- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 16, 2024 at 11:00 am

More bad news for doves last week who are hoping for interest rate cuts sooner rather than later. The Consumer Price Index (CPI) for December came in above expectations, showing sticky inflation is still in play and adding to the reasons that the US Federal Reserve (along with robust jobs numbers) may hold off on interest rate cuts in Q1.[1] Expectations for a Jan 31 rate reduction are dwindling, with the CME Group’s FedWatch tool now showing only a 4.7% chance that there will be a rate cut.[2]

Higher interest rates (as well as potentially lower interest rates later this year) were one headwind highlighted in many of the Q4 bank reports out last week. Despite missing earnings expectations due to a $2.9B fee from regional bank rescues, JPMorgan Chase (JPM) was still able to show revenue growth of 12% during the quarter, leading investors to take the stock higher after the report. However, Jamie Dimon continued to strike a somewhat cautious tone on the US economy. On the one hand he remarked that “The U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing,” but government deficit spending and restructuring of the global supply chain “may lead inflation to be stickier and rates to be higher than markets expect.”[3]

Sentiment from other reporting banks, Citigroup (C) and Bank of America (BAC), hit a similar tone, and results were also impacted by large fees tied to last year’s regional banking crisis. Citigroup saw earnings-per-share (EPS) fall 24% year-over-year (YoY) due to several large charges, and revenues declined 3% over the same period. Due to poor results and an embattled stock price, CEO Jane Fraser announced a 10% workforce reduction.[4]

Bank of America reported revenue of $22.1B that missed expectations of $23.74B. The Charlotte, North Carolina based bank was also hit with a $2.1B fee tied to regional bank failures. Q4 EPS and revenues saw YoY declines of 18% and 10%, respectively.[5]

While banks benefit from the bigger interest fees that higher rates bring, it’s been at the expense of other areas such as loans and investment banking. Wells Fargo (WFC) noted this double-edged sword in their Q4 results. While lower interest rates could mean net interest income falls by 7-9% YoY in 2024, higher interest rates have been problematic for deposits as consumers look for higher yielding instruments. “As we look forward, our business performance remains sensitive to interest rates and the health of the U.S. economy, but we are confident that the actions we are taking will drive stronger returns over the cycle,” said CEO Charlie Scharf.[6]

According to FactSet, with this early round of disappointing results, blended S&P 500Ⓡ EPS growth has turned negative, now expected to come in at -0.1%.[7]

