- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Latest Webinars

Posted March 26, 2025 at 8:27 am

1/ The Weekly Chart Looks Weak

2/ Growth Sectors Lagging

3/ The Nvidia Bellwether

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

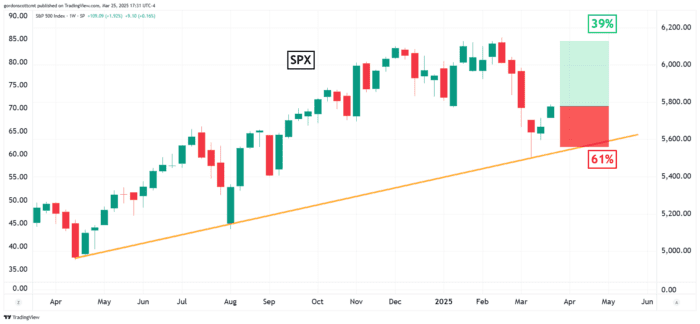

The Weekly Chart Looks Weak

The S&P 500 index (SPX) rose for the second time in as many days this week, giving hope that the frightful spectre of a bear market was all a bad dream in the process of dissipating. While it very well may be so, for now it is worth remembering that the probability of a new bullish trend is a lower probability bet. The reasoning for this can be found in a review of the weekly candle chart for SPX as shown here.

Over the past year the apparent trendline for the upward move (yellow line) has had only two touches. Were a third rendezvous between line and price to occur before earnings season kicks off three weeks from now, it could signal that investors aren’t expecting much from America’s largest corporations.

In fact, if you measure the distance between the most recent high of SPX and the upward trendline during the week after next, what you find is that price has to travel a larger distance to get to a new high than it does to break below the trendline. If you hypothesize that market prices move in randomized ways, then you arrive at the conclusion there is a 61% chance that the trendline will be broken before a new high is printed by SPX.

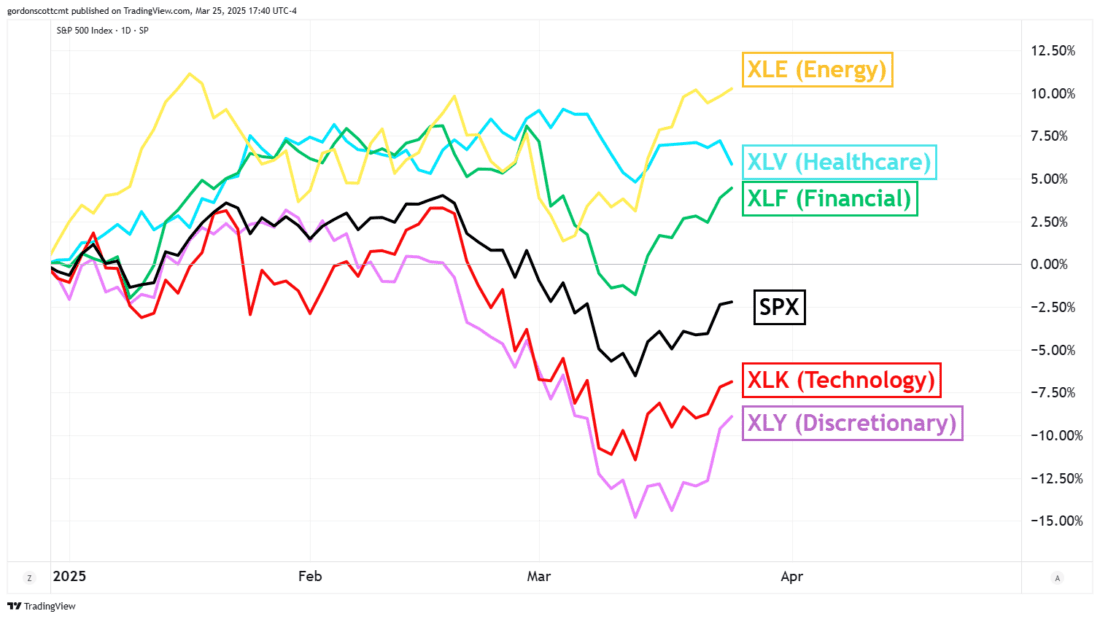

Growth Sectors Lagging

It’s not hard to find more market data to support this idea. One place to look might be the relative performance of sectors (see chart).

Defensive sectors such as Consumer Staples, Utilities and Healthcare are often thought to outperform the rest of the sectors in the event of a bear market. Stocks in these sectors often have lower beta and pay larger dividends.

