- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 30, 2026 at 1:07 pm

Stocks are poised to close out their best month since April even as artificial intelligence enthusiasm could be cooling off on the heels of 4 of the 7 magnificents reporting last night, as a sharp pre-open rip was quickly dismissed, sending 3 of those names deep into the red. There’s certainly a long list of reasons for profit-taking at this juncture, especially in consideration of yesterday’s hawkish pause from the Fed alongside a Middle East situation that’s at risk of escalation. Indeed, Wednesday’s interest rate decision featured 4 dissenters, a level of formal disagreement not seen since 1992, as three officials favored a removal of the easing bias in the central bank’s statement in light of significant price pressure risks, while Governor Stephen Miran preferred a cut. Meanwhile, WTI crude remains well above $100 and even eclipsed $110 in the overnight session, as President Trump meets with his cabinet later today to potentially resume military attacks on Iran. But the drop from $110.93 to $105 has quelled the surge in yields that brought the 2-, 10- and 30-year maturities to highs of 3.95%, 4.44% and 5.01%, against the backdrop of a fixed-income complex that is increasingly believing that a hike is more likely than a reduction in 2026. It’s precisely that alleviation in borrowing costs that has investors running to the cyclical Dow Jones and Russell 2000 benchmarks as tech gets battered due to too much capex and not enough cash flow to show for it in the present, generally speaking. The economic calendar was mostly positive with the exception of the inflation numbers which were awful, as the PCE headline and core indices rose to 3.5% and 3.2% in March, however, GDP, unemployment claims and the employment cost index reflected ongoing shopping, robust business investment subdued layoffs and accelerating paycheck gains. In trading, most major equity sectors are appreciating minus tech, communication services, energy and consumer discretionary. Elsewhere, the greenback is weakening, volatility protection instruments are seeing lighter premiums, commodities are advancing except for oil, cryptocurrencies are climbing and prediction markets are catching bids.

