- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 10, 2026 at 12:46 pm

One feature of the current global market environment is the popularity of leveraged ETFs. Leverage can magnify returns when markets are going your way, and in a relentless bull market – particularly for tech overall and semiconductors more specifically – the appeal of leveraged strategies, whether via options, futures, or leveraged ETFs, is relatively obvious. Unfortunately, as leveraged ETFs become more popular, many investors overlook their inherent pitfalls. These should be used only as trading vehicles. They systematically underperform when held for more than a day.

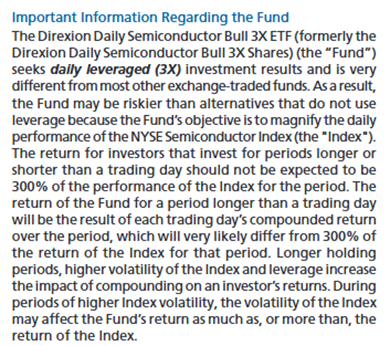

This nasty feature (or bug) is not hidden. In fact, it is typically disclosed, sometimes in bold letters, on the front page of a leveraged ETF’s prospectus. Here is an excerpt from page 1 of the summary prospectus of SOXL, the Direxion Daily Semiconductor Bull 3X ETF, which has become understandably quite popular among Interactive Brokers’ customers:

Now, honestly ask yourself when the last time was that you so much as glanced at a prospectus. One could theoretically accuse an issuer of hiding inconvenient facts in plain sight, but Direxion’s Head of Alternative Investments was quite candid about this “feature” on an IBKR Podcast from November. His comments immediately after the introductory pleasantries contained the following statements:

Andrew Wilkinson (Director of Trading Education, Interactive Brokers)

Now, Ed, what exactly are inverse and leveraged ETFs for the audience, and how do they differ from traditional ETFs or mutual funds?

Edward Egilinsky (Managing Director, Head of Alternative Investments, Direxion)

… leveraged and inverse ETFs are designed for short-term active trading, and I think you see significant daily turnover of assets and high volume with our products. And that denotes that this allows traders to express a magnified bullish or bearish view, as you mentioned, on broad industry sectors, broader indexes, and individual stocks as well. The leverage points will range from 3x in our case to inverse 1x, and the key is within the name of overall leveraged inverse ETFs. It includes the leverage point, the word “daily”—we’ll discuss that later—and the benchmark single stock it seeks to track. And the bottom line, Andrew: these are high-risk/reward vehicles, so not gonna be for everybody.

Andrew Wilkinson

Okay. Let’s dig down into that. Why are those ETFs then typically designed for single-day performance, and what happens when investors hold them longer?

Edward Egilinsky

Well, the objective is to seek to track the leverage point for a given single day. Once you hold these past one day, there’s gonna be something called compounding, and the leverage could work for or against you. So the trend is your friend. If your timing is wrong, you could have excessive losses. So let’s take a simple two-day example. I have $100 and I have a 3x bull fund. And for two days in a row, that underlying index goes up 5% each day. So you made 15% each day. But due to compounding, you are gonna be above that $130 mark after two days.

The flip side is if you have a two-day period where a 3x bull fund has the underlying index up 5% the first day, down 5% the second day. Ideally, you’d think you’d be back to your initial $100, but because of compounding, you are actually below your initial investment after two days and you’re at $97.75, so you’re actually down. So I think those are two simple examples of when the trend works for you two days in a row and when it’s choppy, where you have the index go up and down the same amount on consecutive days—that you’re below your initial investment in that example.

Mr. Egilinsky did a solid job of explaining the key benefits and pitfalls of these products. They can indeed magnify returns, especially during streaky markets when gains can be compounded. But once there is some back and forth, they tend to underperform.

Take special note of the final line in the prospectus excerpt above, that periods of higher volatility might result in that volatility affecting the fund’s returns. This creates an important paradox: traders might be more inclined to utilize leveraged ETFs during periods of high volatility, but that volatility might work against the holders’ returns. This is because leveraged ETFs typically utilize options to achieve their objectives.

Typically, higher volatility leads to higher options prices and faster decay. Therefore, if active investors flock to an ETF during a period of high volatility, its managers are forced to buy expensive, quickly decaying options. Furthermore, the ETF will eventually need to replace expiring options with new holdings that have longer expirations. Longer-term options are almost always more expensive than similar shorter-term ones. Furthermore, these funds need to re-hedge every day to match their desired exposures, making them price-insensitive options buyers. That combination creates a drag on returns for leveraged ETFs, particularly when held for longer periods of time.

The need for these ETFs to constantly replenish their holdings of decaying options with more costly ones led a senior executive at an ETF issuer who eschews leveraged ETFs to once describe them to me as “zero terminal value ETFs.” It means that over time, they will eventually erode their values without fresh inflows, which is why that fund family feels they are inappropriate for their long-term focus.

The bottom line is this: there are solid reasons why traders might find leveraged ETFs to be valuable trading tools (the above linked podcast offers several). But if these products’ issuers are candid about their pitfalls for investors, wouldn’t it behoove investors to listen? They utilize embedded options, and while the inherent risks and rewards of these options might be less explicit, they are still present. Hidden risks are still risks. Understanding those risks and not ignoring them in favor of a fixed focus on returns is crucial.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Complex or Leveraged Exchange-Traded Products are complicated instruments that should only be used by sophisticated investors who fully understand the terms, investment strategy, and risks associated with the products. Learn more about the risks here: https://gdcdyn.interactivebrokers.com/Universal/servlet/Registration_v2.formSampleView?formdb=4155

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!