- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 24, 2024 at 11:15 am

The Santa Rally is showing no signs of fatigue as we approach the last week of January, with market bulls cheering Netflix’s surprise increase in subscribers. Despite an ongoing series of hotter-than-expected economic data, the rally is resilient, supported by relaxed financial conditions driving economic activity. This morning’s S&P Global Purchasing Managers’ Index (PMI) exceeded forecasts, but tomorrow’s GDP report and Friday’s PCE Inflation print are likely to be more impactful upon investor sentiment. However, against this backdrop, market participants are expecting the first Fed cut to arrive in May rather than March, with robust data serving to extend the journey across the monetary policy bridge.

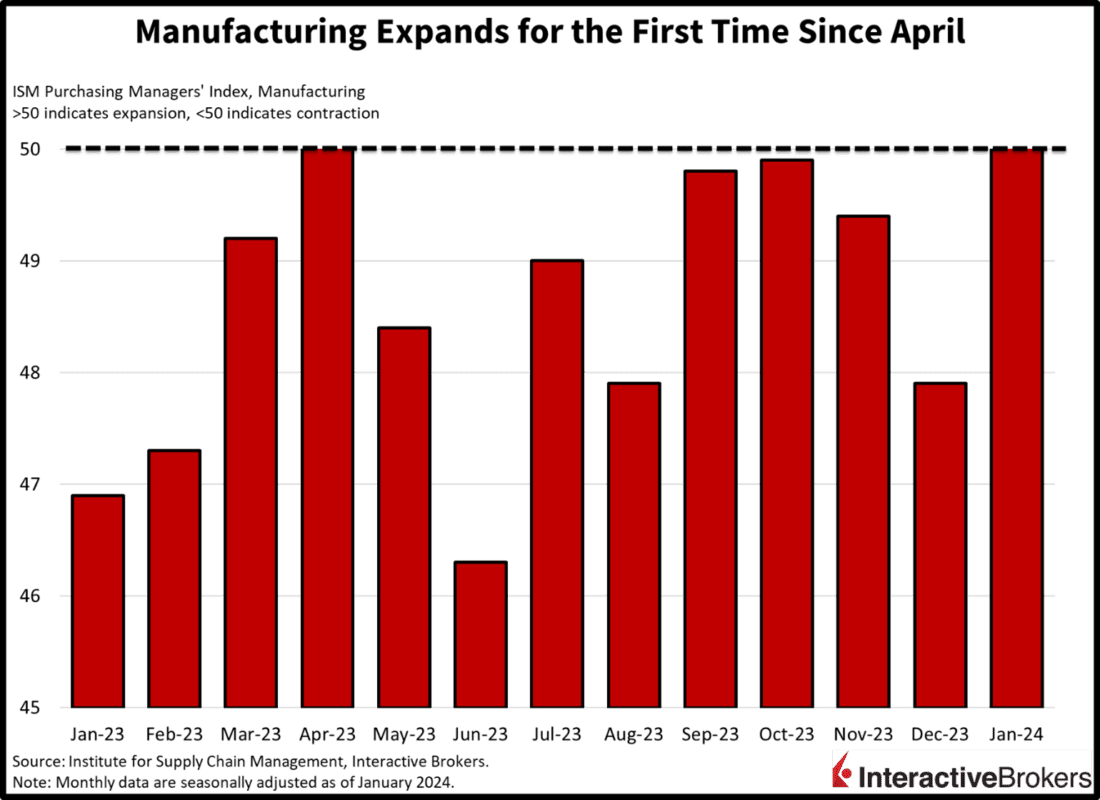

Today’s PMI reflected strong surprises, with manufacturing notably shifting from contraction into expansion. Business confidence was a key driver, propelling the positive change as retailers briskly increased inventories in anticipation of improved future performance. Additionally, input costs rose at the fastest pace since last April. These factors pushed the Manufacturing PMI to 50.3 this month, shattering expectations for an unchanged level of 47.9. The expansion marks the first month of growth in nine. However, weak demand and transportation delays from adverse weather and geopolitical conflicts weighed on performance. Employment also capped the headline figure, with goods producers marginally trimming headcounts.

