- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 25, 2025 at 1:09 pm

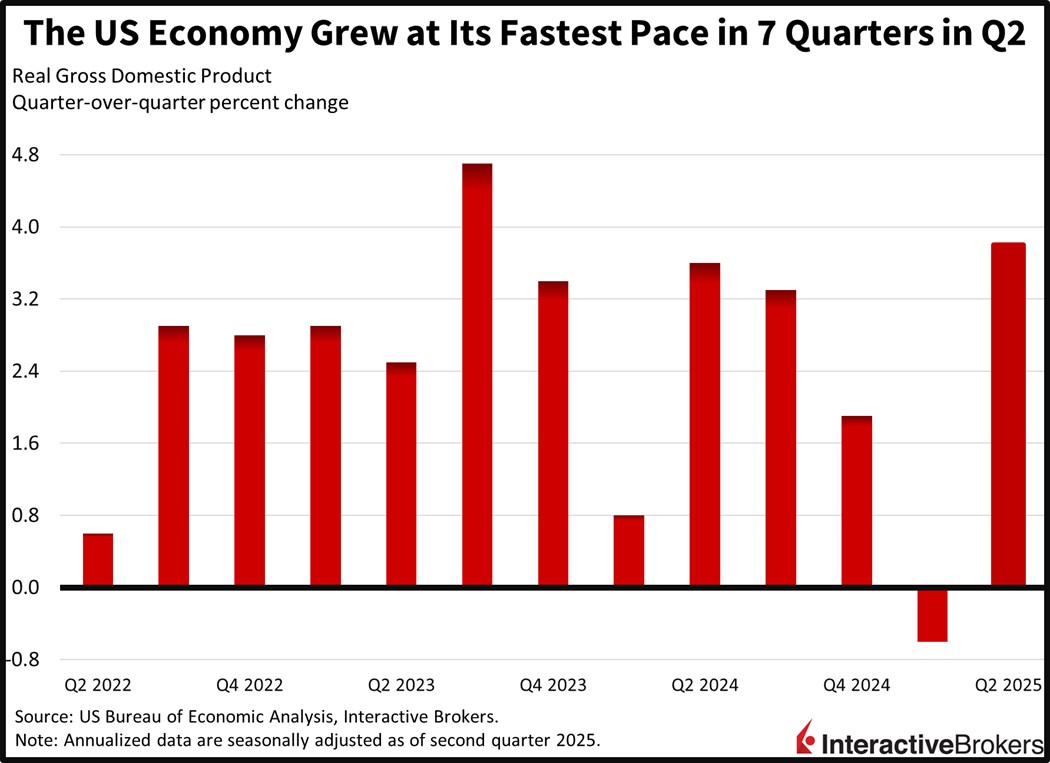

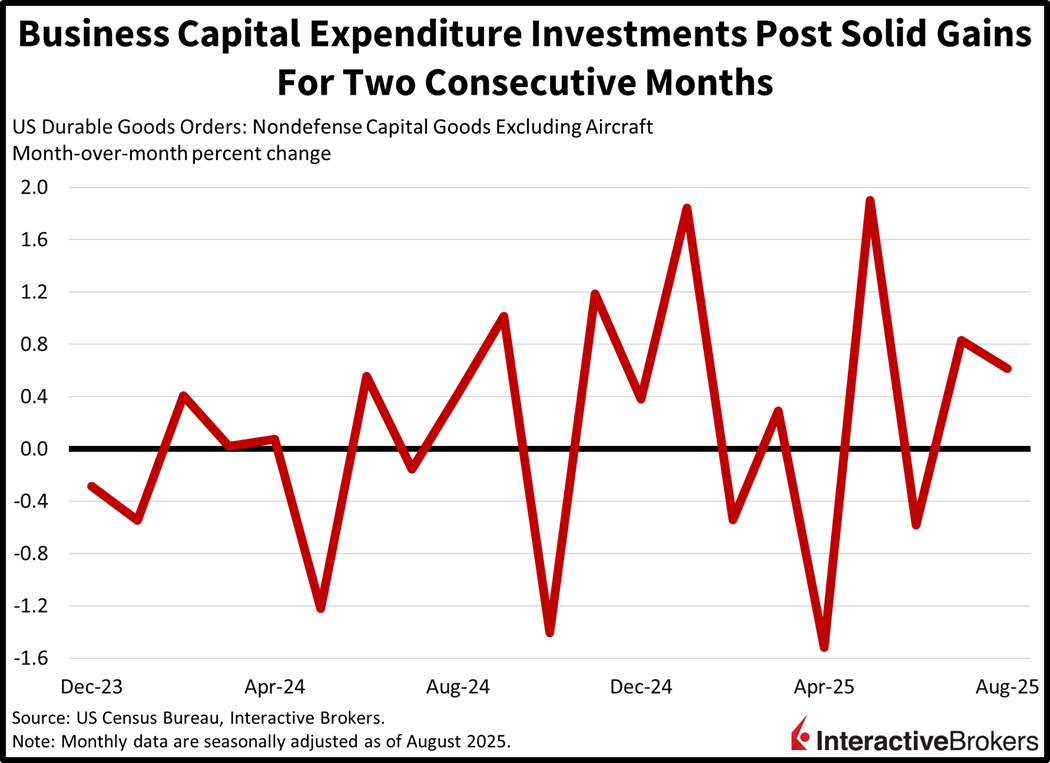

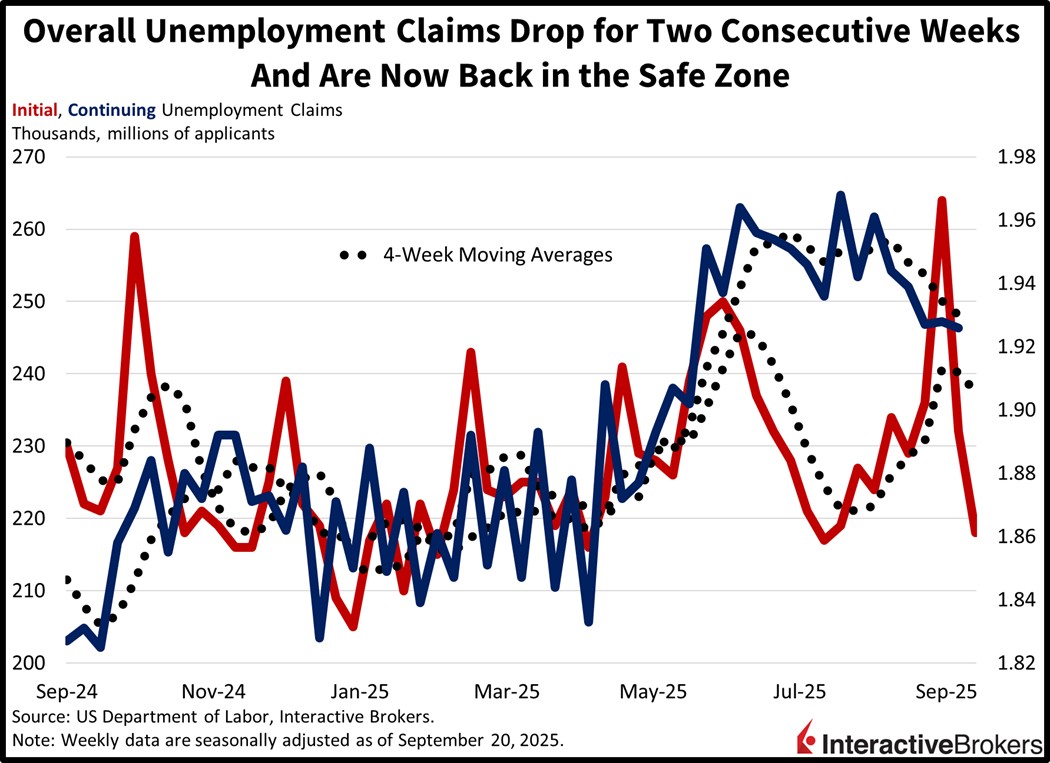

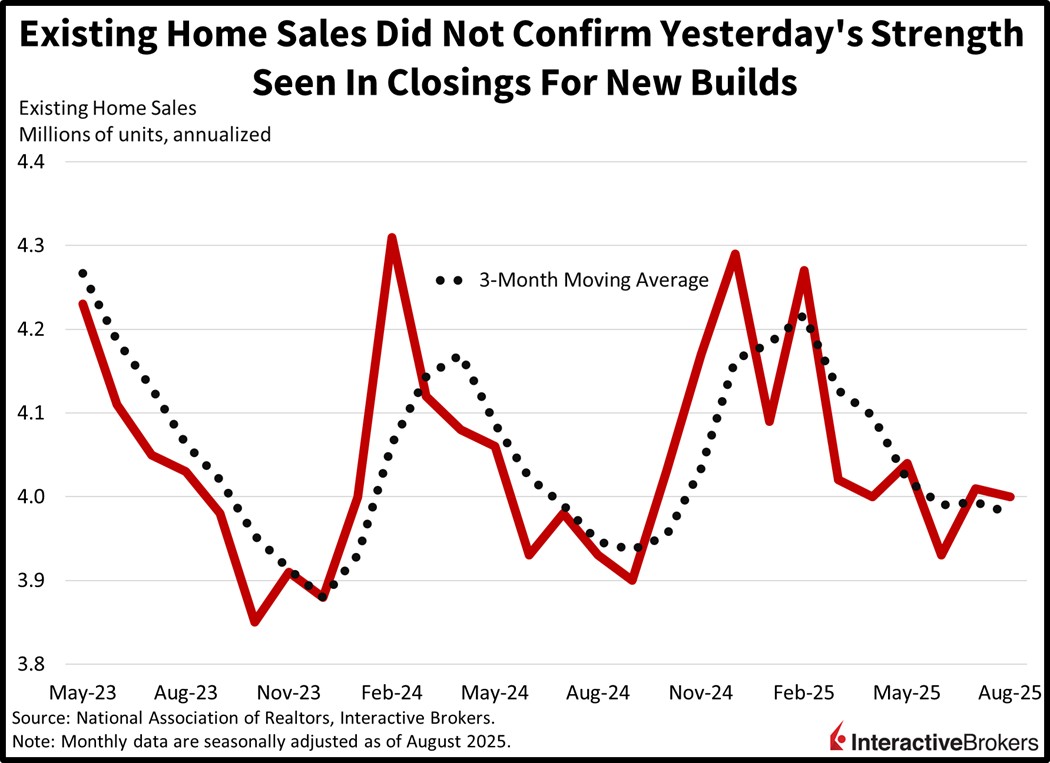

A morning featuring much stronger-than-expected economic data is weighing on Wall Street’s risk appetite, curbing rate cut optimism and sending stocks into modest losses. But equities were even lower closer to the opening bell before investors stepped up to the plate and bought the dips, although fixed-income assets haven’t benefited from a similar kind of rebound due to the numbers being far too robust. The primary driver of loftier yields was a sharp upgrade to second-quarter GDP on the back of buoyant consumers, which brought the pace of advancement to its fastest in almost two years. Then came a ferocious durable goods print, which included momentous business investment as well as voluminous aircraft orders. Meanwhile, a surprise plunge in initial unemployment claims is quelling fears of labor market deterioration. Nonetheless, that too is containing monetary policy accommodation prospects. Additionally, the trade deficit shrunk by more than anticipated while existing home sales posted a beat. Overall, the figures were way too hot for animal spirits to thrive on this Thursday; however, the greenback is gaining on heavier borrowing costs, volatility protection instruments are seeing interest as a result of heightening hedging demand, and the commodity complex is advancing minus copper in light of evidence of a positive cycle. The Treasury curve is ascending in bear flattening fashion led by the shorter tenors, as participants are now confronted with the very real possibility that the Fed may pause in December, considering that another reduction next month sports an 86% probability. Bitcoin is in the red as an incrementally restrictive central bank weighs on liquidity-sensitive cryptocurrencies.

