- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 29, 2025 at 5:58 am

Your Weekly Roadmap with Jay Woods, CMT

1/ Key Data – PCE and Unemployment

2/ Magnificent Earnings

3/ Fed Quiet Period

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

Key Data – PCE and Unemployment

We enter the last days of April on the verge of a three month losing streak. The last time the S&P 500 had three consecutive losing months was August through October of 2023.

The good news is we are well off the lows. In fact, if you were able to tune out the day-to-day market noise you would have no clue about the wild swings April brought us. The S&P 500 sits -1.54% away from an even month, so let’s see if we can finish the month higher.

What will be some of those catalysts to keep the rally going?

Outside of the incessant tariff discussions, we have tons of hard data to sift through as economic data and earnings come into the spotlight.

Economic Data should be the big focus this week barring any more tariff negotiation volatility – key word “should”.

Let’s focus on that data and why it’s so important.

As we head into next week’s Fed meeting, the “data-dependent” Fed gets the two biggest numbers it needs to gauge the economy and their dual mandate of lower inflation combined with low unemployment.

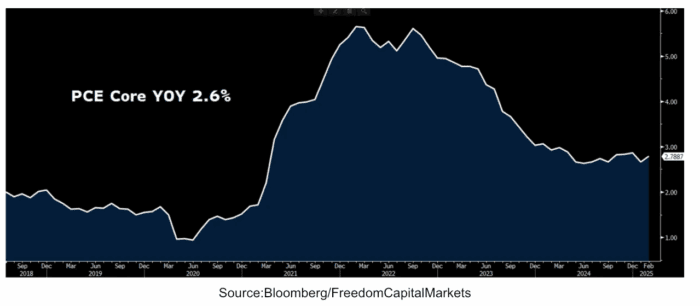

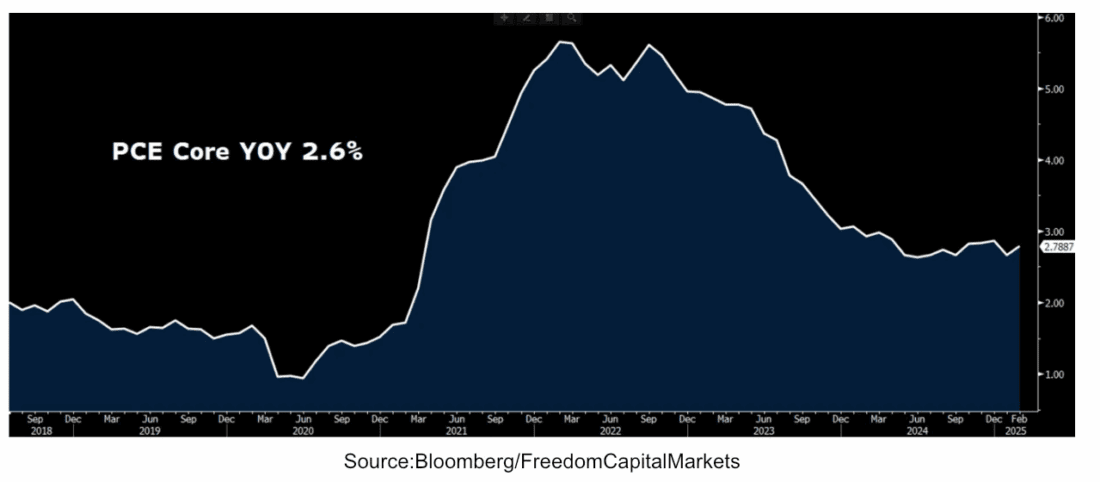

First up is Wednesday’s PCE data. The Personal Consumption Expenditures is known as the Fed’s preferred inflation gauge and its core reading is expected to drop to 2.6% down from 2.8%. That would mark the lowest levels since September when they began their rate cuts. This could give them real ammunition to possibly lower rates.

