- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 2, 2026 at 11:45 am

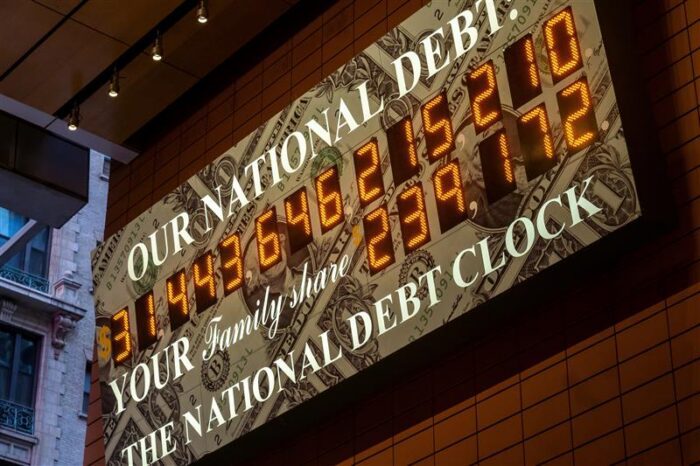

The federal debt has crashed through a gut‑punching milestone: $39 trillion. To put that in perspective, that’s enough to buy every person in the US a yacht and still have billions left over. Treasury keeps hitting this number, bouncing off it, and hitting it again, like a ceiling we can’t quite break through, except we keep breaking through it anyway.

Here’s the thing, the big number isn’t actually the scary part. The scary part is why we got here and what it means for your wallet, your taxes, and your future.

Imagine you make $100 a month but spend $115. Every month, you’re short $15. So you put it on a credit card. After a year, you owe $180 on that card. That’s your debt. But here’s where it gets bad, your credit card charges 8% interest, so now you owe even more just to cover the interest bill. Eventually, you’re paying more in interest than you’re spending on actual stuff you need.

That’s basically where the US government is right now… except with trillions of dollars and way more serious consequences.

Before we get into the numbers, we need to separate these words that get thrown around like synonyms, but they’re not. Think of them like this:

The problem? Deficits keep happening, so debt keeps growing. And the bigger the debt, the more you pay in interest. It’s a vicious loop.

In 2025, the US government spent $7.01 trillion. Here’s the breakdown, and it’s kind of wild:

| What | Cost | Your Share of Budget |

| Social Security (retirement checks) | $1.58T | 22.5% |

| Medicare (senior health care) | $0.987T | 14.2% |

| Medicaid + health stuff | $0.98T | 14.0% |

| Interest on debt | $0.97T | 13.8% |

| Defense | $0.917T | 13.1% |

| Unemployment, welfare, other support | $0.70T | 10.0% |

These six things alone eat up over 80% of every dollar the government spends.

Now look at that interest line. It’s the fourth biggest budget item,right in front of defense. And here’s the kicker: it’s money that literally buys nothing. No roads, no research, no bridges. It’s purely paying off credit card debt. Imagine if your car payment was bigger than your groceries, that’s kind of where we’re heading.

Interest used to be boring. Like, a line item nobody cared about. Not anymore.

In the last few years, interest costs have exploded. Why? Two reasons:

The government is already spending more on interest than on the entire military. If that seems insane, you’re not alone.

Here’s the brutal truth, interest must be paid before anything else. It’s not optional. It’s like if your credit card company showed up at your door and demanded their money before you could buy groceries.

This means:

Every dollar spent on interest is a dollar not spent on things that could help your life. And as interest costs grow, this gets worse.

We’re already five months into fiscal year 2026, and the US has racked up a $1 trillion deficit. At this pace, we’re heading for a $2.4 trillion deficit by the end of the year. That means the government is borrowing massively, adding to the debt pile, which means paying even more in interest next year.

It’s like trying to dig yourself out of a hole by digging faster.

There are really only four ways to solve this:

Option 1: Cut spending – Mostly Social Security and Medicare, since they’re the budget’s biggest items. But good luck telling 60 million seniors their checks are smaller. Politicians know this is unpopular.

Option 2: Raise taxes – Make people and businesses pay more. Also unpopular, especially heading into an election.