Following a day of terrific economic data that wasn’t pleasant for equity and fixed-income bulls who have been enthusiastic about rate cut prospects, we will end the week with the Fed’s preferred inflation-gauge release tomorrow. The PCE is likely to signal that strong price pressures are being driven by buoyant consumer demand, bolstering services costs, rather than tariff-sensitive goods pushing up charges. Rebounding shoppers in the second half of this year, after a turbulent six months featuring asset volatility and heightened trade uncertainty, are supporting the reacceleration, particularly in discretionary categories like airfares, hotel stays, dining, etc. The print will exceed the central bank’s 2% objective quite handily, but the greatest risk to the economy, financial stability and capital markets today are job losses. When examining policy through a lesser of two evils perspective, it’s important to remember that it took almost seven years, exactly 77 months, to recover from the payroll reductions during the 2008 crisis.

Service costs for Japan businesses climbed 0.2% month over month (m/m) and 2.7% year over year (y/y) last month, according to the Corporate Services Price Index. The m/m rate matched July’s print but the y/y result accelerated from 2.6%. Nevertheless, it was lower than the 2.9% economist consensus estimate. The transportation and postal activities category and the other services group led the m/m trend, with both climbing 0.5%. They were followed by the 0.4% northward movement of the real estate classification. Costs for information and communications services matched the m/m headline but there were unchanged for the finance and insurance category. Conversely, advertising costs sank 2.9%. Among subcomponents, hotel costs were up 9.9% m/m and 7.6% y/y, reflecting an increase in tourists from abroad.

