- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 30, 2024 at 11:30 am

Markets are steady today as investors feast on a buffet of economic data and corporate earnings, while patiently awaiting a trifecta of significant information set for release tonight and tomorrow. Major big tech companies will release earnings after the closing bell today as investors will learn the duration allocation of yesterday’s better-than-feared level of quarterly borrowing from the Treasury tomorrow morning. Tomorrow afternoon features Fed Chair Powell’s commentary on monetary policy which will be pivotal for a marketplace that is expecting 5 to 6 cuts this year. In the meantime, hotter-than-expected economic data continues to dominate the floor, with consumer confidence and job openings rising sharply. These factors are capping gains at the moment, with market players wondering if this morning’s data will tilt the Fed’s rhetoric tomorrow.

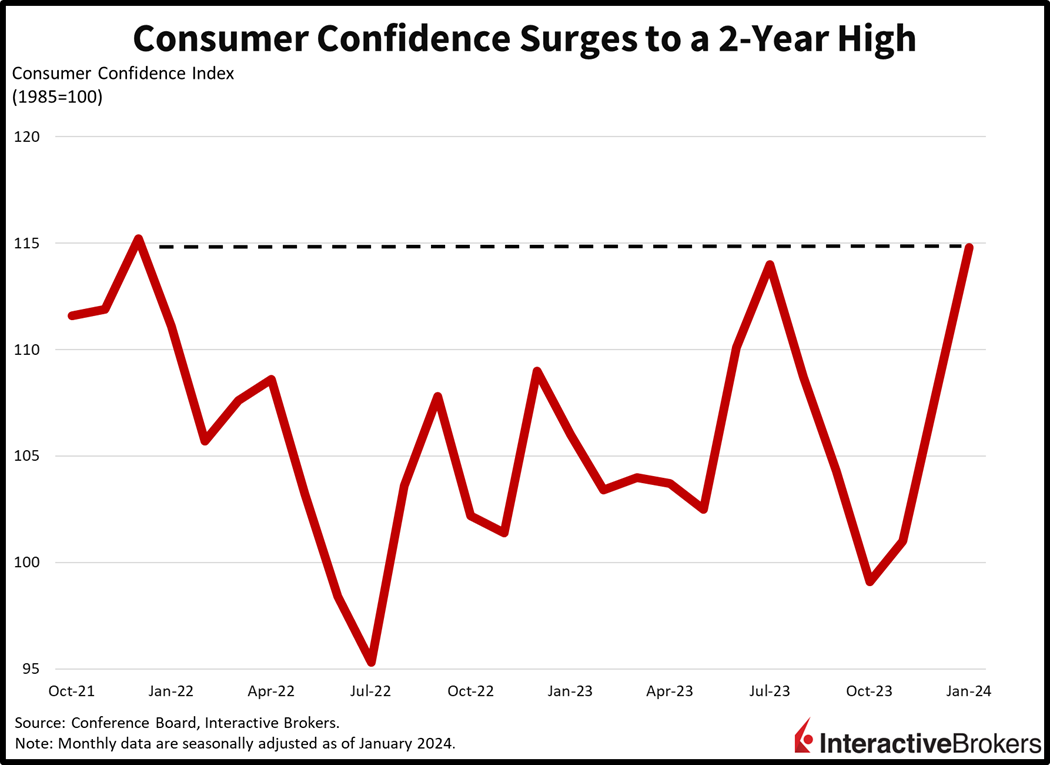

Consumers are feeling lovely as capital gains in their investment accounts, plentiful job opportunities and business possibilities support optimism. Notably, Consumer Confidence has surged to its highest level in over two years this month, reaching 114.8, in line with expectations and better than December’s 108. The present month’s reading, the highest since December 2021, was propelled by a notable increase in the Present Situations Index while the Expectations Index generated an increase of less magnitude. Indices for Present Situation and Expectations rose from 147.2 and 81.9 last month to 161.3 and 83.8 this month. Households also celebrated the outlook for lower interest rates.

