- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 23, 2026 at 1:06 pm

Stocks are advancing further as Beijing lightened its stance on US semiconductor imports by communicating that firms can arrange for purchases of Nvidia H200 chips. The news is essentially saving the day for equities, since the broadening trade is buckling this session following significant year-to-date outperformances from the cyclically oriented Dow Jones Industrial and Russell 2000 benchmarks relative to the S&P 500 and Nasdaq 100 indices. Not even supportive economic data were able to bolster the reacceleration theme, as a historic upward revision to UMich sentiment sent the gauge to a five-month high. Meanwhile, flash PMIs signaled that the cycle remains on solid footing, as the services and manufacturing sectors are firmly in expansion territory although they slightly missed expectations. On the geopolitical front, commodities are soaring as President Trump ordered an Armada of American ships to the Middle East as a result of intensifying protests around Tehran. In response, gold and silver reached fresh records once again on safe-haven demand, with the former inching closer to the $5k level while the latter exceeded $100 for the first time ever. Natural gas and crude oil are additionally catching ferocious bids on the potential for disrupted supplies stemming from a powerful winter storm expected to hit the Northeastern US or from a military grapple near Iran. Treasuries are generally unchanged, as their defensive characteristics are offset by inflation uncertainty driven by a possible sustainable lift in energy costs. Elsewhere, the greenback is lower and volatility protection instruments are pretty flat while prediction markets and cryptocurrencies are seeing investor interest.

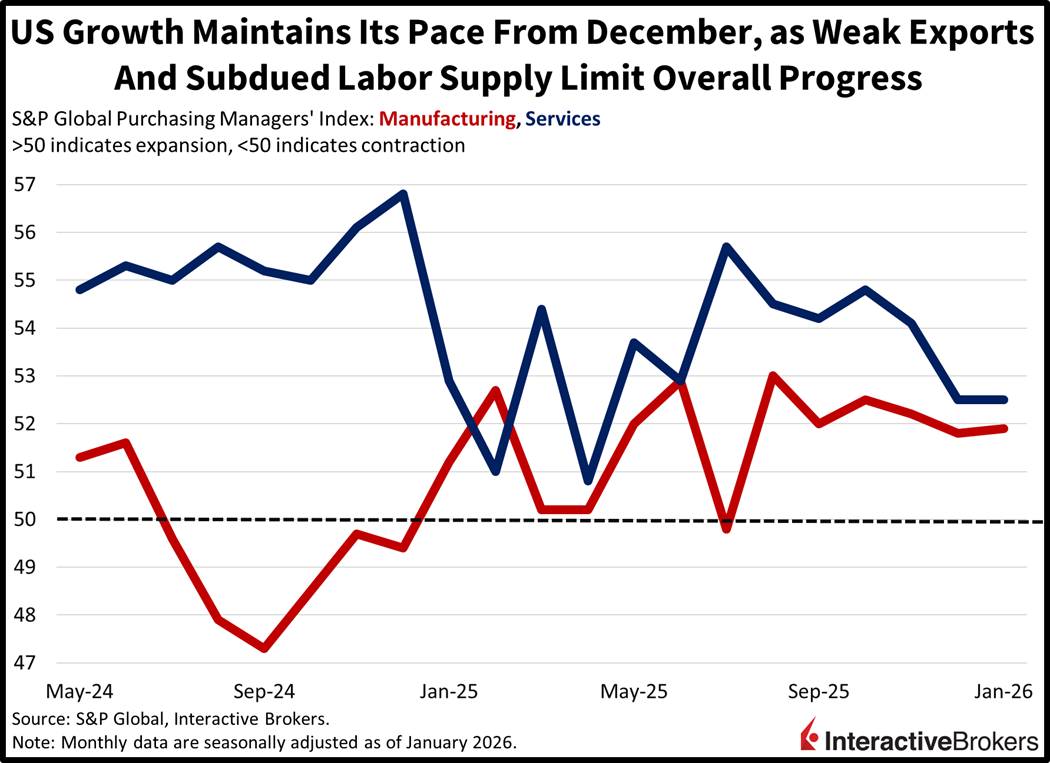

This morning’s flash Purchasing Managers’ Indices (PMI) from S&P Global pointed to solid conditions across the economy. The services and manufacturing sectors delivered scores of 52.5 and 51.9 for this month, unchanged from December on the former but higher than the previously reported 51.8 on the latter. The figures did miss estimates of 52.8 and 52; however, they exceeded the expansion-contraction threshold of 50 by wide margins. Strong confidence, continued demand and modest hiring supported activity in both segments, although firms were worried about geopolitics, affordability and tariffs. Also, labor supply issues weighed on payroll additions as companies had trouble filling vacancies with qualified candidates. Finally, exports were a major drag to start the year.

