- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 8, 2026 at 11:30 am

For years, the automotive sector was considered one of the pillars of the global economy. Companies such as Tesla, BYD, Stellantis, Volkswagen Group and Toyota dominated industrial growth narratives and attracted billions in investor capital.

Today, however, a growing number of signals suggest that the sector may be facing a structural transformation rather than a temporary slowdown.

The key question for investors is no longer: “Which car company will win?”

The real question may be: “Will traditional car manufacturers remain the main winners of future mobility at all?”

One of the most common arguments from investors is simple: automotive stocks look cheap.

Many legacy manufacturers are trading at levels last seen nearly a decade ago. For example, shares of Stellantis recently returned to price zones comparable to 2014–2016.

At first glance, this appears attractive.

But low prices alone do not automatically create value.

In many cases, the market may simply be pricing in a structural decline.

One of the clearest warning signs comes from global vehicle sales data.

If we isolate traditional combustion-engine vehicles, the sector appears to have peaked around 2016. Since then, the industry has struggled to generate meaningful growth.

Electric vehicles temporarily revitalized the market, but even that momentum may be slowing.

Global car sales have stopped growing structurally — EVs are now masking the decline of traditional vehicles. Source: Our World in Data

The long-term issue is behavioral.

Younger generations increasingly live in large urban areas where owning a vehicle is expensive, impractical, and often unnecessary. Rising insurance costs, parking costs, congestion charges, and improved public transportation systems are gradually changing consumer habits.

Mobility demand still exists.Car ownership demand may not.

Much of the recent growth in electric vehicles has come from China.

That is important because China became the engine supporting global EV expansion. However, several investigations raised concerns about the sustainability and quality of this growth.

Recent reports highlighted practices where newly produced cars are sold to affiliated entities before being resold as “used” vehicles with nearly zero mileage. This artificially inflates delivery numbers and allows manufacturers to benefit from subsidies and incentives tied to sales volumes.

This creates an important distinction between:

For investors, that difference matters enormously.

Many investors focus almost exclusively on delivery growth.

But in capital-intensive industries like automotive manufacturing, margins and cash flow are often far more important.

This is where several EV companies begin to show weakness.

Even companies experiencing strong brand growth are seeing:

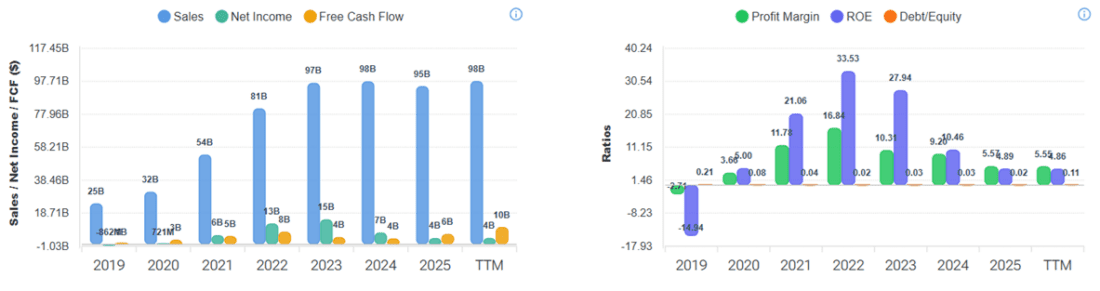

Take the biggest Chinese EV’s maker as an example (image above, source Forecaster Terminal), BYD revenue growth is slowing while profit margins and efficiency metrics continue to deteriorate.

Despite becoming the world’s leading EV seller by volume, the company operates with relatively thin profit margins. In highly competitive industries, thin margins leave little room for operational mistakes, pricing wars, or macroeconomic slowdowns.

The issue is not only whether companies can grow revenues. The issue is whether they can generate durable, scalable profitability.

Interestingly, even Tesla increasingly appears to be positioning itself beyond the traditional automotive business.

Much of Elon Musk’s strategic narrative now revolves around:

This shift may itself be a signal.

Perhaps the future value creation opportunity is not primarily in manufacturing vehicles, but rather in controlling the platforms, software, networks, and AI systems that power mobility.

Tesla is showing the same pattern seen in BYD: slowing revenue growth, weakening margins, and deteriorating efficiency metrics — further confirming the structural challenges facing the global auto industry. Source:Forecaster Terminal Financial Highlights

If fewer people buy cars, does that mean transportation demand disappears?

Of course not.

People will continue moving between cities, airports, workplaces, and homes.

What may change is how they access mobility.

That distinction could become one of the defining investment themes of the next decade.

This is where companies like Uber Technologies become particularly interesting.

Unlike traditional automakers, Uber does not depend on consumers purchasing expensive vehicles.

Instead, it operates a platform connecting transportation demand with transportation supply.

This creates a fundamentally different business model.

