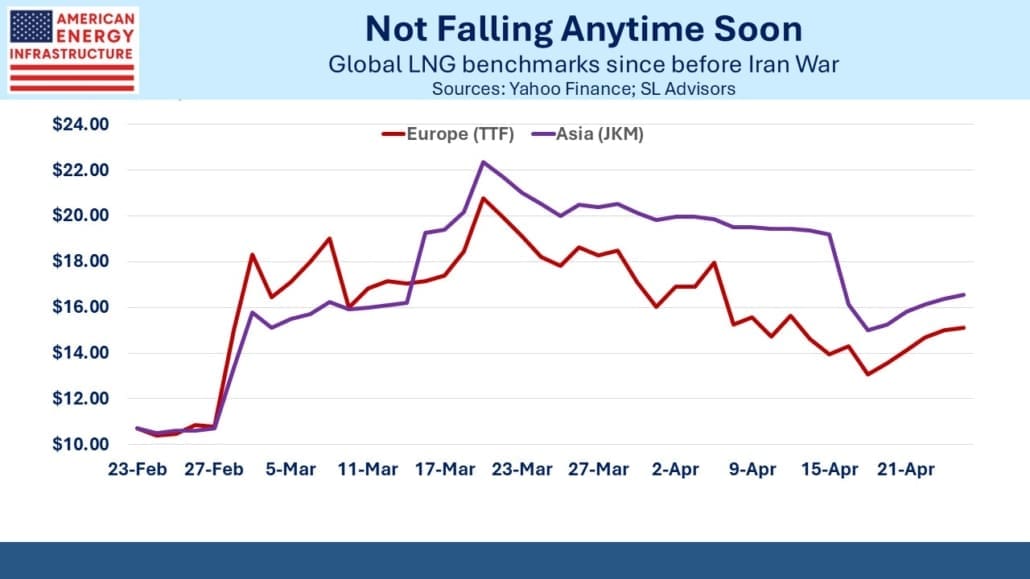

Europe is feeling the effects of the Iran War more keenly than the US, where the most visible impact has been to push gasoline above $4 per gallon. Globally, natural gas prices moved higher again last week and now sit halfway between their pre-war level and the highs reached in early March. Crude oil has similarly pulled back from its highs earlier last month, although spot transactions are at $20 or more per barrel above front month futures.

Europe is feeling the loss of LNG shipments from Qatar. Increased US deliveries have helped but only to a point. Industrial production, already in long term decline due to green energy policies, has suffered further. Voluntary energy saving measures are common across Europe. The EU has recommended countries reduce highway speed limits by at least 10 kph, but so far governments are relying on moral suasion to lower energy consumption.

Europe’s dysfunctional energy and security strategies are elegantly combined in the news that Russia has stopped sending crude oil from Kazakhstan to a refinery just outside Berlin, because Germany is Ukraine’s largest arms supplier. The PCK refinery supplies 90% of the region’s gasoline, jet fuel and heating oil.

The operations of PCK were taken over by Germany from Russia’s Rosneft as punishment for the invasion of Ukraine. Nonetheless, oil continued to flow since it suited both countries. The recent jump in prices has boosted Russia’s oil revenues, evidently allowing them to be more selective about whom they supply.

German policy, and by extension EU policy, has been to rely on Russia for energy and the US for protection from Russia. They need to revise their thinking.

Poland’s leader recently wondered, “…whether US is ‘loyal’ to Europe’s defense” a question which would prompt most Americans to ask what we’re getting in return.

Financial markets remain sanguine about the closure of the Strait of Hormuz. The economic pain is spreading. Beyond the obvious loss of oil and gas shipments, fertilizer and sulfuric acid are among those vital products whose prices have risen sharply. Sulfur is widely used in the production of fertilizer.

However, neither the US nor Iran seems motivated to open the Strait up. It’s increasingly clear that both countries would need to agree for normal shipping traffic to resume.

US farmers, who are generally in red states, are grumbling. Political commentators think unencumbered energy trade must resume before Memorial weekend to avoid having an impact on November’s midterms, but the US economy has as many winners as losers from elevated oil. This is the message from the stock market.

Kinder Morgan (KMI) kicked off pipeline earnings with a solid report last week, beating expectations in each business segment. Management raised full year EBITDA guidance by 3%.

The challenge for KMI’s peers may be meeting heightened forecasts from sell-side analysts. KMI now expects US natural gas demand to reach 150 Billion Cubic Feet per Day (BCF/D) by 2031, driven by LNG exports and data centers. The Energy Information Administration expects 110 BCF/D of demand this year.

In the same vein, the INGAA Foundation which advocates for the natural gas industry believes the US will need to add 70 BCF/D in new pipeline capacity by 2050. Gas is a growth business.

—

Originally Posted April 26, 2026 – More Pain Over There Than Here

Please go to following link for important legal disclosures: https://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

{kind=link}

{kind=link}

{kind=link}

I’m puzzled as to why the climate crowd aren’t out dancing in the streets singing the praises of President Trump. He has prevented millions and millions of tons of carbon from enterIng the atmosphere by simply working together with Iran to close the Strait of Hormuz. Where is Al Gore? Get your voters out to be sure Republicans keep control of congress so that Mr. Trump can continue the good work.