- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 14, 2021 at 11:00 am

GitLab Inc. (GTLB), a software development platform, is set to IPO soon. At the midpoint, the firm would have a valuation of $8.2 billion and earn our Unattractive rating.

GitLab is a subscription based SAAS company with a large total addressable market (TAM), which may entice investors. However, the firm sells to only a tiny portion of its TAM and is competing against some of the largest technology companies in the world. With worst-in-class fundamentals and an already overpriced valuation, we have significant concerns regarding the stock’s profitability.

We believe the stock is worth less, approximately 91% below the midpoint of the expected price range. An $8 billion valuation implies that GitLab will achieve very optimistic milestones, including reversing a downward trend in profits, growing revenue by more than 17x, and nearly tripling its current market share.

With only ~21 months of cash to cover its current cash burn rate, GitLab’s current owners need this IPO to help the company avoid bankruptcy.

GitLab’s model for growing revenue is based on the freemium model: gain users with a free version of its software and convert those users to paying members. As of June 2021, GitLab had 30 million free users with just 15,356 paying users.

In other words, GitLab has converted less than 1% of its user base, which is well below the average estimated freemium conversion rate of 2-5%. Most of these converted users are also on lower priced, less profitable plans. GitLab notes that it has 3,632 “base customers”, which generate more than $5,000 in annual recurring revenue (ARR). It discloses only 383 customers generating $100,000+ in ARR.

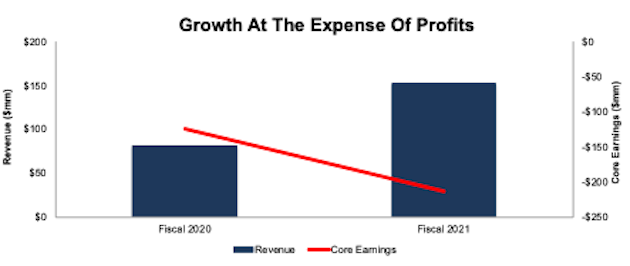

This model has proven capable of driving revenue growth, as GitLab’s revenue grew 87% year-over-year (YoY) in fiscal 2021. However, Core Earnings[1] fell from -$125 million to -$213 million over the same time.

Sources: New Constructs, LLC and company filings

GitLab’s strategy is clearly focused on growing its top line and forgoing profitability for now. While GitLab’s net operating profit after-tax (NOPAT) margin improved slightly from -158% in fiscal 2020 to -141% in fiscal 2021, it remains highly negative. Additionally, the firm’s return on invested capital (ROIC) declined from -41% to -76% over the same time. GitLab’s economic earnings, the true measure of cash flows, declined from -$149 million in fiscal 2020 to -$229 million in fiscal 2021. Despite growing its top line, GitLab is destroying shareholder value.

GitLab operates in the highly competitive infrastructure software market, which the firm notes in its S-1 is estimated to be worth $328 billion in 2021 and grow to $458 billion in 2024, or 12% compounded annually. Such a large TAM may entice investors looking for another tech growth story.

However, Gitlab recognizes that it cannot provide products to the entire TAM and, instead, aims to serve $43 billion of the industry in 2021 and $55 billion in 2024. At its current run rate revenue[2] of $233 million, Gitlab has just 0.5% share of its “serviceable” market in 2021.

If we narrow in on the Global DevOps segment of the infrastructure software market, the expected CAGR is higher, but the addressable market is much smaller. Global Industry Analysts projects the Global DevOps market will grow by 20% compounded annually through 2026 to reach $18 billion. Regardless of the addressable market, Gitlab’s IPO valuation implies it will take significant share and grow much faster than either of these market projections, as we’ll show below.

Click here to read the full article – GitLab: Another Overpriced Tech Company

—

This article originally published on October 8, 2021.

Disclosure: David Trainer, Kyle Guske II, Alex Sword, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Only Core Earnings enable investors to overcome the flaws in legacy fundamental research, as proven by The Journal of Financial Economics.

[2] Gitlab calculates run rate revenue as revenue for the three months ended July 31, 2021 multiplied by 4.

Click here to download a PDF of this report.

David Trainer, Kyle Guske II, Sam McBride, Matt Shuler, Alex Sword, and Andrew Gallagher receive no compensation to write about any specific stock, style, or theme.

The information and opinions presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or solicitation of an offer to buy or sell securities or other financial instruments. New Constructs has not taken any steps to ensure that the securities referred to in this report are suitable for any particular investor and nothing in this report constitutes investment, legal, accounting or tax advice. This report includes general information that does not take into account your individual circumstance, financial situation or needs, nor does it represent a personal recommendation to you. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about any such investments or investment services.

Information and opinions presented in this report have been obtained or derived from sources believed by New Constructs to be reliable, but New Constructs makes no representation as to their accuracy, authority, usefulness, reliability, timeliness or completeness. New Constructs accepts no liability for loss arising from the use of the information presented in this report, and New Constructs makes no warranty as to results that may be obtained from the information presented in this report. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information and opinions contained in this report reflect a judgment at its original date of publication by New Constructs and are subject to change without notice. New Constructs may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them and New Constructs is under no obligation to insure that such other reports are brought to the attention of any recipient of this report.

New Constructs’ reports are intended for distribution to its professional and institutional investor customers. Recipients who are not professionals or institutional investor customers of New Constructs should seek the advice of their independent financial advisor prior to making any investment decision or for any necessary explanation of its contents.

In-depth risk/reward analysis underpins our stock rating. Our stock rating methodology grades every stock according to what we believe are the 5 most important criteria for assessing the quality of a stock. Each grade reflects the balance of potential risk and reward of buying that stock. Our analysis results in the 5 ratings described below. Very Attractive and Attractive correspond to a “Buy” rating, Very Unattractive and Unattractive correspond to a “Sell” rating, while Neutral corresponds to a “Hold” rating.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from New Constructs and is being posted with its permission. The views expressed in this material are solely those of the author and/or New Constructs and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!