- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 30, 2026 at 11:00 am

In 1817, a young Swedish chemist, Johan August Arfwedson, was analysing a mineral called petalite when he identified a new element. He named it lithium, from the Greek word lithos, meaning stone, because unlike sodium and potassium, it was discovered in rock rather than plant ash. It turned out to be the lightest metal on the periodic table. Light but quick to react even with water, lithium has always ignited curiosity in the laboratory1.

Two centuries later, that same element sits at the heart of a very different revolution. Lithium is the backbone of the modern rechargeable battery. From electric vehicles (EVs) and grid storage to smartphones and data centres, it quietly powers the electrification and digitalisation of our world.

As economies push to decarbonise, digitise, and electrify, lithium’s strategic importance is rising rapidly. Demand is expected to grow strongly, while supply could tighten relative to that demand in the years ahead. In this blog, we outline the key demand and supply forecasts for lithium and what they could mean for investors.

Demand for lithium is expected to rise

The International Energy Agency’s (IEA) Stated Policies Scenario, in other words, its base case which projects the future based on currently stated policies globally, forecasts a notable increase in demand for lithium.

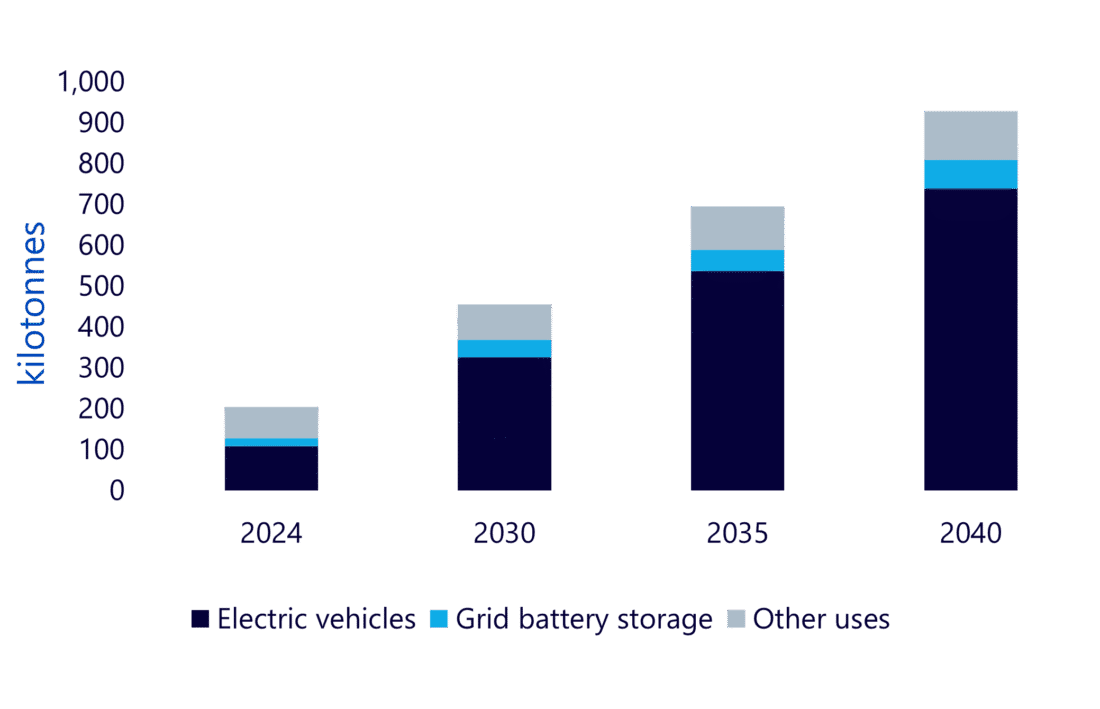

Figure 1: Total demand for lithium in the IEA’s base case

Source: International Energy Agency (IEA), May 2025. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

We can make three key observations from the graph. First, electric vehicles are the dominant driver of growth. Lithium-ion batteries sit at the heart of both battery electric vehicles and plug-in hybrid electric vehicles, and as EV penetration rises, so too does lithium demand. Wood Mackenzie estimates that rechargeable batteries account for around 90% of global lithium demand in 2025, with the automotive sector representing the majority of that share2. Demand is also shaped by evolving battery chemistries, including strong growth in lithium iron phosphate (LFP) and high-nickel cathodes3. In short, the electrification of transport is the single biggest force shaping lithium markets.

Second, grid battery storage is also a growing segment. As renewable energy capacity expands, energy storage systems are increasingly needed to balance power grids and smooth intermittency. Wood Mackenzie expects annual energy storage systems installations to grow by nearly 60% between 2025 and 20304. More renewables mean more storage, and more storage means more lithium.

