- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 21, 2025 at 9:12 am

1/ What Was the Fuss About Tariffs Again?

2/ LOW Returning to a High

3/ Sectors Still Show Bullish Performance

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

What Was the Fuss About Tariffs Again?

Tariffs on imported U.S. goods will surely cause a spike of inflation. That was, and to some extent still persists as, the primary narrative used to finger wag the White House. Meanwhile, staffers gave a few media outlets the rejoinder that we are now four-and-a-half months removed from the first tariff announcements, and inflation is a no show.

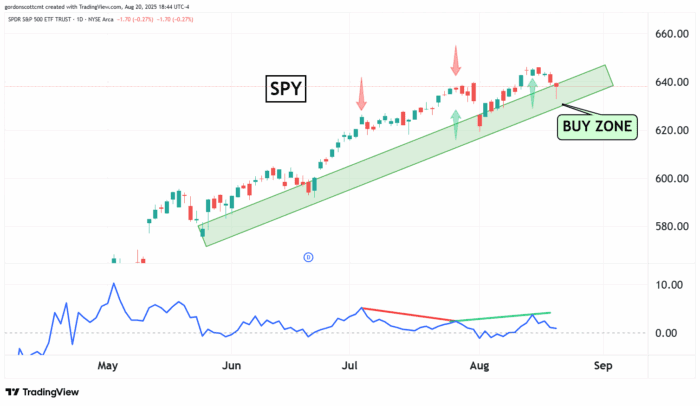

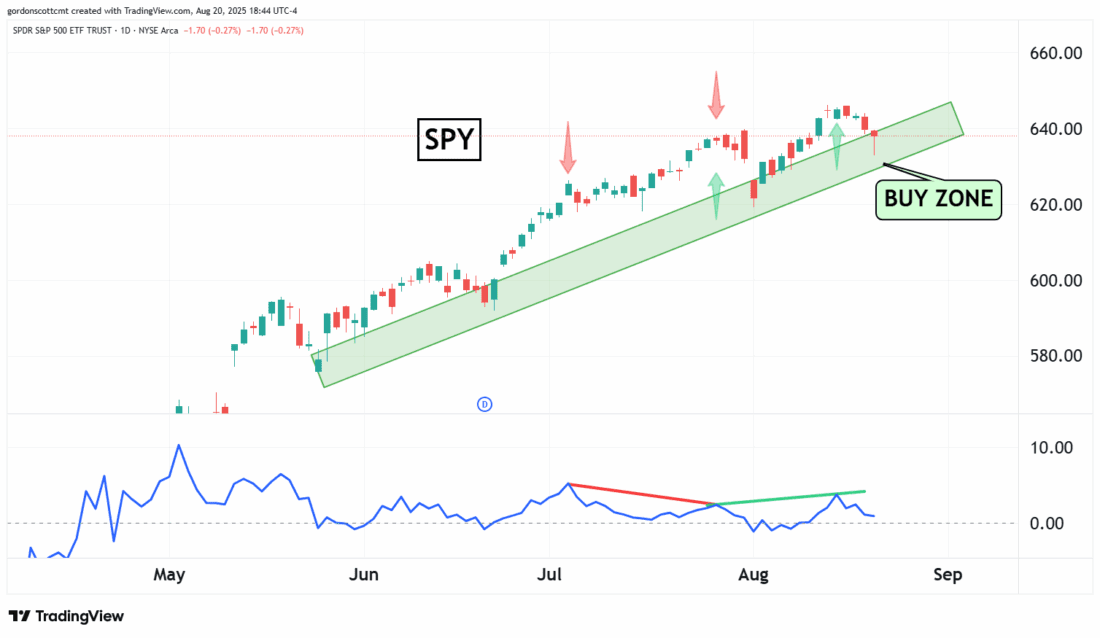

Perhaps that is why even additional tariff news couldn’t keep buyers from showing up once the S&P 500 index (and the ETFs like SPY that track it), dropped into the de facto buy zone (see chart).

The question is whether this is the beginning of a weakening resolve in the minds of buyers. Such a loss of confidence from investors could turn the trend of prices lower, but as of now, technical indicators aren’t showing that. Note that the rate of change (ROC) indicator shown in the lower pane of the previous chart, had a bearish divergence building in July, but now shows a bullish confirmation signal (the last two peaks rising congruent with price action).

If investors need to be worried about rising inflation that will result from tariffs, the pundits need to find another way to tell them to become fretful, because the message is simply not getting through. Alternatively, the message could be wrong.