The University of Michigan’s (UMich) Consumer Sentiment Index was upwardly revised to 56.4 following an initial read of 54, as households lightened their inflation expectations. Indeed, the most optimistic reading in five months was bolstered by downwardly adjusted price pressure projections over 1- and 5-years, which sank from 4.2% and 3.4% to 4% and 3.3%. Still, elevated costs and softening labor conditions continued to stress amongst shoppers.

President Trump has started 2026 similar to 2025, as he adopts a foreign police posture with allies and adversaries alike around the world. And as we head into this weekend, equity investors are hesitating to add much incremental risk to portfolios in light of the potential for Greenland volatility to be replaced by Middle East turbulence. Still, over the long run, geopolitics aren’t a huge determinant of stock prices; however, they can cause significant hiccups, like Russia’s invasion of Ukraine in 2022, which contributed to a down year as the Fed had to hike in a rush to subdue the event’s substantial contribution to global inflation via soaring energy costs. Furthermore, fundamentals and the cycle remain solid, but earnings expectations have started to decline modestly, and that’s a key factor to watch as we progress through the fourth year of a terrific bull market that has delivered three consecutive annums of robust gains.

The HCOB Flash Eurozone PMI from S&P Global was unchanged in January at 51.5 with a slight improvement in manufacturing being offset by softness in the services sector. The manufacturing gauge climbed from 48.8 to 49.4, a two-month high, but stayed below the contraction-expansion threshold of 50. Manufacturing output, however, went from 48.9 to 50.2. At the same time, the Flash Eurozone Services PMI Business Activity Index fell from 52.4 to 51.9, hitting a four-month low.

Within the Composite gauge, output grew in response to a modest uptick in new orders despite weaker demand from foreign customers. Employment was scaled back slightly, primarily a result of a declining workforce in Germany. Even with reduced labor, businesses were able to work down their backlogged orders. In other matters, both input and output prices were higher. Input price increases were the most notable in manufacturing. Looking ahead, business sentiment about the future, including output, climbed to a 20-month high.

The Bank of Japan delivered a hawkish message when announcing its widely expected decision to maintain its key interest rate at 0.75%. Only one central banker pitched raising the rate with a proposed 25 basis point bump. Conversely, Japan Governor Kazuo Ueda implied that the next rate hike could occur in April.

Members expressed the following reasons for their restrictive outlook:

The bank also said it expects gross domestic product (GDP) to have increased 0.9% in 2025 and projects an expansion of 1% this year. In October, it estimated GDP for both of those periods would be 0.7%.

The Japan Flash Composite PMI Output Index hit 52.8 this month, up 1.7 points from December with both services and manufacturing improving. The Services PMI went from 51.6 to 53.4 while the manufacturing gauge hit 51.5 after December’s 50 score.

New orders increased, resulting in a record jump in outstanding work, which prompted companies to increase hiring at the greatest pace since early 2019. Demand from foreign buyers for Japanese products and services also climbed. It was the first uptick since last March. Conversely, input inflation was still strong, having eased only slightly from the eight-month high in December. Within this metric, price pressures slowed in the services sector but accelerated in manufacturing. Companies passed loftier labor costs and input expenses to customers by increasing their gate prices at the fastest rate in 20 months. The growth in orders and the corresponding ability to increase prices didn’t improve sentiment, with business’ 12-month outlook falling to the long-term average. Businesses expressed concerns about rising costs, the global economy and the availability of labor.

UK consumer spending volumes were 0.4% higher month over month (m/m) in December, but the final quarter of 2025 saw a 0.3% decline relative to the three-month period ended in September, according to the Office for National Statistics. The December m/m result exceeded the economist consensus estimate for a flat month after purchase volumes slipped 0.1% in November. December sales, furthermore, were 2.5% higher than in the year-ago period. Economists anticipated a 1% increase after November’s 1.8% year-over-year gain.

Within the m/m print, the following categories and the extent of their changes had the most significant expansions in sales:

Among categories with contracting sales, household goods stores experienced a 3.4% drop followed by a 1.9% decline at department stores.

The S&P Global Flash Uk Composite PMI Index climbed from 51.4 in December to 53.9 for this month, hitting a 21-month high with both manufacturing and services recording faster rates of expansion. The composite exceeded the economist consensus estimate of 51.7 while the manufacturing and services components moved from November’s 50.6 and 51.4 scores to 51.6 and 54.3. Economists anticipated prints of 50.6 and 51.7 for manufacturing and services, respectively. The rate of output growth hit the fastest pace in nearly two years with the services sector experiencing robust activity.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Next week is going to be significant given tech’s earnings releases and the FOMC meeting. Thanks for the insights, Jose.