- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 21, 2024 at 9:45 am

The high points for economic data in the May 20 week should be the sales numbers for new and existing homes for April. Gauging the health of the housing market may be a bit tricky in reading these reports. Seasonal adjustment factors for this time of year anticipate a busier sales period as potential homebuyers shake off winter and start planning moves based on changing household needs.

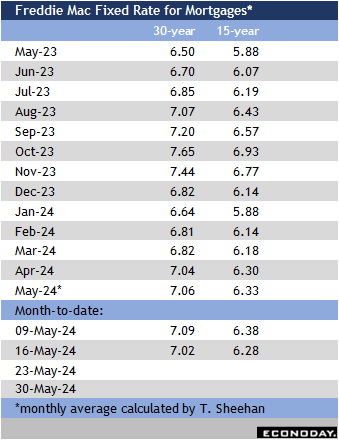

However, the housing market got a chill earlier this year when mortgage rates began to rise again and home prices did not ease up despite some slackening in the market. The Freddie Mac weekly report shows mortgage rates for a 30-year fixed rate note trending higher from 6.64 percent in the February 8 week to 6.88 percent in the March 7 week and then up to 6.82 percent in the in the April 4 week. Rates reached 7.10 percent in the April 18 week and have remained above 7 percent since then. Rates near the 7 percent-mark seem to be a point where potential buyers decide to wait for better rates, or, if waiting isn’t an option, to borrow with an adjustable rate. In any case, rates remain at levels not seen since before the Great Recession. The current generation of buyers entering the housing market is taking time to adapt to the reality that mortgage rates under 6 percent are not coming back any time soon. Buyers are and will remain rate sensitive in taking out a mortgage and are looking for any dips to lock in lower borrowing costs when they can.

The NAR report on sales of existing homes in April at 10:00 ET on Wednesday is for purchase contracts signed in February and March. As such, the buyers in these months had a lower rate which may have encouraged them to commit to a purchase with the prospect of rates going up. However, sales could have been restrained by a lack of supply. Those who currently hold mortgages with favorable rates – especially those taken out in 2019-2021 when rates were particularly low – are unlikely to put their home on the market absent a pressing reason. Competition is fierce for the more sought-after units.

The government report on sales of new single-family homes in April at 10:00 ET on Thursday is for contracts signed in that month. As such, the uptick in mortgage rates is expected to limit the number of sales as buyers for new construction could be willing to delay buying until a more favorable rate becomes available.

The minutes of the FOMC meeting of April 30-May 1 are set for release at 14:00 ET on Wednesday. These may be less informative than usual. There may be some nuance about the previously announced decision to reduce the monthly cap on reinvesting US treasuries from $60.0 billion to $25.0 billion starting in June 2024. However, the minutes are now three weeks out of date. FOMC participants have been talking about interest rate policy since the end of the meeting’s communications blackout period. Their recent comments combined with the economic data line up solidly for leaving the fed funds target rate at 5.25-5.50 percent until they achieve enough confidence that the inflation numbers are moving in the right direction again. Chair Powell’s remarks in the last few weeks have focused on the inflation performance in the first quarter. There’s a hint that disinflation is happening again after stalling for a few months. However, the April numbers are only one month’s data and the FOMC will want more than that before changing their rate outlook.

—

Originally Posted May 17, 2024 – High points for US economic data scheduled for May 20 week

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!