- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 31, 2026 at 10:45 am

Defence is undergoing a profound re-rating in the minds of policymakers, industrial planners and investors alike. What was once often treated as a cyclical and sometimes controversial corner of equity markets is increasingly being recognised as a structural theme tied to national resilience, strategic autonomy and technological leadership. Despite that shift, defence companies still account for only around 2.5%1 of the MSCI World Index, underscoring how underrepresented the theme can remain in broad global equity allocations.

Global military expenditure reached around US $2.7tn in 20242, marking the tenth consecutive annual increase and the sharpest rise since the end of the Cold War. Importantly, this is not simply a short-term replenishment cycle following recent conflicts. Defence budgets are increasingly being embedded into multi-year procurement plans, industrial policy frameworks and capacity buildouts that could support earnings visibility across the defence value chain for years to come.

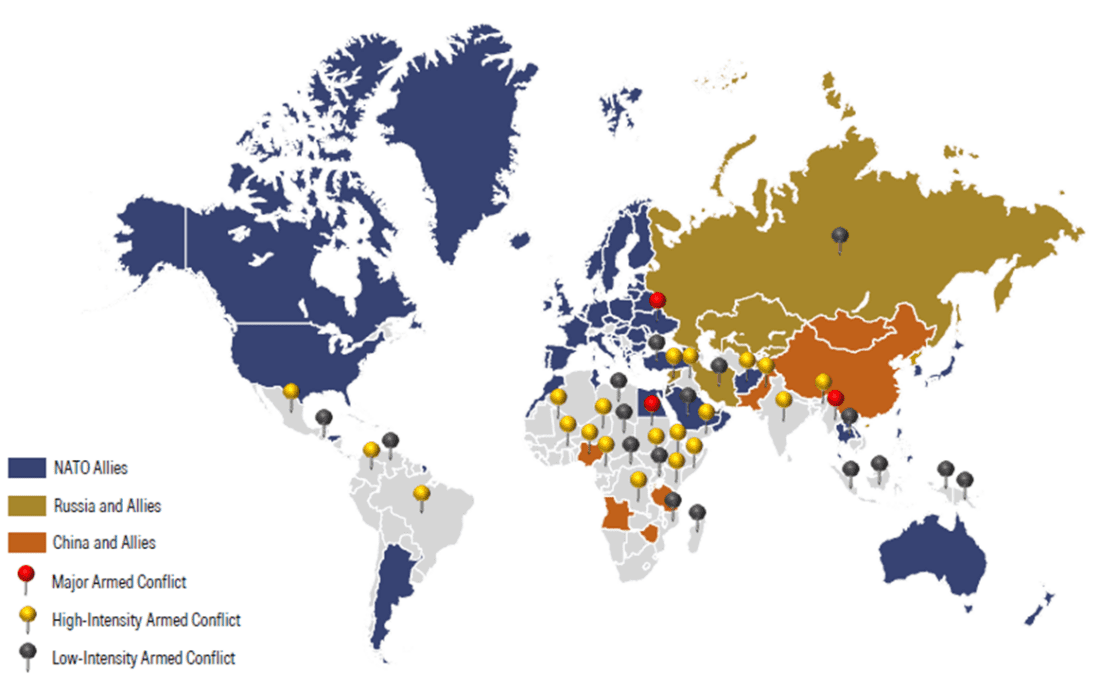

The first driver is a more persistent and geographically dispersed threat backdrop. Russia’s invasion of Ukraine accelerated rearmament in Europe, while tensions in the Indo-Pacific and instability in the Middle East have reinforced the need for deterrence, readiness and stockpile rebuilding on a broader global basis. The result is a higher baseline for defence spending, not only among countries directly exposed to conflict, but also among allies reassessing force posture, resilience and supply security.

Figure 1: Geopolitical tensions and security threats drive defence spending

Source: SIPRI Stockholm International Peace Research Institute, WisdomTree as of 10 February 2026.

The second driver is that the nature of defence spending is changing. The current cycle is not limited to traditional land, air and sea platforms. New spending is increasingly directed towards air and missile defence, drones and autonomous systems, cyber and electronic warfare, space-based assets, and C4ISR3 capabilities. That broadens the opportunity set beyond prime contractors to include businesses involved in sensors, software, electronics, secure communications and mission-critical subsystems.

