- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 1, 2026 at 2:04 pm

US stocks are rallying further on the heels of the best single day for equities in almost a year. Talks of a ceasefire between Tehran and Washington are propelling optimism that the Middle East conflict will resolve soon, while President Trump stating that the war could end within two to three weeks additionally bolstered peace hopes. A trio of beats on the economic calendar also helped propel speculative enthusiasms, as ADP-jobs, retail sales and ISM-manufacturing signaled a cycle that remains on solid footing despite recent headwinds that are clouding the outlook. The robust data are holding Treasuries back from gains, as buoyant consumption, hiring and factory activity along with WTI still around $100 a barrel support both growth projections and inflation expectations. Crude continues to be more attentive to hostilities on the ground amidst continued violence in the region, unlike other asset classes that are increasingly driven by headline comments from political and military leaders. Indeed, all major averages are up north of 1% with every sector and subcomponent gaining except for staples and energy. Cryptocurrencies and forecast contracts are catching bids as well, but Treasurys are nearly flat, and the greenback is sinking on revitalized rate cut prospects. The commodity complex is mostly lower across the board although gold and silver are advancing; volatility protection instruments are seeing declining interest in light of risk-on attitudes on Wall Street.

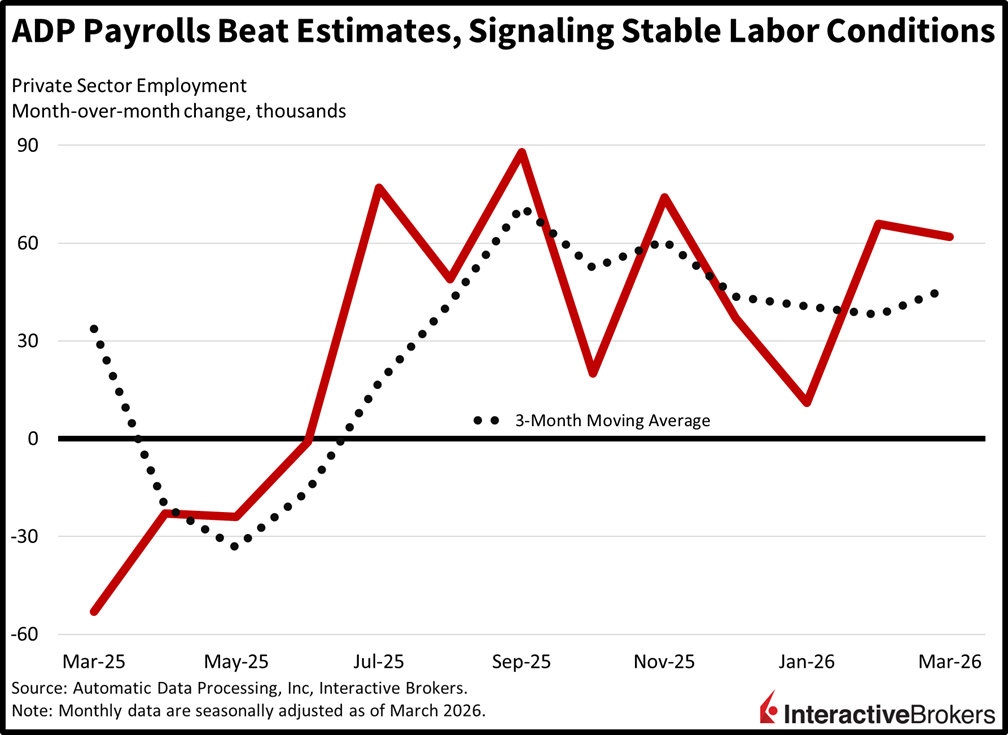

Small businesses drove strong hiring last month, but mid- and large-sized firms trimmed labor, according to ADP. The US private sector added 64k positions, above the median estimate of 40k and near February’s 66k figure. Roster expansions occurred across most sectors, with the extent of their gains as follows:

Leisure/hospitality, other services, financial activities, and professional/business services printed more tempered progress with each adding less than 8k employees. Conversely, trade/transportation/utilities and manufacturing lost 58k and 11k workers, respectively.

Establishments with under 50 employees boosted employment by 85k, while those with 50-499 and north of 500 experienced headcount reductions of 20k and 4k. Wage pressures intensified, meanwhile, with the year-over-year (y/y) change in annual pay accelerating from 6.3% to 6.6% for job changers while remaining at 4.5% for stayers.