Third, there is an ‘other uses’ category which is, quite clearly, significant. Lithium is used in portable electronics, power tools, industrial applications such as ceramics and glass, and a range of specialised products. Steady growth is expected across this segment of lithium demand as well.

Lithium, therefore, has a crucial role to play not just in transport, but across the broader electrification and digitalisation of the global economy.

Supply is expected to tighten and remain concentrated

The IEA’s base case on supply makes the analysis of market dynamics even more revealing.

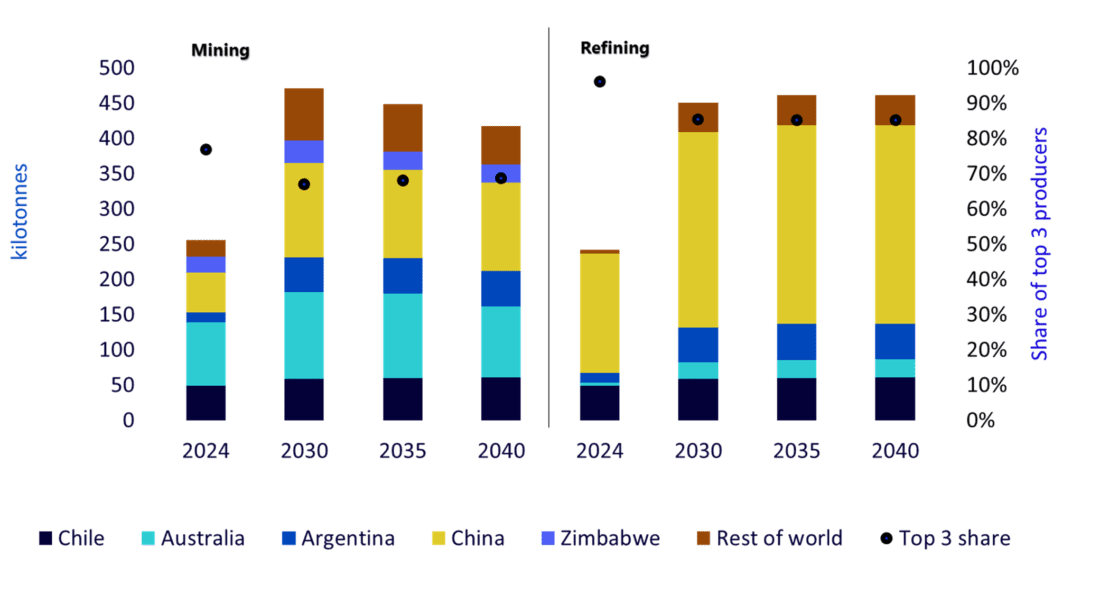

Figure 2: Lithium supply from existing and announced projects in IEA’s base case

Source: International Energy Agency, May 2025. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

Again, from the chart, we can make three key observations. First, supply growth slows meaningfully over time. While the market has seen exceptional expansion in recent years, Wood Mackenzie notes that lithium extraction grew at a 31% compound annual growth rate between 2020 and 2025 but is expected to slow to 6% over the longer term to 20355. This is because known resources would have been discovered and developed resulting in the plateauing in extraction. In other words, after a period of rapid buildout, supply growth begins to slow down just as demand continues to rise. In commodity markets, such deceleration is where tightness begins to emerge.

Second, supply remains concentrated in a handful of countries. On the mining side, Australia and China are expected to maintain dominance, even as their relative shares shift over time. In addition to hard rock mining, lithium is also extracted from salt-rich underground water reservoirs known as brines, particularly in South America. Chile, Argentina and China account for the majority of this brine production6. This concentration means that disruptions, policy shifts, or underinvestment in a few regions can have outsized global effects.

Third, refining capacity is also heavily concentrated, particularly in China. Wood Mackenzie highlights that Chinese-based refineries delivered 74% of refined output growth between 2020 and 20257. Although growth is expected to become more geographically balanced in the future, China is still projected to contribute over half of new refining capacity in the near term. As with many strategic metals, control over refining is just as important as control over raw material extraction.

Overall, supply growth is slowing and remains geographically concentrated, creating the conditions under which periods of tightness can become pronounced if demand continues on its projected path.

Closing word

Lithium is the lightest metal on the periodic table, yet it carries the weight of the world’s rapidly rising energy needs on its shoulders. From electric vehicles and grid storage to the devices we use every day, lithium enables electrification, mobility, and digital connectivity.

It does not always dominate headlines in the same way as oil or gold. But as demand rises and supply growth slows and remains concentrated, its strategic importance is becoming harder to ignore. For investors looking ahead to the next phase of electrification, lithium is increasingly central to the conversation.

—

Originally Posted April 28, 2026 – Lithium: the light metal with a heavy impact

1 International Lithium Association, 2023.

2, 3, 4, 5, 6, 7 Wood Mackenzie, Global lithium investment horizon outlook, Q4 2025.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!