- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 18, 2025 at 12:46 pm

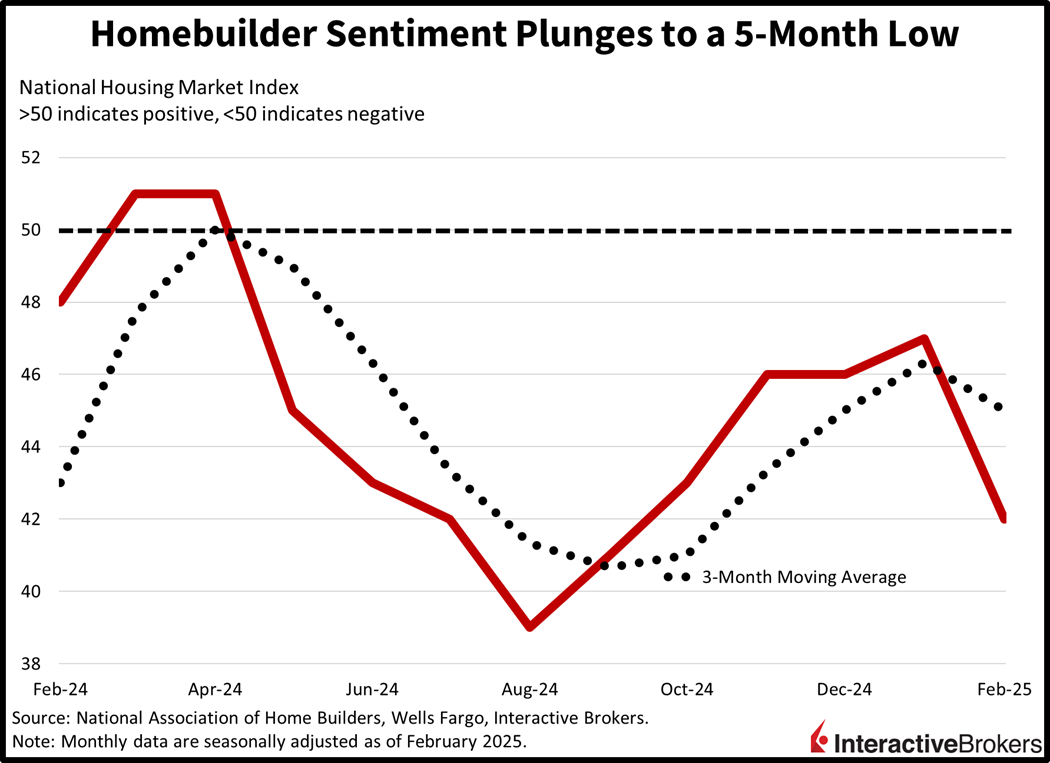

Optimism amongst market participants regarding the nearing of a potential ceasefire between Kyiv and Moscow sent stocks towards all-time highs in early morning trading. But a 10 am intraday homebuilder sentiment report derailed the momentum as industry players reported the lowest level of confidence in 5 months. Indeed, a shortage of home buyers, pricey costs for materials, heavy mortgage rates and tariff uncertainty are pressuring transaction volumes, much to the dismay of builders. The softening real estate sector, furthermore, isn’t serving to quell yields, which are rising and at their loftiest heights of the session. Equities are near their flatlines, meanwhile, as traders hope for a catalyst that can lift benchmarks out of their two-and-a-half-month trading range.

Homebuilder sentiment plunged to its lowest level since September as the headwinds of tariff uncertainty, rising costs and elevated rates weighed on affordability. The dampened outlook has essentially erased all of the progress in the months following the presidential election due to industry players seeing little that the White House can do to improve transaction volumes. The headline figure dropped a whopping 5 points to 42 this month, missing projections for an unchanged 47. All three major components of the gauge reflected pessimism, with the outlook for single-family sales in the present and the six-month future dropping from 50 and 59 to 46 on both fronts. The traffic of prospective buyers also slipped from 32 to 29 while all regions contributed to the decline, sporting weaker results month over month (m/m).

Manufacturing conditions are improving modestly in New York state this month, supported by rising orders, shipments and prices. The Empire Manufacturing Survey came in at 5.7 in February, better than the -1 projected and the -12.6 from January. Capping the overall gain, however, were contracting employment and shorter work weeks alongside worsening optimism. Sentiment was hurt by weaker expectations for capital expenditures as well as a dampened outlook for supply availability.