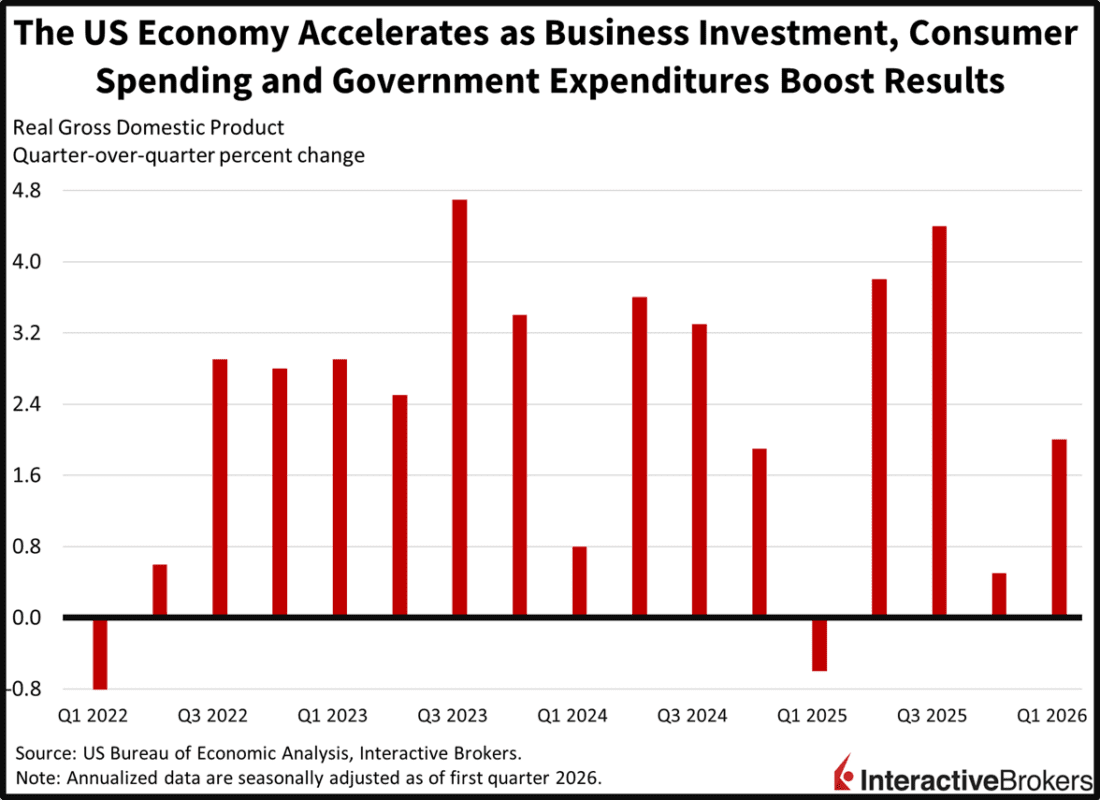

GDP Rebounds as Capex Lifts the Headline

The US economy accelerated in the first quarter after the final period of last year was hampered by the longest government shutdown in history. The 2% growth rate in real Gross Domestic Product (GDP) ramped up from the 0.5% clip in the fourth quarter, although it missed the 2.3% median estimate. The contributors to the 2% expansion included 1.4% from business investment, 1.1% from consumer spending, of which most came from services rather than goods, public sector expenditures offered 0.7% and private inventories pushed up the headline by 0.4%. Conversely, net exports subtracted 1.3%, as imports rose strongly and residential outlays weighed by 0.3%, as elevated mortgage rates continue to hurt construction activity and closings.

PCE Inflation Approaching Double The Fed’s Target

The March report on the Personal Consumption Expenditures (PCE) price index reflected fiercely accelerating cost pressures. The headline and core segments moved up by 0.3% and 0.7% month over month (m/m) and 3.2% and 3.5% year over year (y/y), exactly as expected. The results compare to 0.4% and 0.4% and 3% and 2.8% from February. Last month, prices for nondurables, durable goods and services rose 2%, 1.4% and 0.3% m/m, while the energy segment advanced 11.6% during the period. Real consumer spending rose 0.2% m/m while incomes retreated 0.1%, serving to drop the personal savings rate to 3.6%, its lowest level since October 2022.

Paychecks Expand with Inflation

The employment cost index (ECI) expanded 0.9% quarter over quarter (q/q) in the January to March period, the fast pace of increase in 3 quarters. The result came in ahead of the 0.8% median estimate and the 0.7% from the prior interval. Wages rose 0.8% while benefits increased 1.2% q/q, accelerating from 0.7% and 0.8% in the previous print. Furthermore, the public worker ECI climbed 1% q/q while private sector employees saw a more modest gain of 0.9%.