Job openings rose to their highest elevation of the fourth quarter last month, surpassing 9 million for the first time since September. December’s 9.026 million in job openings was better than the projected 8.75 million and the previous month’s 8.925 million. The professional and business services category led with 239,000 additional job openings. Other top gainers included education and health services, up 73,000, and retail, up 50,000. In contrast, the leisure and hospitality and wholesale trade sectors weighed on the headline, surrendering 131,000 and 83,000 vacancies. Quits did decline to 3.4 million though, the lowest level in four years, as workers feel less confident about replacing their jobs amidst slower hiring.

Across the Atlantic the European Union’s statistical office, Eurostat, reported flat GDP growth for the last quarter. The figure exceeded expectations of an unchanged -0.1% pace of decline from the third quarter. The continent’s largest economy, Germany, accelerated its decline from 0.2% to 0.3%, however, as manufacturing order weakness continues to weigh upon results. France managed to offset some of the pain, accelerating from 0.6% to 0.7%. The region avoided a technical recession for now, defined by two consecutive quarter of GDP contraction. Against the backdrop, upcoming revisions will be important to watch.

Recent earnings reports depict businesses struggling with labor costs and in some cases reducing employee headcounts as they struggle to maintain profits. Consider the following examples:

Stocks are down and yields are higher today as one of Chair Powell’s preferred indicators, job openings, beat by over a quarter-million. Chair Powell frequently cites declining job openings amidst low unemployment as a favorable development concerning the trajectory of inflation. The ideal result is that the labor market cools and wage gains slow without massive layoffs, keeping money in people’s pockets, supporting consumer demand and capping consumer credit delinquencies. But the second consecutive month of increasing job openings supports wage increases, thereby boosting labor costs and working against the Fed’s 2% inflation target, likely tilting Powell’s talking points toward the hawkish side tomorrow.

All major US equity indices are lower with the small-cap Russell 2000 and tech-heavy Nasdaq Composite indices leading the charge; they’re off by 0.9% and 0.4%. The S&P 500 and Dow Jones Industrial indices are each lower by 0.1%, meanwhile. Sectoral breadth is deeply negative, with all segments lower except for financials, consumer discretionary and materials; they’re up 0.7%, 0.2% and 0.1%, respectively. Real estate, utilities and technology are leading the way lower, with the sectors down 0.8%, 0.6% and 0.4%. Bond yields reversed their trajectory lower after hot economic data tilted them the other way. The 2- and 10-year Treasury maturities are trading at 4.37% and 4.09%, 5 and 2 basis points (bps) higher on the session. Tighter Fed policy anticipations and stronger inflation expectations are helping the dollar, as its index trades at 103.55, up 9 bps today. The greenback is gaining against the pound sterling, franc, yuan, yen and Aussie and Canadian dollars while it loses ground relative to the euro. Energy markets are lifting price pressure projections against the backdrop of intensifying geopolitical tensions in the Middle East, including the Red Sea, and Beijing. WTI crude oil is trading at $77.53 per barrel, higher by 0.8%, or $0.60 cents on the session.

Tomorrow may be significant for markets, as the cross currents of big-tech earnings, the ADP jobs report, the distribution of Treasury issuance and Powell comments meet at a critical juncture. I’m expecting Powell to take some rate cuts off the market’s table by perhaps even calling current projections aggressive. The aftermath of the conference may shift the market’s pricing from five to six cuts down to three to four and lift yields notably as a result. Meanwhile, market players will be eager to hear about artificial intelligence (AI) developments from big tech. Are the projects boosting the bottom line? Or is enhanced profitability distant? On the Treasury front, Secretary Yellen may decide to continue funding the federal government through short-term borrowing rather than committing to higher yields over the long-term. With stocks near all-time highs amidst relentless animal spirits and irrational exuberance, tomorrow’s confluence of events may spark market volatility.

Visit Traders’ Academy to Learn More About Consumer Confidence and Other Economic Indicators.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Sell Mortimer, sell ,sell, sell , man