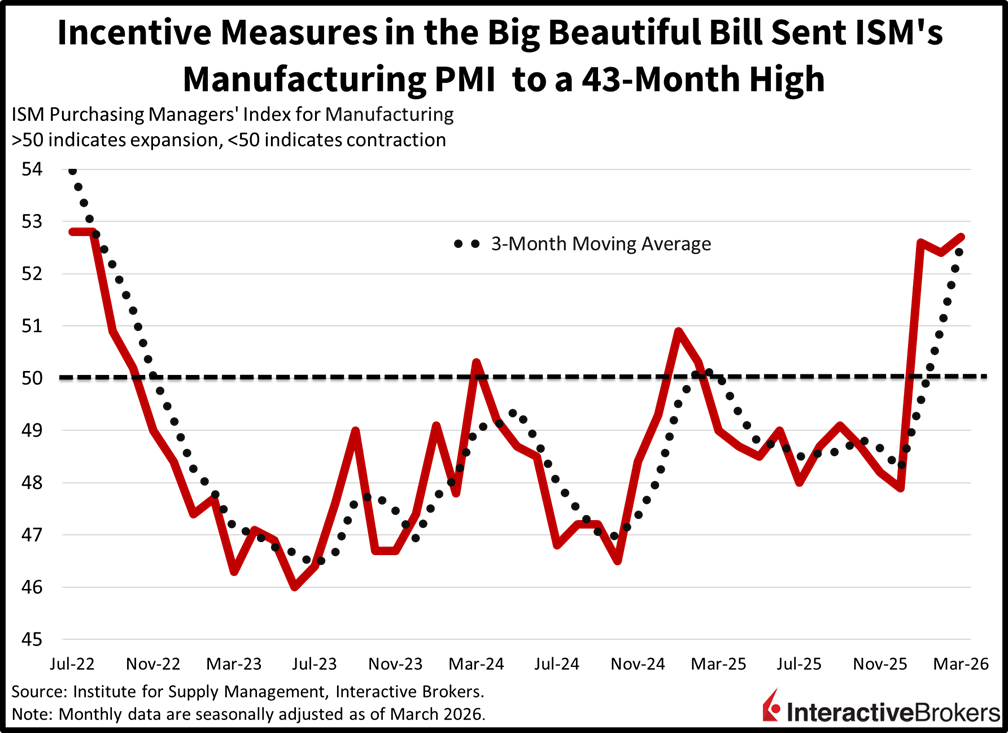

The manufacturing sector grew at its fastest pace in 43 months last month as strong customer demand and incentive measures from 2025’s Big Beautiful Bill generated an uptick in factory activity. The Institute for Supply Management’s Purchasing Managers’ Index leaped to 52.7, the loftiest level since August 2022. The March result arrived modestly ahead of the anticipated 52.5 and February’s 52.4. Production, backlogs and new orders helped deliver the headline beat, coming in at 55.1, 54.4 and 53.5. Prices soared to 78.3 though, as tariff pressures and heavier energy costs were felt by manufacturers and their consumers alike. Goods producers did yield more output with less workers, however, as the employment gauge fell to 48.7. Exports came in at 49.9, meanwhile, pointing to a slight contraction below the critical threshold of 50.

