- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 11, 2026 at 12:57 pm

While there is no shortage of geopolitical news upon which we can focus today – more nighttime strikes in the Persian Gulf followed by threats to attack Iran’s Kharg Island tonight – that does not appear to be the main focus for traders today. If oil traders thought that the President was serious about that threat, those futures would be up sharply, not be roughly unchanged. Instead, let’s take another look at one of today’s biggest movers: Oracle (ORCL), which is dropping more than 10% despite solid earnings and guidance.

We have written numerous times about the necessary and sufficient conditions for a stock to rally after a quarterly report. It is necessary for EPS to exceed the published analyst consensus, but insufficient on its own. Positive guidance is the sufficient condition. After yesterday’s close, ORCL reported fiscal Q4 EPS of $2.11 (excluding items, of course), which nicely surpassed the $1.97 analyst consensus. Check. Guidance was decent. Total cloud revenue is projected to jump by 61%, a shade below the 62% average of analysts’ expectations. That’s a slight miss, but on a huge number. Bookings, most of which are for long-term, large-scale AI contracts, were $638 billion, well ahead of the estimated $589.5 billion. That seemingly should outweigh the ever-so-modest shortfall in revenue guidance. Unfortunately, this points to the root of ORCL’s decline.

Those bookings require data centers and the equipment necessary to fill them. Regarding that, the company said, “This substantially reduces the amount of capital Oracle must raise to build out our AI data centers.” Therein lies the problem – the company plans to raise another $40 billion in debt and equity in the coming fiscal year. And, as we noted last autumn, the main customer of those data centers requiring that buildout is OpenAI. Even then it was not clear how a money-losing startup might be able to meet its spending commitments, and that was before Anthropic seemed to be surpassing the company that brought agentic AI to the masses.

Investors love the idea of AI-related spending, but they’re a bit squeamish about the copious debt and equity that are affbeing raised to fund it.

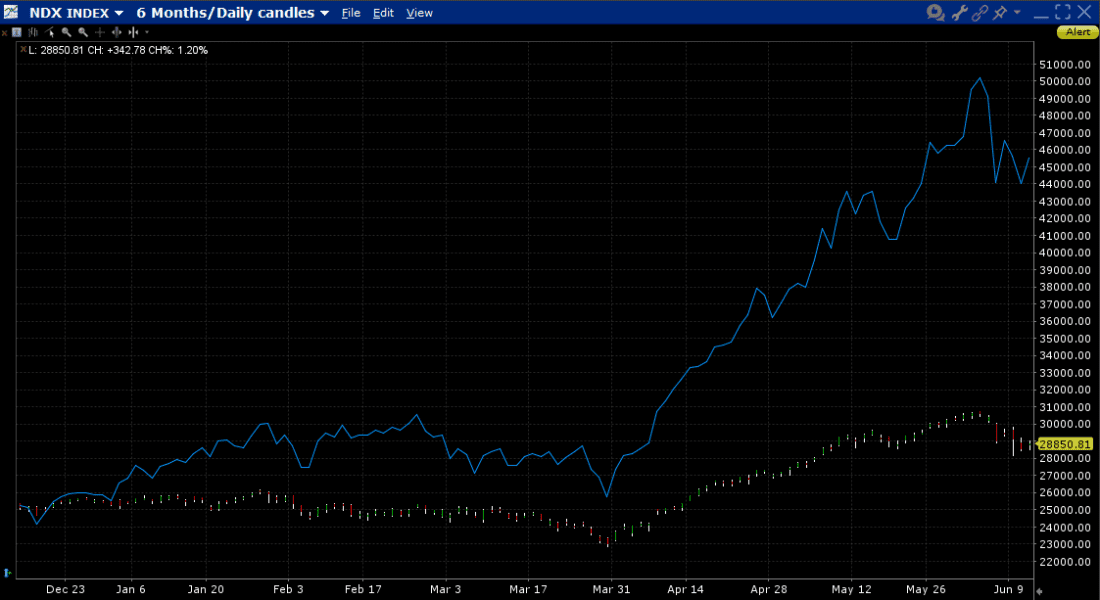

The stock prices of the beneficiaries of the largesse are vastly outpacing those of the spenders. There are various ways that we can portray the outperformance, but a simple way is to chart the Nasdaq 100 (NDX), which is dominated by AI behemoths, versus the Philadelphia Semiconductor Index (SOX). Certainly there is considerable overlap between the two – semiconductor manufacturers Nvidia (NVDA) and Micron Technology (MU) are the largest and fourth-largest components of NDX – but mega-spenders like Alphabet (GOOG, GOOGL), Microsoft (MSFT), Amazon (AMZN), and Meta Platforms (META) represent about 20% of NDX and 0% of SOX. (Interestingly, NYSE-listed ORCL is a component of neither.) Consider that SOX is up about 3.5% today, undoubtedly aided by ORCL’s affirmation of continued spending.

Source: Interactive Brokers

This leads us to two key points.

First, because many of the best performing stocks and sectors are recipients of copious AI-related spending, investors are increasingly dependent upon that tsunami of money. At the same time, however, investors seem to be souring – at least relatively speaking – on the companies that are selling shares and borrowing. What might happen, therefore, if some of those mega-spenders decide to listen to the message that investors are sending them?

My nightmare scenario, which I raised at a recent event, is that Alphabet’s Sundar Pichai or Microsoft’s Satya Nadella wakes up one morning and decides that he should take a breather from throwing endless amounts of money at all things AI. The faucet wouldn’t need to be turned off completely or even slowed to a trickle; it would just need to be turned down from full blast. The reaction from the wide range of companies that benefit from that spending would be huge.

Second, now that some of these companies are switching to equity funding alongside debt, we risk upending a supply/demand dynamic that has benefitted equities for several years. The overall supply of stock has been stable to negative for years, thanks to private equity buyouts and persistent buybacks. Now we find ourselves in a situation where a combination of announced and rumored stock sales disrupts that dynamic. Digesting that supply might simply be a “pig in a python” problem for now but is one that requires consideration.

The Oracle of Delphi was believed to deliver prophecies from the Greek god Apollo. We need to hope that its namesake, ORCL, is offering a murky, not an ominous, prophecy today.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Great read, thanks

I concur. AI is risky despite its continued potential upside.