Markets are mixed with Treasurys losing, commodities and the greenback gaining and equities nearly flat. Major stock index performance is uneven with modest selling in the Dow Jones Industrial and Nasdaq 100 baskets met with limited buying enthusiasm in the Russell 2000 and S&P 500 benchmarks. Sectoral breath is nonetheless positive and led by utilities, industrials and materials, which are sporting gains of 0.8%, 0.7% and 0.7%. Only 3 of the 11 major segments are lower, characterized by consumer discretionary, communication services and health care dropping 0.5%, 0.4% and 0.3%. Treasurys are getting trimmed, however, with the 2- and 10-year maturities changing hands at 4.29% and 4.53%, 3 and 5 basis points (bps) heavier on the session. Pricier borrowing costs are helping the greenback, though, with its gauge up 22 bps as the US currency appreciates against most of its major counterparts, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Trade and geopolitical uncertainty are pushing up materials charges and silver, lumber, gold, crude oil and copper are gaining 1.6%, 1.3%, 1.2%, 0.6% and 0.1% as a result. WTI crude is trading at $71.80 per barrel as OPEC+ is seen delaying production increases despite President Trump calling for more supply.

Today’s real estate data depicts an industry that was far too exuberant in its expectations of lighter mortgage rates and softer inflationary pressures. Perhaps part of the cheerfulness stems from President Trump’s long tenure in the construction and property management sectors alongside his bias toward low financing costs. Meanwhile, solving significant societal problems like that of home affordability requires meaningful policies and sacrifices, measures that aren’t easy to enact. Finally, tomorrow’s data releases on building permits and housing starts will offer us a perspective on whether waning sentiment is being countered with buoyant activity. I don’t expect that to be the case since 7-handle mortgages are far too extended for most of the population to close transactions but the results could underscore an old-school Winston Churchill quote that alludes to watching what they do, rather than listening to what they say.

IBKR Forecast Traders are also predicting a decline in m/m construction activity in tomorrow’s New Residential Construction report from the US Census Bureau:

Source: ForecastEx

The Aussie central bank started its descent of the monetary policy stairs this morning. In a sign of growing confidence that Australia’s inflation is under control, the country’s central bank trimmed its cash target rate 25 bps to 4.10% and the interest rate paid on exchange settlement balances to 4%. It is the first easing in four years. When announcing the policy change, the Royal Bank of Australia (RBA) noted that considerable uncertainty exists, such as how long the recent recovery in consumer spending will continue and businesses in some sectors reporting having difficulty with passing higher costs on to customers. The bank also believes the lower interest rates are still restrictive. It has a target inflation rate of 2% to 3%. In December, the country’s underlying price pressure rate was 3.2%.

The UK’s 4.4% fourth-quarter unemployment rate was unchanged from the preceding three-month period and lower than the 4.5% economist forecast. December, however, portrayed a favorable job market for workers with average earnings including bonuses climbing 6% y/y, exceeding the median estimate of 5.9% and accelerating from the 5.5% increase in November. Average earnings without bonuses grew 5.9%, matching both November’s pace and projections. In another positive sign, the economy added 107,000 jobs in the final quarter of last year, up from the third quarter’s gain of 36,000.

Hong Kong’s labor market strength continued in the three-month period ended in January with the unemployment rate of 3.1% unchanged relative to the interval running through December. The country’s unemployment level was only 3% in the July to September timeframe, but for August to October, it climbed to 3.1% and has remained at the rate.

Canada’s headline inflation climbed 1.9% y/y and 0.1% m/m in January, according to the Consumer Price Index. The y/y result surpassed the forecast of 1.8%, which would have been unchanged from December while the shorter term metric matched expectations and reversed from the preceding period’s 0.4% decline. The Core CPI, which excludes energy and food because of their volatile prices, rose at faster rates of 2.1% and 0.4 y/y and m/m. In December, the y/y core gauge climbed only 1.8% but fell 0.3% m/m. The lion’s share of the y/y higher headline figure was driven by gasoline and natural gas prices while the food category declined for the first time since May 2017.

To learn more about ForecastEx, view our Traders’ Academy video here

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!