Option 3: Lower interest rates – Have the Federal Reserve cut rates so the government pays less on its debt. But that requires the economy to cool down first, and the Fed doesn’t take direct orders from Congress.

Option 4: Privatize government sectors – Sell off or hand over operations of government services (highways, airports, water systems, prisons) to private companies. This generates one-time cash upfront and shifts operational costs to the private sector.

The honest answer? We’ll probably need some mix of all four. But right now, nobody’s seriously pushing for any of them. It’s the political equivalent of ignoring a leak in your roof and hoping it goes away.

The uncomfortable truth is that federal debt isn’t some abstract policy thing. It touches your life in real ways:

Policymakers know this math doesn’t work forever. The question isn’t if things have to change, they do. The question is when:

Historically, when governments face these decisions, they choose “later” until “later” becomes a full-blown crisis. Let’s hope we’re different.

To learn more about how Fiscal Policy impacts you download the IBKR InvestMentor App.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

for Daily Seasonal Data")

Starting with the headline, 39 trillion and 8 billion people. My immediate reaction was “something is wrong there”. The answer is $4,875, hardly enough to buy a simple fiberglass duck blind boat. If it were just the good old US of A, it would work out roughly to about $103,000. Nice sailboat, but not even a Hinckley. But then again, not many people really know what a billion dollars is let alone a trillion. Nobody in Washington, maybe a couple, really knows. The worst part is they don’t care. Everett Dirkson used to quip, ” billion here, a billion there, and it adds up to real money. I don’t know either – the best understanding that I could come up with for myself, I tried, when writing about what it would cost to get rid of fossil fuels. To wit: “• A TRILLION is a really big number -One never heard it mentioned 20 years ago, but now it is bandied about like it’s pocket change, particularly in the context of debt and global warming e.g. the spending bill Biden just signed was $1.7 trillion –this amount now clearly falls into the category of “pocket change.” • $150,000,000,000,000.00 trillion (150T)- it’s 12 zeros x 150 and is less than a quadrillion, otherwise to me it means zip, zero • $150 T = 150,000 (thousand) x $1,000,000,000.00 (billion)– breaking it down into smaller parts doesn’t help either, still not ringing any concept bells on this end. When my calculator can’t deal with a number, why should I have an understanding? • $150 T = 2.3 x the GDP’s of the World’s 25 largest economies and 12.5x the rest of the world– a slight glimmer of understanding, but I still can’t quite grasp our own GDP • $150 T = 9 x the value of all the gold in the World (produced + reserves to date) —–I know it fits in a 23meter cube and is $1,844/oz. But that’s it. • $150T would pay for a $450,000 house for every man, woman, and child in the US –getting somewhere now, I can conceptualize that house, but still have a hard time conceptualizing 380,000,000 of them. • $150T would provide a payment of $18,750 to every man, woman, and child on the planet. – I have a firm grasp on this one- it’s a little more than the value of my 1981 Intl 20-ton dump truck and a 2005 John Deere Trac loader, combined. But now you have to conceptualize 8,000,000,000 + or – having these two pieces of equipment. Do you think the author of the headline understands what is being written about. Maybe, maybe not. Ciao glen shipway an IB client

The correct taxes can lower taxes on businesses, lower costs of living, lower costs of doing business, and reduce inflation all at once. But the financial industry will never allow that. Also, government debt is a small part of what drives inflation. Corporate borrowing, juiced by the LLC that results in zero consequences for irresponsible long-term borrowing, is a massive driver of inflation.

OMG, who taught you simple math, author?

No, there are 2 options for fixing it you missed: 1) Cut riduclous unnecessary spending (like DOGE found and GAO finds every year) 2) Cut beaurocracy to stimulate growth

I don’t think it is fair to lump social security and Medicare in with all the other expenses. They are funded through a dedicated trust that is replenished by payroll not income tax. Right now there is more going out of the trust than coming in but the difference is that the trust has a positive balance that is making money through treasury bills. Eventually the trust is projected to have a negative balance and then can be in the same category of expenses paid by income and other taxes.

It is fair because those expenditures are massive and no longer covered by the income they bring in. 7 years from insolvency. Democrats have been encouraging massive fraud in every state – from those programs, and complaining bitterly when DOGE or anybody else points it out.