- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 1, 2026 at 12:53 pm

Markets zoomed yesterday on a series of reports that implied a potential quick end to the hostilities in the Persian Gulf. Obviously, any cessation of outright warfare would be a good thing – hopefully no one wants to see casualties and major disruptions– but the notion that it might occur without a reopening of the Strait of Hormuz seemed rather incomplete. A ceasefire is a necessary condition for a resolution; reopening the Strait is the only condition sufficient to return global economies to a state of relative normalcy.

Yesterday’s rally was quite stunning, no matter how we look at it. The S&P 500 (SPX) rallied 2.9% and the Nasdaq 100 (NDX) by 3.4%. We haven’t seen one-day moves that large since May 12, 2025, when SPX and NDX jumped by 3.3% and 4.0%, respectively. That was about one month after the giant post-“Liberation Day” rallies of April 9th, when those indices zoomed by 9.5% and 12%. The combination of yesterday’s monster rally and today’s comparatively minor, but still substantial, 1% advance has brought us back to levels not seen since (… double-checks notes…) one week ago.

Source: Interactive Brokers

How about that for some “socially acceptable volatility”?

It is difficult to know exactly what led to stock traders’ extraordinary enthusiasm. I suspect it was a combination of factors, with the end of the first quarter playing a significant role.

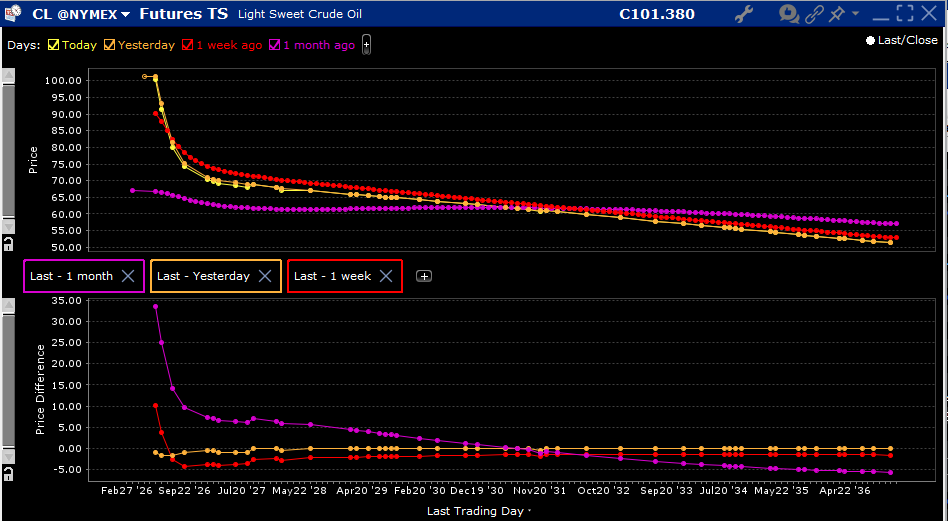

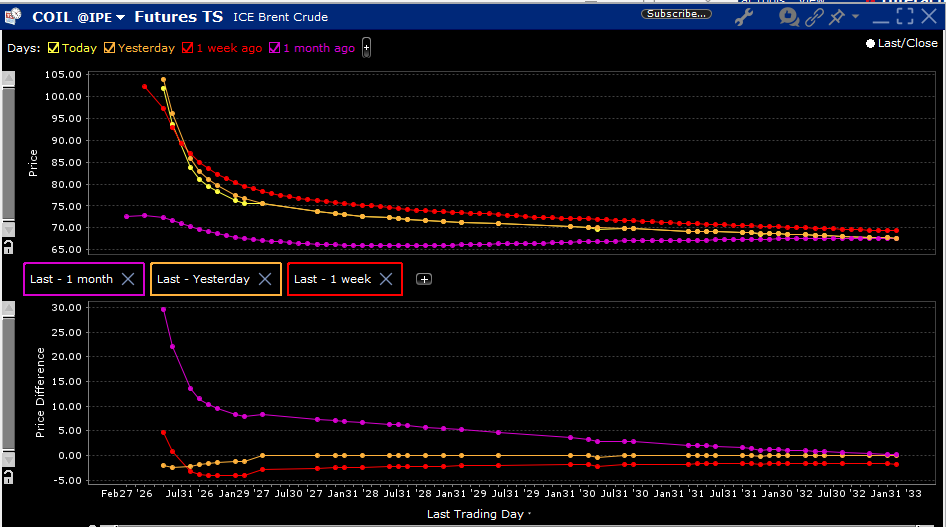

For starters, crude futures fell, but not to a degree that might have suggested that oil traders viewed an imminent end to the bottlenecks affecting that commodity. But it was also the expiration day for May futures on Brent (COIL) and WTI (CL). Big moves can occur on expiration in already volatile commodities, particularly when there are supply or demand constraints. May Brent futures rose by $4.94 to a life-of-contract high of $118.27 yesterday, while the June contract fell by $3.18. Both months’ WTI contracts fell yesterday, with May -$1.46 and June -$2.98. This morning, both June contracts are down about $2. There is clearly some incremental normality being priced in, particularly in longer-term contracts since last week, but little that signals an imminent return to pre-conflict pricing.

Source: Interactive Brokers

Source: Interactive Brokers

The quarter-end seems to have motivated at least some of the buying yesterday in equities. The selling throughout the course of the past month, which accelerated late last week, must have left at least some institutions with higher cash allocations than normal and some traders with uncomfortable short positions. On Thursday, we noted that skews in SPX options had notably changed, with boosted implied volatilities in upside strikes. Some of that was undoubtedly driven by speculators hoping for a quick bounce like we saw last year, but I believe the bulk of that activity resulted from under-invested institutions insuring against underperformance and rally-selling traders hedging against a major reversal. Although traders are not necessarily focused on the calendar, portfolio managers who file quarterly reports are. They probably had second thoughts about appearing poised to miss a potential turnaround by carrying too much cash for their investors’ liking.

Today we see the rally continuing. Some of that may be attributable to the first of the month; some might reflect a change in short-term momentum; some are certainly hoping that the President’s speech tonight could bring a meaningful change to the events in the region. By tomorrow, we’ll get a clearer sense of how to attribute those factors.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Short selling is an advanced trading strategy involving potentially unlimited risks and must be done in a margin account.

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

It’s Tuesday, anybody seen the new TACO trick? er, I mean, truck? It’s time once again and maybe it will work one more time. Besides, I’m hungry for some more gains even if they are based on BS-based gains/profits that should be taken and won’t last. Should I sell the rallies… yet?