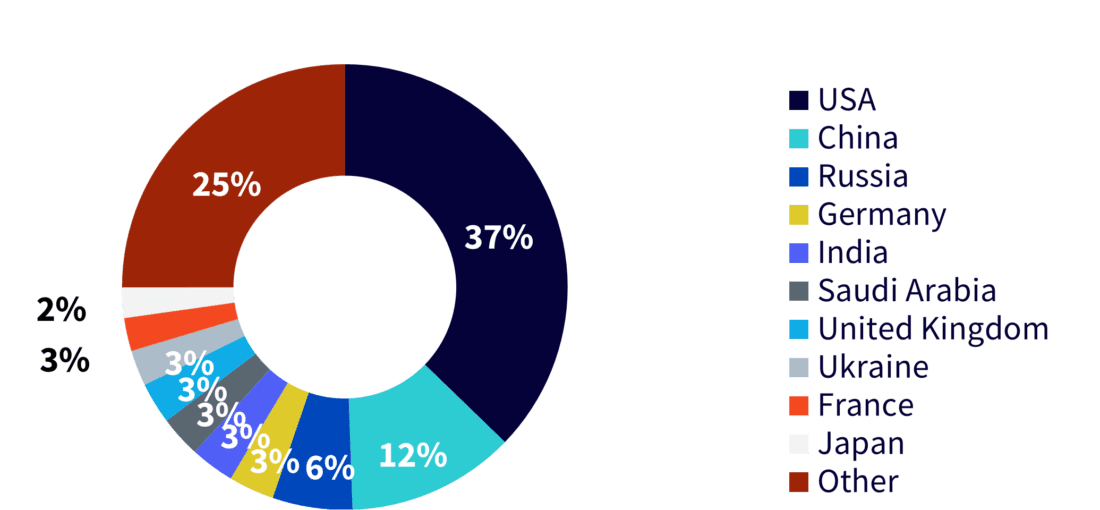

The third driver is that defence budgets are being supported by national strategy and alliance commitments rather than ad hoc responses. The ten largest military spenders account for roughly 75%4 of total global defence expenditure, highlighting how policy decisions in a relatively concentrated group of countries can shape the industry’s revenue outlook. NATO countries, meanwhile, allocate on average 58%2 of their total defence budgets to equipment, research and development, and maintenance, reinforcing the case that procurement and modernisation remain central to the current cycle.

Figure 2: Top 10 Global Defence spenders in 2024

Source: SIPRI Stockholm International Peace Research Institute, Morningstar, WisdomTree as of 30 June 2025. Historical performance is not an indication of future performance and any investments may go down in value.

For investors, this combination of geopolitical persistence, technological change and longer funding horizons points to something more durable than a short-lived sentiment trade. In our view, global defence markets appear to be in the early stages of a new supercycle, supported by both sovereign demand and industrial investment.

Why a targeted global approach matters now

A purely regional defence allocation can be powerful, but a global approach may be especially compelling at this stage of the cycle. The United States remains central to defence technology and procurement. Europe continues to accelerate rearmament and industrial coordination. At the same time, other markets are becoming increasingly important as both buyers and suppliers of defence equipment. A global strategy can therefore capture a broader mix of prime contractors, subsystem manufacturers and emerging industrial champions positioned to benefit from rising defence budgets, modernisation programmes and export demand.

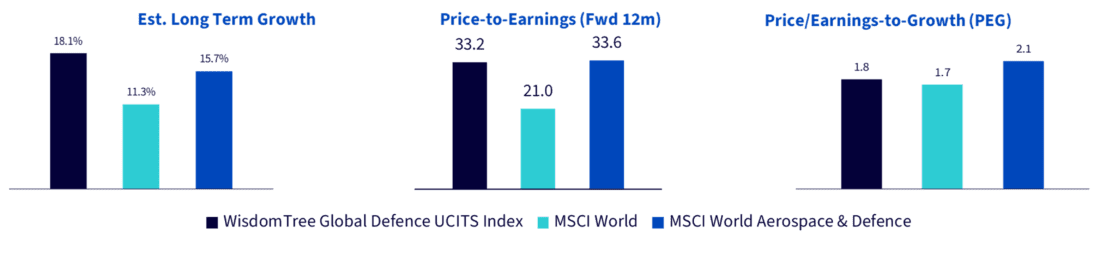

The WisdomTree Global Defence UCITS Index (Ticker: WTGDEFUN Index) currently has the highest estimated long-term growth rate among its peers at 18.1%. While its price-to-earnings (P/E) ratio appears elevated at 33.2x in isolation, this looks more reasonable when considered alongside its expected earnings growth. On this basis, the Price/Earnings-to-Growth (PEG) ratio is 1.8x, which is lower than that of benchmark indices.

Figure 5: Long-term growth and valuation metrics (forward P/E and PEG)

Source: WisdomTree, FactSet, Bloomberg, as of 31 December 2025. Holdings of the peers were sourced from Bloomberg. Fundamentals were sourced from FactSet. PEG ratios are based on forward P/E ratios and est. long term growth. MSCI World denotes MSCI World Index. MSCI World Aerospace & Defence denotes MSCI World Aerospace & Defence Index. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Compared with broader aerospace and defence benchmarks, WisdomTree’s approach tilts towards companies with higher direct revenue exposure to defence, while allocating more meaningfully beyond the US and Europe.

Conclusion

As security priorities harden and defence budgets become more deeply embedded in national industrial strategies, the investable case for the sector is evolving. Defence is increasingly moving from a niche satellite exposure to a more strategic allocation candidate within global equities.

—

Originally Posted March 31, 2026 – Global Defence: security as a secular trend

1 Source: MSCI Inc., latest available data as of February 2026.

2 Source: SIPRI Stockholm International Peace Research Institute, WisdomTree as of 10 February 2026.

3 C4ISR represents Command, Control, Communications, Computers, Intelligence, Surveillance and Reconnaissance.

4 Source: SIPRI Stockholm International Peace Research Institute, Morningstar, WisdomTree as of 30 June 2025. Historical performance is not an indication of future performance and any investments may go down in value.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!