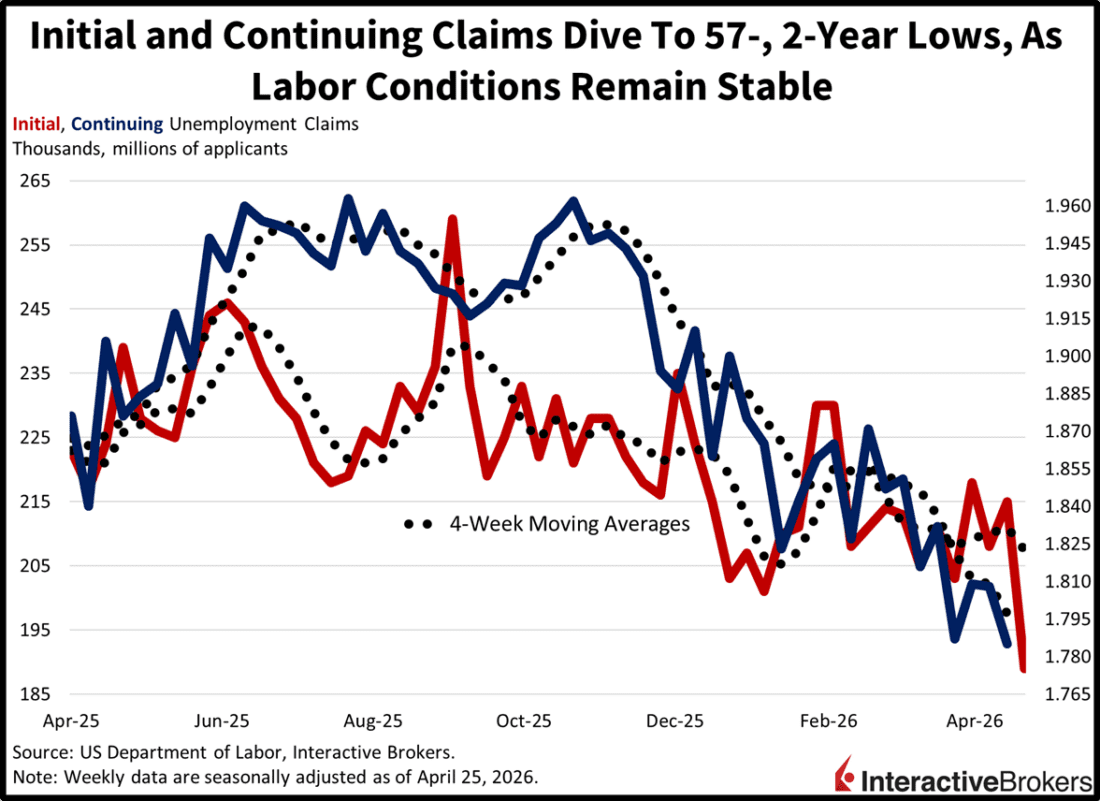

Initial Filings Fall To 57-Year Low

Unemployment claims also supported the view of healthy labor conditions, as initial filings dove to their lowest point going back to 1969 while continuing applications marked a 2-year low. The 189k and 1.785 million figures came in below the expected 215k and 1.820 million during the weeks ended April 25 and 18 as well as the 215k and 1.808 million from the prior prints. Four-week moving averages declined on both fronts to 207.5k and 1.797 million.

Sell In May and Go Away?

With the S&P 500 going on an 861 point rally from the March 30th low at 6,317 to an all-time high of 7,178 reached last Monday, some investors are wondering if the old-school sell in May and go away saying applies here on the final day of April. Meanwhile, it’s precisely the wall of worry that market bulls continue to climb that has paved the way for more upside. Indeed, certain analysts are asking if the war, the associated oil price shock, accelerating inflation and significantly higher interest rates is actually good for stocks, which stands in contrast to the traditional belief that economic fundamentals are important for risk assets. In light of the relentless advance, bears have been starved looking for the smallest of pullbacks, as animal spirits and AI enthusiasm have sparked a party on Wall Street even though macroeconomic risks are severe. What’s especially shocking is that today’s lift is being carried by the cyclically oriented, rate-sensitive aspects of the equity space, and adds further evidence that the bulls seem to have an infinite amount of levers to pull. $100 oil used to be a headwind, but a pullback from $110 to $105 seems to be a tailwind in today’s trading.

International Roundup

The central banks of Europe and the United Kingdom decided to keep their rates on hold today but officials are highly attentive to accelerating cost pressures. Investors have pared back hike odds in 2026, however, as policymakers are worried that tightening their stance could drive the continent into recession. The views from both institutions served to quell global borrowing costs after the Fed meeting yesterday lifted them.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

Market climb despite fear It’s good right now, but it’s not gonna last other words, it’s strong on the surface but unstable underneath big tech is starting to stumble investors want real profits now not just future promises other words good luck AI will continue to be strong, but be careful.

Nicely composed, read the whole thing like it was a conversation in my head. If it weren’t for tax implications, I just might pull the Sell in May and go away“ clever lever. On the other hand, 15% capital gains tax is way better than a 30% loss of equity, twice as “better“ in fact.