- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 3, 2024 at 10:45 am

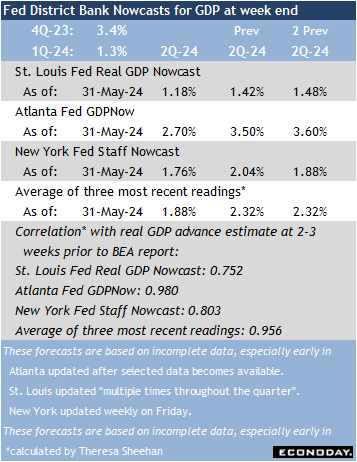

The June 3 week focus will be firmly on labor market conditions and how these might affect the upcoming FOMC meeting on June 11-12.

The monthly employment report for May is set for release at 8:30 ET on Friday. The change in nonfarm payrolls will be watched carefully to see if it disappoints or not versus market expectations. In April, nonfarm payrolls rose 175,000, a significant slowing from the first-quarter’s monthly average of 269,000. However, April’s increase reflects a healthy pace of hiring for an economy in modest expansion. Forecasts for May suggest that the upcoming report is expected to deliver a similar number of job gains as in April. If so, the cooling in the labor market would be much as Fed policymakers have anticipated as conditions rebalance and normalize.

There are three special factors that should be kept in mind for the May report. First, this is a five-week reference period for collecting establishment data (April 13-May 18). This slightly longer period could pick up a few extra workers hired late in April who were first paid in May. Second, some June graduates who have secured a job may have been already put on payrolls in May. This often occurs, but if it is more than usual as businesses snap up those with desired skills, it could be more noticeable in the numbers. Third, the relatively early timing of Memorial Day (May 27) might have prompted more aggressive hiring of workers in the travel and leisure sector and brought them on payroll a bit sooner than the normal hiring patterns.

The outlook for monetary policy should not be much changed if the payroll numbers come in close to market consensus. A materially weaker number could spark anticipation of a rate cut sooner, but without the inflation data for May, it would be a few days ahead of things. The CPI for May will be released on Wednesday, May 12 at 8:30 ET and might influence how the FOMC tweaks the language in the statement it will release at 14:00 ET. A cooler labor market combined with a resumption of disinflation might mean the timing of a rate cut looks a bit sooner. A cooler labor market combined with a sideways move or uptick in the CPI – particularly for housing and/or non-housing prices – would mean the FOMC will remain cautious and insufficiently confident about the path of inflation.

—

Originally Posted May 31, 2024 – High points for US economic data scheduled for June 3 week

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!