- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 27, 2026 at 12:57 pm

(Today’s theme song by Berlin)

Things change quickly in today’s markets. When I wrote yesterday’s piece, completed before 11 AM EDT, stocks had tried to gamely bounce off their lows. I later emerged from several hours of meetings to discover that bounce had failed miserably. After the close, the President announced a 10-day extension of the ceasefire, which seemed intended to bolster nervous markets. Post-market futures bounced, but as of this morning, traders are not mollified. Rhetoric isn’t doing the job.

Last Friday we asked whether there was indeed a “Trump Put”, and if so, what was its strike. On Monday, after an early Truth Social post announcing a 5-day pause in bombing Iran’s infrastructure, we felt confident in asserting that the strike on that hypothetical put was revealed to be either 6,500 on the S&P 500 or 4.45% on the 10-year Treasury yield. (Frankly, that should have been 4.40%, but we’re in the right ballpark.) After discussing that topic in a media interview on Tuesday, a well-respected market veteran suggested that a 4% 2-year yield might be more appropriate, which was indeed a highly plausible suggestion. That’s the problem with nebulous “options” – the strike is far from explicit.

As the week wore on, the early ceasefire enthusiasm faded, and after yesterday afternoon’s sloppy close we found ourselves with SPX below 6500, the 10-year above 4.40%, and the 2-year just below 4%. Although the timing of the ceasefire extension might have been coincidental, I doubt it. I believe that once again, it was an attempt to exercise that mythical “Trump Put.” But this time it had no lasting benefit. Why not?

We noted yesterday that there was a noteworthy upside skew to SPX options, implying that traders were hedging against the risk of a significant rally, writing:

Few investors, no matter how concerned they may be about the prospects of higher oil prices bleeding into broader price pressures and economic malaise, want to risk being caught wrong-footed in the event of a ceasefire or similar resolution.

The post-Liberation Day reversal is still quite fresh in investors’ minds, so even though we remain mired in a notable medium-term downtrend, traders who are willing to trade the market from the short side do not want to bear all the risk of a similar updraft. There is a “right-tail” risk, so to speak, and options pricing continues to reflect it. (That said, those same options are also pricing in no shortage of “left-tail” risk.)

Skews for SPX Options Expiring April 2nd (top), April 17th (middle), May 15th (bottom)

Source: Interactive Brokers

The immediate problem for traders is that the rally attempts that occurred earlier this week failed at their attempts to breach the 200-day moving average. This is problematic for several reasons: the 200-day never offered meaningful support on the way down, yet offered resistance on the way up; the 200-day is the lone trendline that is not pointing lower; there are few obvious levels of significant support for several hundred points; and as we are about to complete our fifth straight weekly decline (barring a stunning late reversal), the pattern of lower highs and lower lows is now well established. I know that not everyone is a fan of charting, but it is quite apparent that SPX has rolled over after a long, solid upward move.

SPX 10-Months, Daily Candles, with 50-day (top), 100-day (middle), and 200-day (bottom) Moving Averages and Horizontal Line at 6520

Source: Interactive Brokers

Hence, having failed to achieve anything more than a brief respite from the nascent downtrend, mere jawboning isn’t doing the trick today. Now-wary investors want and need something more concrete. A temporary pause, while better than outright hostilities, is just that – temporary. The message currently being sent by the markets is that a series of short-term respites that seem timed to assuage their fears are no longer sufficient.

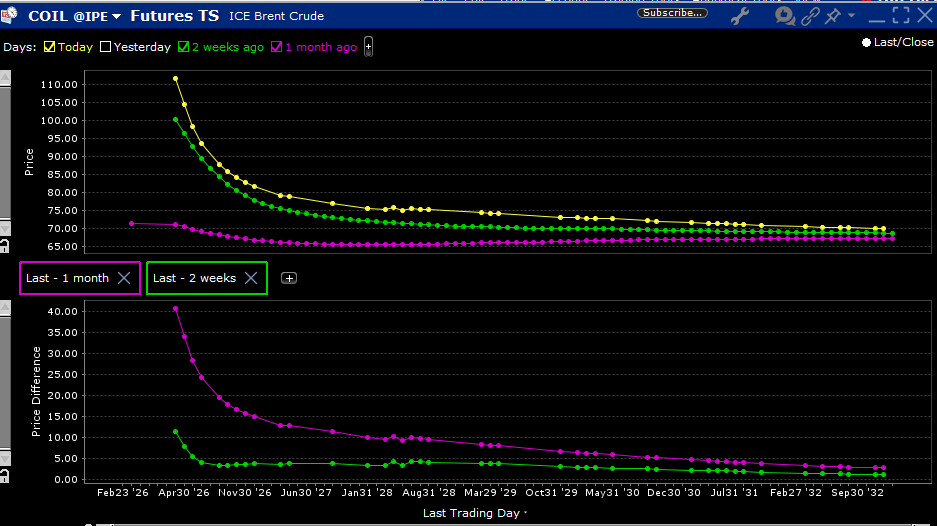

This is especially so when we consider that the longer it takes until the situation is resolved, the more lasting the effects. For starters, it takes weeks for oil tankers to reach Asian and European destinations from the Persian Gulf, so the more time that elapses, the longer it will take the bottleneck to resolve. Futures markets are saying this explicitly, with Brent futures expiring one year from now reflecting about $15 higher prices than prevailed prior to hostilities. Throw in the fact that farmers have to bear the costs of higher fertilizer prices whenever the calendar says they need to plant, along with the potential impact of constrained helium availability on already tight semiconductor supplies, and we find ourselves staring at a series of consequences that are difficult to resolve in the near-term – and certainly not fixable via executive order (like tariffs) or soothing rhetoric.

Brent Futures Term Structures, Today (yellow), 2-Weeks Ago (green), 1-Month Ago (magenta)

Source: Interactive Brokers

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

rhetoric used to represent intention and therefore was solid information which traders could use to form judgements and markets were free. Rhetoric is now manipulated information therefore is not solid information so traders cannot rely on it.

Most people look upon bankruptcy as a personal failing, rather than a smart way of getting out of paying your debts. Those of the latter treat their problems with the approach of “What do I have to do today to get this off the table?” Working as a construction superintendent, I learned that mistakes will often happen and the first response to it is one of “How can I cover this up?” That normally only compounds the sin. The good mechanic will take the time to find a solution that it will require another good mechanic to see that there ever was once a problem there. Clearly yesterday there was a possibility of choosing a solution for resolving TSA, etc. Yes, it wouldn’t open up traffic through the Strait, but it would show people that government could solve a problem and that might help improve the spirit of the public, and possibly results in the fall, but the resident at 1600 said “No” , and the pain will continue. The investing public has to decide whether they can personally stand the continuing pain until this resolves, or whether they wish to cut their loss at this point. I’ve been around long enough to go for the former, but I admit I can’t see a good mechanic in sight.