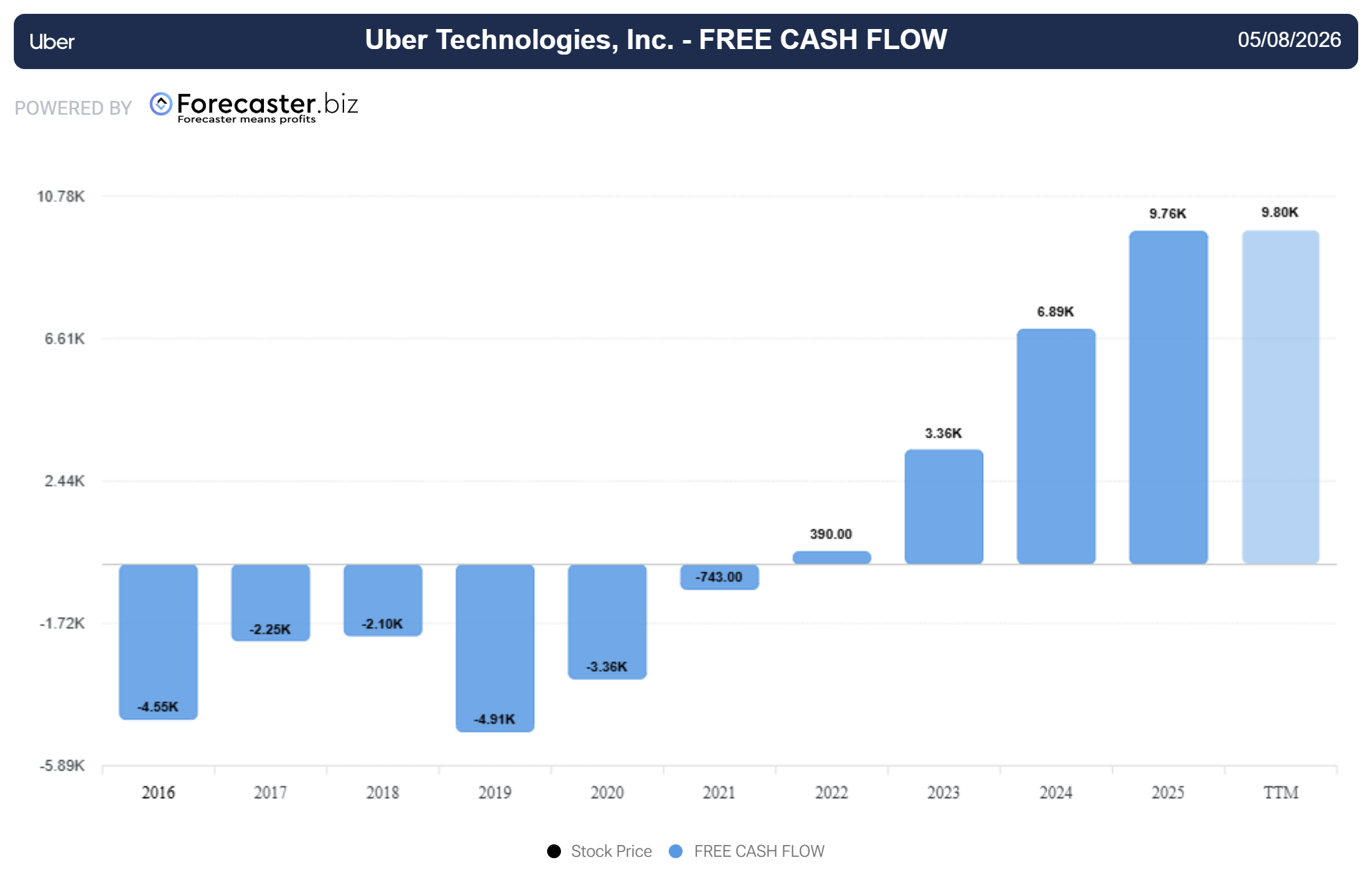

Unlike most car manufacturers, Uber is showing a completely different trend: rapidly improving free cash flow and a business model benefiting from the shift away from car ownership toward mobility-as-a-service. Source: Forecaster Terminal Cash flow Statement

In recent earnings releases, Uber even managed to rally after missing analyst expectations — a sign that investors may be focusing more on long-term positioning than short-term quarterly noise.

That dynamic is often important: Sometimes markets reward future strategic dominance more than current earnings precision.

What makes the Uber story even more interesting is that, despite the strong improvement in revenues, profitability, and free cash flow generation, the stock still appears significantly undervalued from a fundamental perspective. According to Forecaster’s multi-model valuation system — which combines Discounted Cash Flow, Peter Lynch valuation, Economic Value Added, and EV/Sales analysis. In other words, the market may still be underestimating how powerful Uber’s positioning could become in a world increasingly shifting from car ownership to mobility platforms.

Uber combines accelerating fundamentals with a stock price still trading more than 21% below its estimated fair value. Source: Forecaster Terminal

One of the most misunderstood aspects of the autonomous driving revolution is this:

The winners may not necessarily be the companies building the vehicles.

The winners could instead be the companies controlling the customer relationship and mobility network.

If robotaxis become mainstream, users will still need:

This is where platform businesses potentially gain enormous leverage.

Even if autonomous vehicles eventually reduce driver costs, the demand aggregation layer may remain the most valuable component of the ecosystem.

Another underappreciated factor is the impact of AI on operational efficiency.

Large technology-driven companies increasingly use AI internally to accelerate software development, automate workflows, optimize logistics, and reduce costs.

Uber recently disclosed that a large percentage of its engineering teams already use AI coding tools regularly.

This matters because AI may create widening productivity gaps between technology-enabled platforms and traditional industrial manufacturers.

In other words:

The future winners may be companies that combine mobility with software, AI, and network effects.

—

Originally Posted on May 8, 2026

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Forecaster.biz and is being posted with its permission. The views expressed in this material are solely those of the author and/or Forecaster.biz and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!