The services sector also surprised to the upside, growing at a faster pace than December. The Services PMI of 52.9 exceeded the 51 projected and December’s 51.4. An uptick in customer traffic, which increased at the fastest pace since June, was the primary driver of the increase. Employment growth did slow down, however, as companies increasingly focus on efficiencies while only increasing prices marginally. These measures seek to boost worker productivity, maintain competitiveness and preserve margins. Similar to manufacturing, confidence also rose sharply, driven by expectations of potential Fed rate cuts boosting business prospects.

Across the Atlantic, European PMIs continued to indicate recessionary conditions with both manufacturing and services continuing to contract. The manufacturing sector contracted at a slower speed this month while services declined slightly faster as the segments reported levels of 46.6 and 48.4, respectively, versus 44.8 and 48.8 for December. Geopolitical conflicts weighed on Europe more than the US, with the Suez Canal turmoil significantly impairing supply chain conditions and intensifying price pressures. In fact, the rate of inflation jumped to its hastiest clip since May. New orders also weighed on headline figures, while employment and business confidence offset some of the weakness. The region’s largest economies, Germany and France, didn’t provide much optimism, however, with both nations experiencing sharp deteriorations in economic conditions.

Lower cost streaming entertainment options are gaining traction while in other areas of the economy, demand for natural gas is surging while semiconductor manufacturers are experiencing revenue weakness.

Bullish sentiments continue to dominate equity markets with all major US indices higher on the session. Unsurprisingly, technology is leading with the Nasdaq Composite Index up 0.8% while the S&P 500 is up 0.7%. Other leaders include the Russell 2000 and Dow Jones Industrial indices with gains of 0.5% and 0.4%, respectively. Sectoral breadth is split with the defensive health care, utilities and consumer staples sectors lower alongside cyclical real estate and materials. The other six sectors are higher, led by communication services, up 1.2%, and technology and energy, which are both up 1.1%. Energy is benefitting from a sharp increase in crude oil prices, driven by intensifying tensions in the Red Sea, a big draw in US inventories and optimism regarding stimulus from Beijing, the world’s largest importer. WTI crude is up 1.4%, or $1.07, to $75.52 per barrel, its highest level in four weeks. Bond yields are generally higher, with 2- and 10-year Treasuries trading at 4.37% and 4.15%; the former is unchanged while the latter is up 2 basis points (bps). The dollar is weaker as firmer monetary policy expectations out of Tokyo and Frankfurt weigh on the greenback. Specifically, the Bank of Japan is expected to lift its key rate into positive territory while today’s news of the sharpest Euro inflation since May points to a hawkish Lagarde. The greenback is down relative to the euro, pound sterling, franc, yen, yuan and Aussie dollar while it’s up against the Canadian dollar.

Since 2021, an important feature of short-term inflationary cycles is that when the marketplace and Chair Powell dismiss them, they somehow come back. January’s hot US economic reports portraying a robust December raise concerns for the rest of the year. Additionally, January’s PMIs indicate a global acceleration in inflation, driven by relaxed financial conditions and disruptions in the supply chain due to geopolitical factors. These developments have the potential to significantly amplify price pressures considering the Consumer Price Index bottomed at 3% last June. While December’s CPI was 3.4%, the ongoing developments may push the figure closer to 4% in the coming months, derailing plans for monetary policy easing and triggering substantial market re-pricings. If GDP and PCE inflation come in hot tomorrow and Friday, I’m expecting a mean Chair Powell to approach the mound at next week’s Fed meeting. He may even be as tense as at Jackson Hole in August 2022, when his remarks led to a 20% decline in equity markets in only six weeks.

Visit Traders’ Academy to Learn More About PMIs and Other Economic Indicators.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

Everyone thinks inflation is dead. No way. We are heading into the inflationary spiral of no return if the govt opens the faucet again. If it doesnt you are looking at a dark well of depression