- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 11, 2026 at 12:58 pm

The relentless equity rally is continuing ahead of a series of critical developments on the geopolitical, monetary policy and economic data fronts. The ferocious lift in artificial intelligence enthusiasm doesn’t appear to be ebbing, as investors clamor for shares of tech names and chipmakers that stand to benefit from the increased adoption of the modern technology. Meanwhile, tensions between Tehran and Washington aren’t cooling off, as President Trump called the most recent Iranian proposal unacceptable before the commander in chief meets this week with Chinese leader Xi Jinping to discuss the war, tariffs, trade and other topics. Additionally, Wall Street will need to digest pivotal inflation reports with the CPI and PPI prints on deck. They will be followed by retail sales, unemployment claims and industrial production. The publications are poised to depict the level of pressure that the Middle East conflict has placed on cost forces, the momentum of household shoppers, the strength of labor conditions and the output of the manufacturing sector and may shift positioning across equity and fixed-income portfolios. And just as the end of Chair Powell’s term at the Fed approaches this Friday, yields are jumping across the curve alongside the greenback and WTI crude, as bond watchers carefully gauge whether Kevin Warsh will be able to adopt a looser posture against the backdrop of elevated inflation and an economy that appears to be running hot. In trading, all major averages are advancing with 7 of 11 sectors in the green as the S&P 500 and Nasdaq 100 indices reach fresh records. Elsewhere, commodities are climbing across the complex, prediction markets and volatility protection instruments are catching bids while cryptocurrencies retreat.

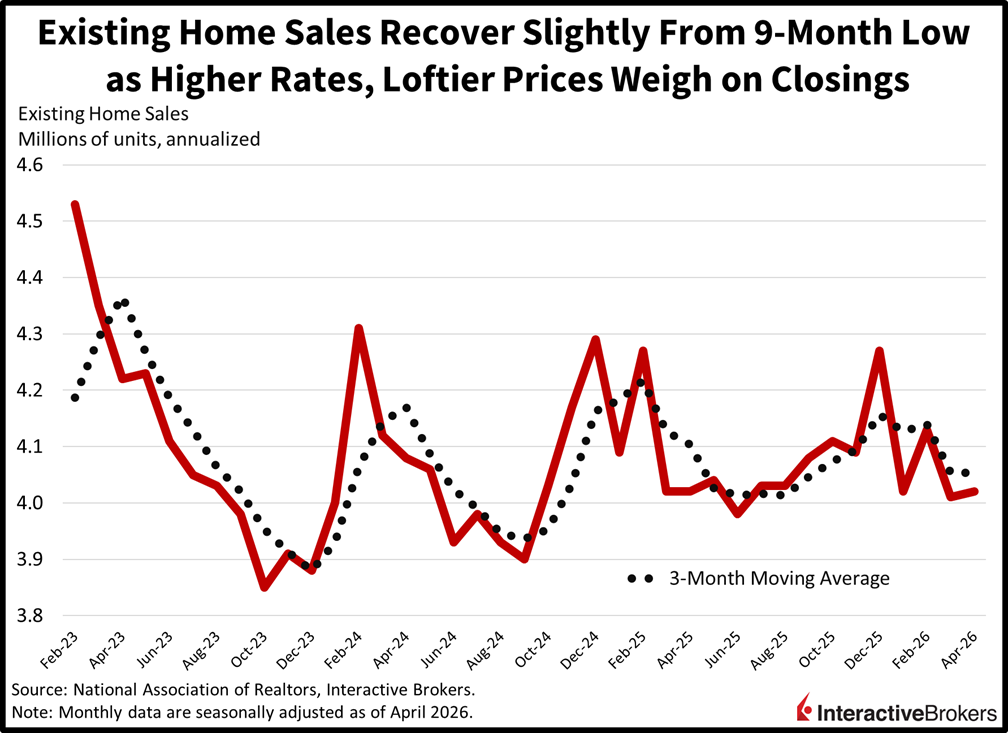

Sales of existing homes barely grew in April, climbing 0.2% month over month (m/m) to a 4.02 million seasonally adjusted annual rate (SAAR). Transactions reversed from March’s 2.9% m/m slip when keys exchanged hands at a nine-month SAAR low of 4.01 million. April closings, additionally, were below the economist consensus estimate for 4.05 million. The volume was unchanged from the year-ago period. Condominium and co-op deals led, climbing 2.7% for both m/m and year-over-year results (y/y). Single-family residences, however, were unchanged when compared to March and were down 0.3% y/y. The median sales price for all housing types ascended by 0.9% y/y to $417,700, the 34th consecutive month of price appreciation. Affordability relative to March also declined because the average mortgage rate ascended from 6.18% to 6.33% but improved from the year-ago period when financing carried a 6.73% burden. Inventory expanded by 5.8% from March and 1.4% from the year-ago period. The market had 4.4 months of supply of unsold inventory, up from 4.2 in March and 4.3 12 months prior.

The ferocious rally in stocks maintains incredible momentum as equity bulls exhibit no sign of tiredness, with buyers present at virtually every dip occurring on Wall Street. But investors face some critical tests that are probably going to rock the boat gently at a minimum or spark volatility in a worst-case scenario. President Trump’s meeting with Xi Jinping comes at a pivotal time for the world’s two largest superpowers, as Beijing has tried to diffuse the Middle East war to limit the pain for the global economy and quell the pressure on Iran’s revenue coffers, an ally that exports a heavy amount of crude to China. The closeness of the two nations is poised to draw the ire of the US commander in chief, and could negatively influence separate negotiations on AI, Russia, Taiwan, trade and tariffs. Another crucial consideration for markets is whether Treasurys have priced in the reality that we are almost certainly going to have Consumer and Producer Price Index (CPI, PPI) readings north of 4% for May and June, ahead of expectations of 3.7% and 4.9% for this week’s April prints. The hot numbers coincide with change at the Federal Reserve and the chance that geopolitical tensions rise, further limiting Kevin Warsh’s capacity to cut while sustaining central bank independence. Still, risk appetites are more likely to wane on the Trump-Xi gathering rather than from loftier rates, as climbing yields all year have done little to deter speculative enthusiasms.

China’s CPI jumped more than expected in April while a gauge of factory gate prices climbed to a 45-month high with loftier gold and energy commodity costs working their way through the economy. The CPI was up 1.2% y/y and 0.3% m/m, considerably stronger than the economist consensus estimates for a 0.9% y/y climb and a 0.1% m/m drop. The gauge also depicted price pressures accelerating from March when the CPI climbed 1% y/y and fell 0.7% m/m. Core inflation, which excludes energy and food, hit 1.2% compared to the year-ago period, an acceleration from March’s 1.1% growth. Within the headline index, retail gasoline prices surged 19.3% y/y, according to China’s National Bureau of Statistics. The country is the world’s largest importer of oil, but its large reserves partially dampened the impact of surging oil prices. Spring breaks and the Chinese equivalent of Labor Day, furthermore, boosted travel spending and demand for gasoline. In other areas, prices for computer memory devices climbed in response to the growth of artificial intelligence computing. Food prices bucked the trend with pork and fresh products stickers causing the category to decline 1.6% y/y.

Gate prices, meanwhile, climbed for the second consecutive month. The PPI hit 2.8% y/y and 1.7% m/m in April, a significant acceleration from the 0.5% y/y and 1% m/m gains in March. The y/y pace was considerably stronger than the economist consensus estimate of a 1.7% northward change. Non-ferrous metals, oil and gas and tech equipment contributed to the PPI acceleration.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!