The value of Hong Kong’s exports grew 14.5% y/y last month, slightly faster than the 14.3% July rate with the special administrative region reversing a decline in exports to the world’s largest economy, according to the Census and Statistics Department. Meanwhile import growth decelerated, dropping from 16.5% in July to 11.5% and the trade deficit fell from $34.1 billion in July to $25.4 billion. At a time of uncertainty regarding globe trade resulting from US tariffs, exports to the world’s largest economy jumped 17.3% y/y after declining 7.6% y/y in June. Shipments to Asia were also strong, gaining 12.6%. In other markets, the Netherlands and UK increased their purchases of Hong Kong items by 65.7% and 55.8%, respectively. Regarding imports, demand from Vietnam, the UK and Taiwan was the strongest, expanding 81.1%, 43.1% and 30.2%, but buying of items from Korea fell 11.5%.

Canada’s year-to-date trend of stable payroll numbers continued in July with the total number of employed individuals climbing only 0.1% m/m, but it was a reversal from a decline by the same amount in June, according to Statistics Canada. Payrolls expanded in only six of 20 sectors. The number of individuals punching timeclocks in finance and insurance was up 1%, followed by 0.6% and 0.2% gains in the health care and social assistance group and the accommodation and foods services category. Conversely, manufacturing and construction employees declined 0.3% and 0.2%. Also in July, vacancies sank 4.2% m/m and 14.5% y/y.

Weekly earnings climbed 0.6% m/m and 3.3% y/y in July with the annualized figure slowing from 3.6% in June while average weekly hours worked, 33.3, was unchanged m/m but down 0.6% y/y.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

ok

A peak followed by a trough caused by the Lemmings front running the tariffs going into effect.