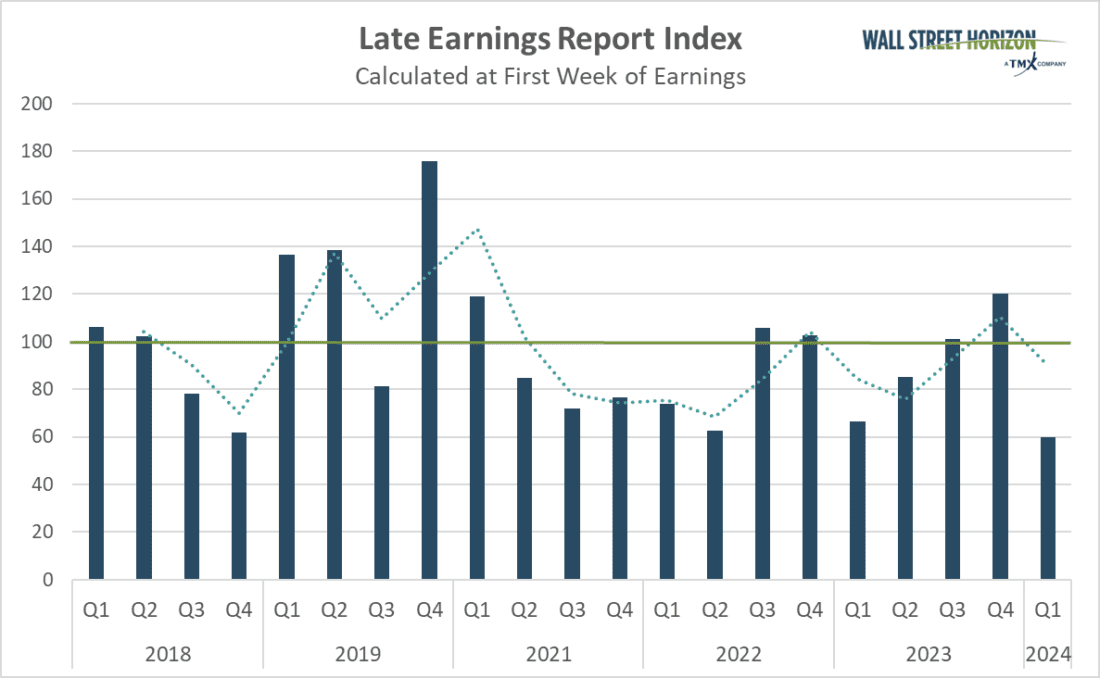

Despite the tone from some banking executives last week, our proprietary gauge of corporate uncertainty just clocked its lowest reading on record. Just as the Q4 earnings season gets underway, the most recent reading of the Late Earnings Report Index (LERI) shows that fewer companies are delaying earnings reports than advancing them.

The LERI tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, anything above that indicates companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests companies feel they have a pretty good crystal ball for the near-term.

The official pre-peak season LERI reading for Q4 (data collected in Q1) stands at 60, the lowest reading in the metric’s 9-year history. As of January 12, there were 37 late outliers and 56 early outliers. This is in stark contrast to the LERI readings from the Q2 and Q3 earnings seasons which showed CEOs at their most uncertain since the COVID-19 pandemic.

Source: Wall Street Horizon

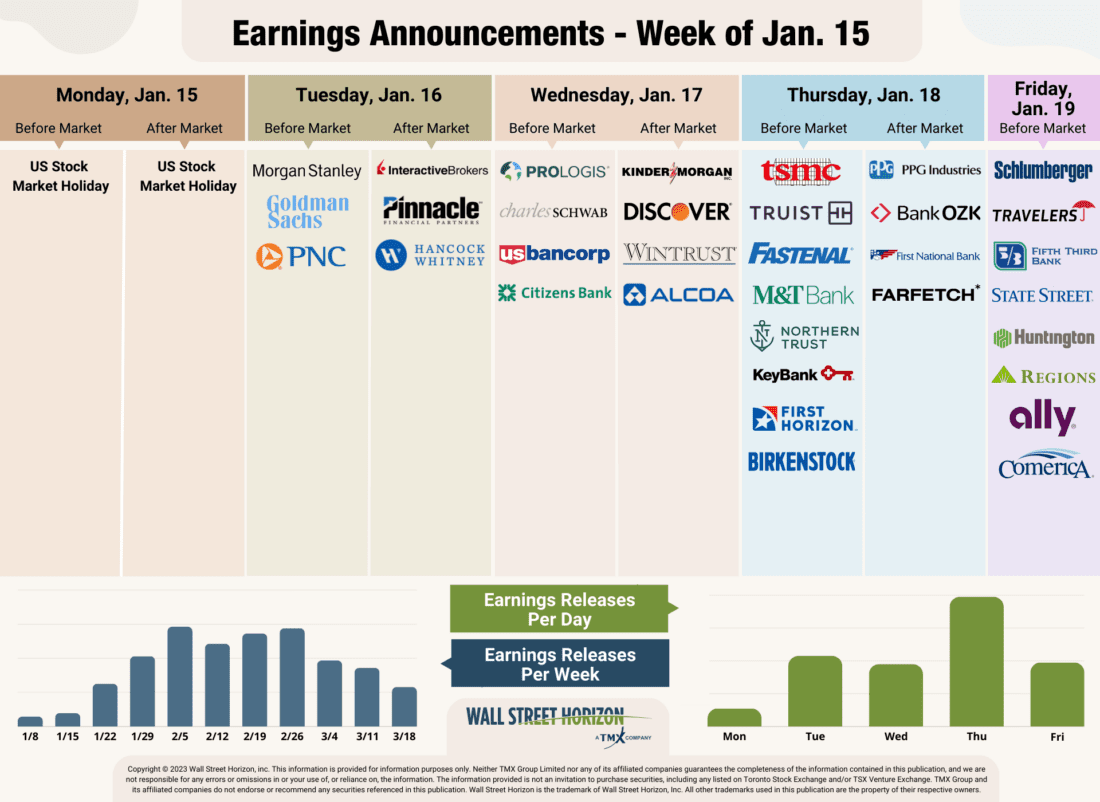

Financials continue to report this week, with big bank results wrapping up on Tuesday with Morgan Stanley (MS) and Goldman Sachs (GS). We also will get a read on semiconductors when Taiwan Semiconductor Manufacturing reports on Thursday, January 18, and on how a recent IPO is faring when Birkenstock releases results on that same day.