LOW Returning to a High

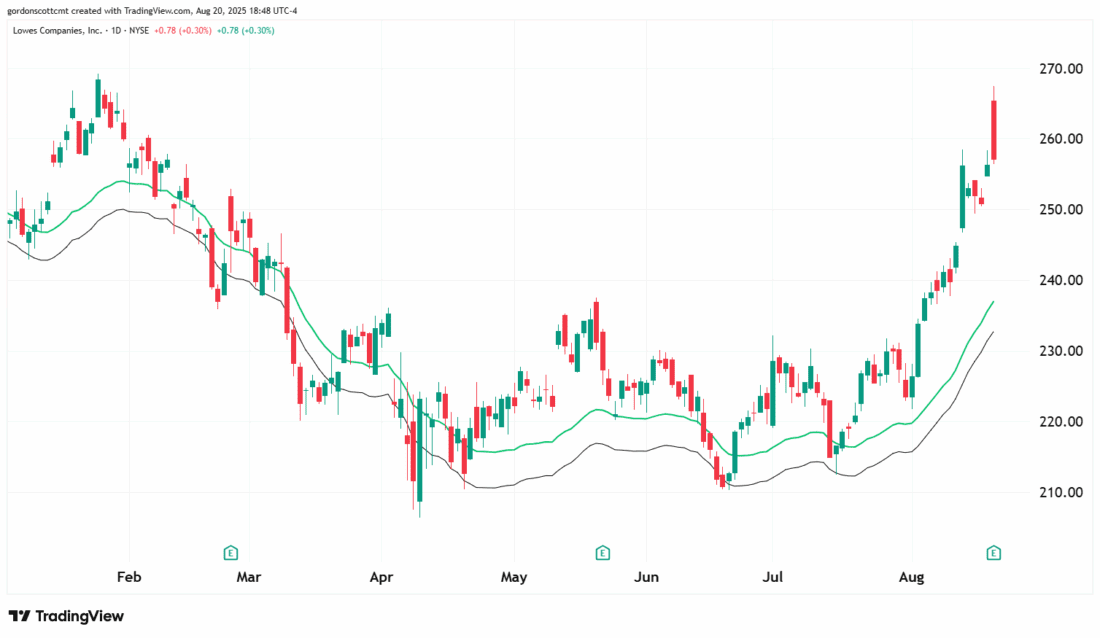

If inflation rises, interest rates won’t be cut by the Fed, and mortgage rates will remain high, keeping potential home buyers away from the market. It follows that home prices will soften under such circumstances. If those circumstances were expected to play out, you can bet that big box home improvement retailers would likely have trouble.

Again, investors are ignoring the popularized narrative and buying up the big box retailers. Yesterday I mentioned Home Depot (HD), but today we see evidence from Lowe’s Companies, Inc. (LOW). This company reported its quarterly earnings Wednesday morning and, even on mildly good news showing that they met forecasts and plan to acquire a supplier, investors bid the stock up to $265 per share, near its all-time high.

This is not the behavior of a nervous, skeptical market waiting to sell off. It may be this year’s version of irrational exuberance. On the other hand, it could also be the wisdom of crowds determining that the economy has better prospects ahead of it than behind.

Sectors Still Show Bullish Performance

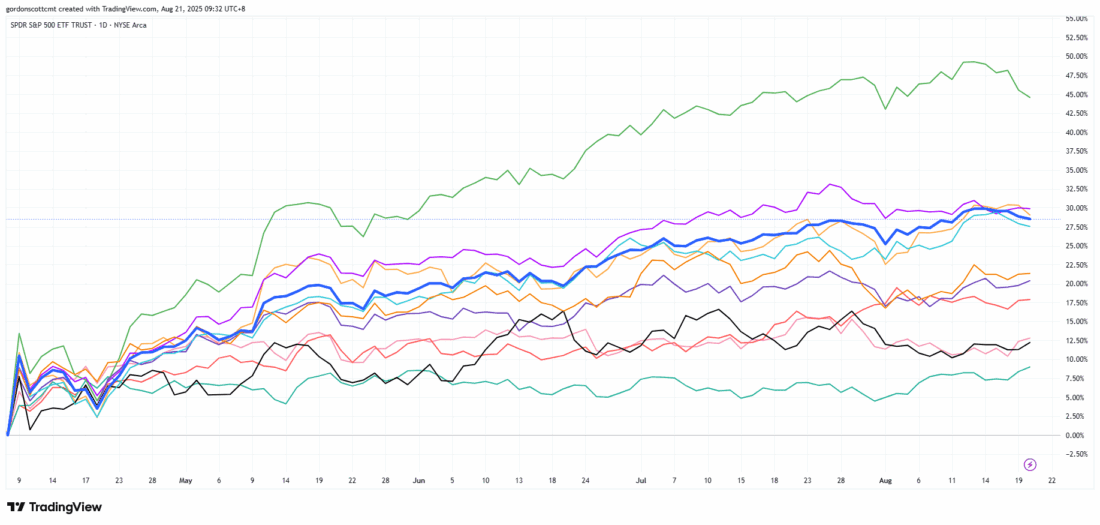

Perhaps it would be too much of a stretch to extrapolate a bullish sentiment just from one stock in the consumer discretionary sector. However, it isn’t just one stock. It is the entire sector. Along with the industrial sector and the technology sector, the consumer discretionary sector has led the broad market higher ever since the tariff tantrums in early April (see chart).

The thick blue line in this chart is the S&P 500, the three colored lines above it represent the aforementioned bullish sectors. The other 8 sectors have lagged the average, but they haven’t run into negative territory over the past few months. While technical analysts could have a debate about the lack of breadth in the current rally, none would feel comfortable ignoring the bullish undertone of the current sector alignment.

—

Originally posted 21st August 2025

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!