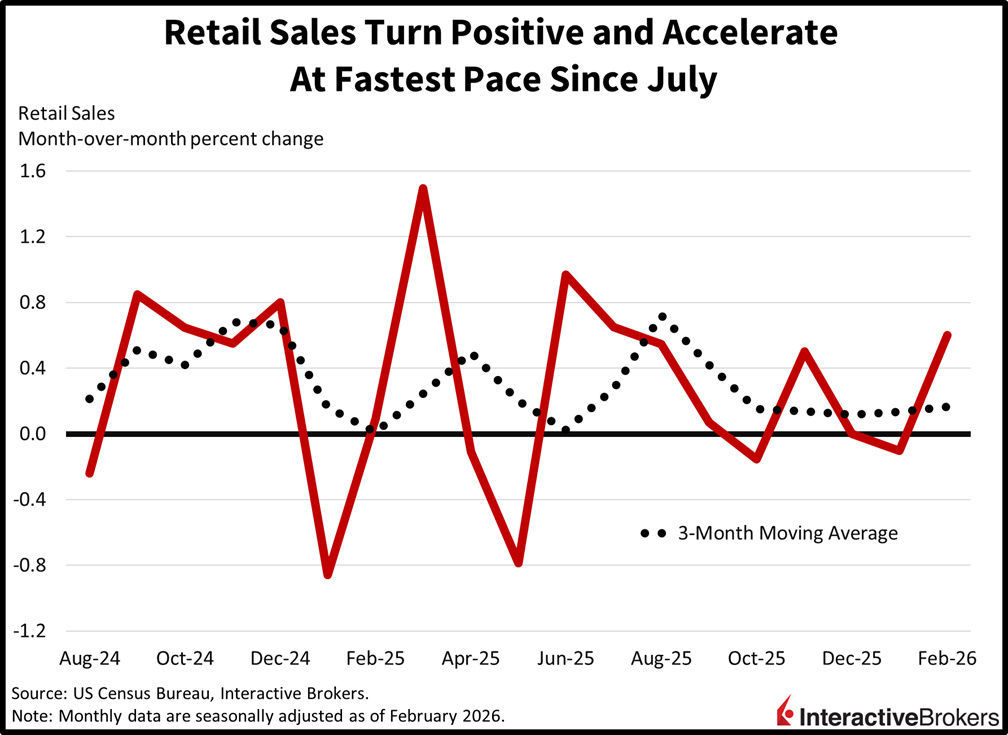

Retail sales expanded for the first time in three months in February and accelerated at the fastest pace since July as consumers rebounded from a sluggish holiday season. The February headline grew 0.6% month over month (m/m), exceeding the 0.5% expected and the -0.1% from January. Performance was broad-based, too, with 10 of the thirteen categories growing, propelling the control group, an integral input into the Gross Domestic Product calculation, up to 0.5% m/m, north of the 0.3% projected and 0.2% from the prior period. This print was delayed due to government shutdown.

President Trump is scheduled to address the nation tonight and investors and traders alike will be listening closely for any clues on when the Iran war will end. Stocks are exuberant against the backdrop, but crude oil is still wary, trading near $100, as violence in the Middle East remains elevated. It’s precisely the bifurcation between equities and commodities that signals a heavy amount of confusion in markets, with the former camp taking its cue from statements out of Washington and Tehran, while the latter sees ongoing aggression in the region as an indication that peace hopes are remote. This evening’s communication may shed light onto which asset class has a better grip on the geopolitical tensions, while the event also carries the potential of further perplexing market participants.

Large Japanese manufacturers’ outlook fell slightly during the first quarter, but overall sentiment strengthened across the business community, according to the Tankan indices. The Large Manufacturers Index climbed one point from 16, matching the economist consensus estimate. The advancement occurred despite the Big Manufacturing Outlook Index slipping one point to 14, which was better than the economist consensus estimate of 13. Among smaller goods producers, sentiment also improved with the corresponding Tankan Index moving from 6 to 7. Meanwhile, indices for large and small non-goods producing companies climbed from 34 and 15, respectively, to 36 and 16.

Demand for artificial intelligence products pushed South Korea’s semiconductor exports to an all-time high last month and helped the country’s trade surplus jump from $15.3 billion in February to $25.7 billion. Total exports climbed 48.3% y/y, outpacing the economist consensus estimate for a 44.9% ascent and February’s 28.7% growth, according to preliminary data from South Korea’s customs service. Shipments of semiconductors drove the gains with a 151% jump. Also in March, imports were 13.2% higher than during the year-ago period, falling short of the 18% growth estimate but accelerating from the 7.5% expansion in February.

Regarding countries, the value of South Korea’s shipments to China and the US the exceeded the year-ago amounts by 64.2% and 47.1%, respectively.

South Korea officials yesterday proposed a $17 billion stimulus package to help buffer the country’s economy from the adverse impacts of the Iran war. The country imports the lion’s share of the energy it consumes, and the stimulus would assist residents with higher bills for energy and oil derived products. It would also include reimbursements for public transportation, providing consumer vouchers and placing a petroleum price cap. The package would be funded by an additional tax on semiconductor exports.

Hong Kong shoppers splurged in February with retail sales spiking 19.3% y/y following January’s 5.5% growth, according to the Census and Statistics Department.

During the first two months of 2026, furthermore, sales were up 11.8% y/y. The Census and Statistics Department provided the two-month data because the Chinese New Year fell on Feb. 17 this year but on Jan. 29 last year.

Categories with higher y/y sales and the extent of the changes for the two-month period were as follows:

Conversely, fuel sales and Chinese drugs and herbs slipped 14.2% and 0.8%, respectively.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

U.S. Spot Gold trading through IB LLC accounts is only available to legal residents of the United States that do not reside in Arizona, Montana, New Hampshire, and Rhode Island.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!