Right now only Healthcare shows up among those three sectors as a leader. That it is accompanied by Energy and Financials speaks to the market’s fascination with tariffs, inflation and the Fed’s responsive interest rate policy more than anything else.

Meanwhile the two sectors lagging the index, Technology and Consumer Discretionary, are typical candidates for the sectors that should be leading in a bear market. So the stage is nearly set for prices to fall.

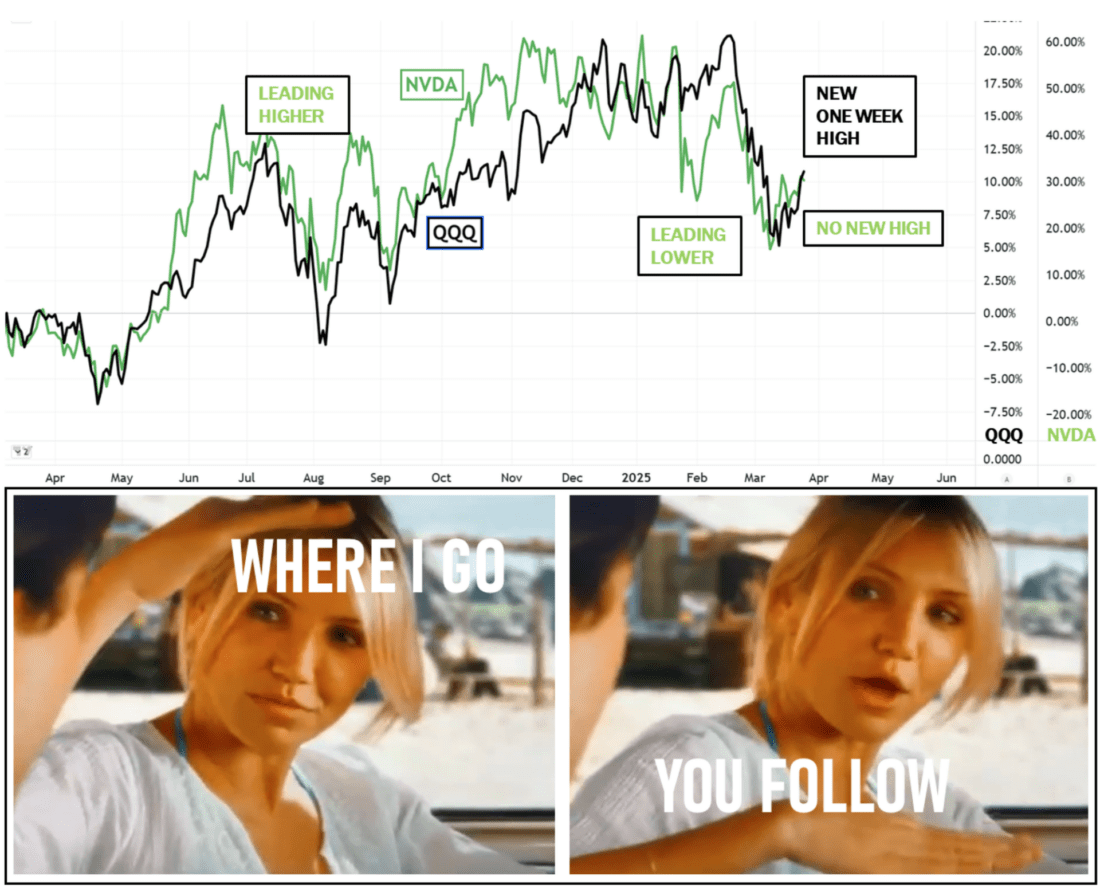

The Nvidia Bellwether

Nvidia (NVDA) share prices had risen 60% at their peak in the last twelve months. The share price has given back half of those gains since the beginning of the year for a number of reasons, not the least of which is the revaluation of the money other corporations are likely to spend on the companies chips as part of their AI implementations.

NVDA has fallen to the number three position in Invesco’s Nasdaq 100 ETF (QQQ) behind Apple (AAPL) and Microsoft (MSFT) for its market cap size. The larger the market cap of a stock, the larger percentage of it is held by the QQQ fund. The Invesco fund has nine percent of its holdings in NVDA shares, and that makes it an influential bellwether leading QQQ around wherever it decides to go as can be seen in the chart below.

Clear as night and day, NVDA shares led the market higher on the way up, and more recently, have led QQQ southward like June led Roy at the end of that movie (you know the one). Even more telling is that in the past few days, while QQQ has pushed to a higher peak, NVDA has not. Can Roy really go on without June?

—

Originally posted 26th March 2025

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

April and May still to come before June. My guess is, shotgun wedding early May.