Source: Wall Street Horizon

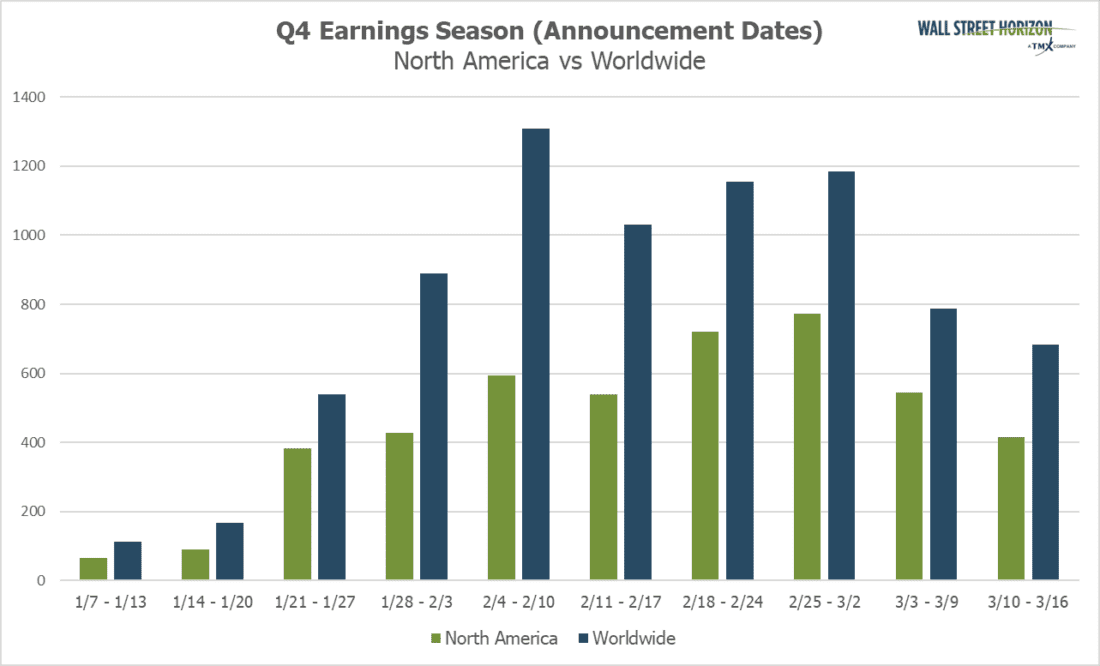

This season peak weeks will fall between January 29 – March 1, with each week expected to see over 1,000 reports. Currently February 22 is predicted to be the most active day with 599 companies anticipated to report. Thus far only 39% of companies have confirmed their earnings date (out of our universe of 10,000+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data. Keep in mind the Q4 reporting season is always a bit more prolonged, typically stretching over four or five peak weeks rather than the usual three peak weeks seen in Q1 – Q3.

—

Originally Posted January 16, 2024 – Despite Disappointing Bank Results, Corporate Uncertainty has Never Been Lower

1 Consumer Price Index Summary, U.S. Bureau of Labor Statistics, January 11, 2024, https://www.bls.gov

2 CME FedWatch Tool, CME Group, January 12, 2024, https://www.cmegroup.com

3 FOURTH-QUARTER 2023 RESULTS, JPMorgan Chase & Co., January 12, 2024, https://www.jpmorganchase.com

4 Fourth Quarter and Full Year 2023 Results and Key Metrics, Citi, January 12, 2024, https://www.citigroup.com

5 Bank of America Reports Q4-23 Net Income of $3.1 Billion, EPS of $0.35 Full-Year 2023 Net Income of $26.5 Billion, EPS of $3.08, Bank of America, January 12, 2024, https://d1io3yog0oux5.cloudfront.net

6 Wells Fargo Reports Fourth Quarter 2023 Net Income of $3.4 billion, or $0.86 per Diluted Share, Wells Fargo, January 12, 2024, https://www08.wellsfargomedia.com

7 Earnings Insight, FactSet, John Butters, January 12, 2024, https://advantage.factset.com

Copyright © 2024 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon’s prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!