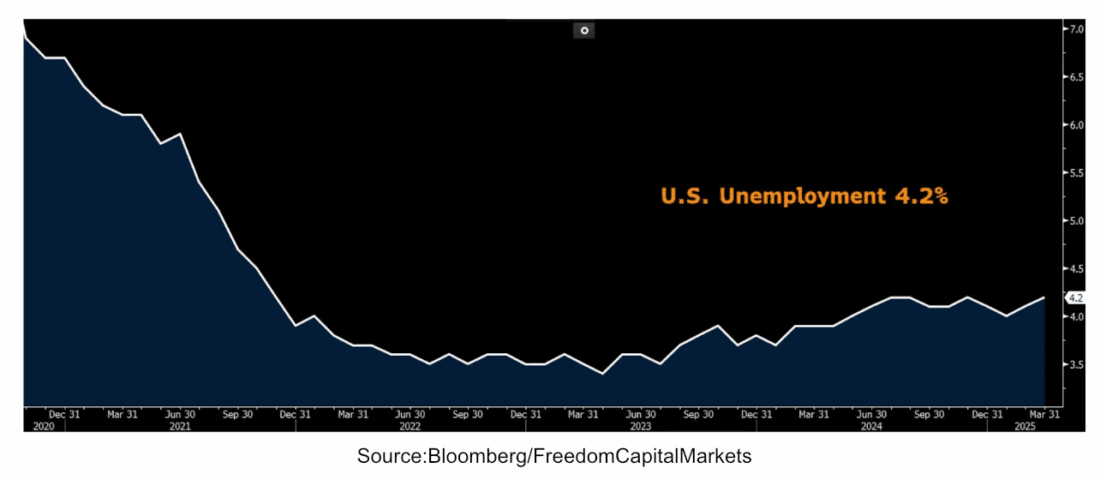

Then we get the second key piece of the Fed’s dual mandate in April’s unemployment report on Friday.

The numbers here also remain stuck in a narrow range, but still at historical lows. Expectations remain for a 4.2% number despite fears of recent layoffs and the impacts of DOGE. If these numbers surprise to the downside then the talk of a potential rate cut could grow louder.

Magnificent Earnings

Magnificent Earnings… Meta Platforms (META), Microsoft (MSFT), Apple (AAPL) and Amazon (AMZN) report this week and hope to build off their recent price momentum.

Considering we are dealing with the top market caps in the world, their price impact will move the markets. All but META are in both the Dow and S&P 500 and all four stocks are the top holdings in their specific sector ETF’s.

They all recently reached individual bear market territory and have much room to reverse to get back to old highs. Here’s a quick rundown on what to watch other than the obvious forward guidance and tariff impact.

🟢 META shares are 26% below their 52-week highs and currently embroiled in litigation which has taken CEO Mark Zuckerberg away from his daily activities.

Watch to see if reduced ad spending by Chinese companies SHEIN and Temu have impacted their bottom line. Also, how are recent AI initiatives and spending contributing to growth? Lastly, how much time are daily active users spending across their platforms?

🟢 MSFT shares are 16% below their highs and flat for the last year. The company continues to spend on AI and investors want to see how this investment is being integrated into their product suite and what impact that will have on revenue.

Another key focus will remain on its cloud services performance. Growth with Azure is expected to bolster its cloud operations.

🟢 AMZN shares are 22% below their 52-week highs. Like the other megacap growth stocks, AI monetization remains a priority. Investors are also focused on their e-commerce and consumer trends to get a better gauge to see if new spending habits are impacting the bottom line as expectations of tariffs grow.

🟢 AAPL shares are 19% below all-time highs and facing pressure in the Chinese markets. The company has announced plans to shift production to India. Investors are hopeful to gain insight on how progress is going in that endeavor and what impact that may have on the bottom line.

iPhone sales will also be scrutinized closely. They may have experienced a bump due to people rushing out to beat expected tariff increases that could cause severe price hikes. Lastly, what’s new in the pipeline? They usually reserve this for their semi-annual events, but a tease could come here as well.

Fed Quiet Period

Fed quiet period. Now that it appears the President has dialed down his criticism and threats of potentially firing Jerome Powell we can focus on the Fed doing their job. However this week they cannot comment on anything as we have hit the quiet period before next week’s FOMC decision. The lack of headlines may be a welcome change for the volatile markets.

Jerome Powell has made it clear that the Fed was concerned about the uncertainty and magnitude that potential and proposed tariffs could have on the economy. Now the data that will come into play ahead of their next rate decision, will that change their tune?

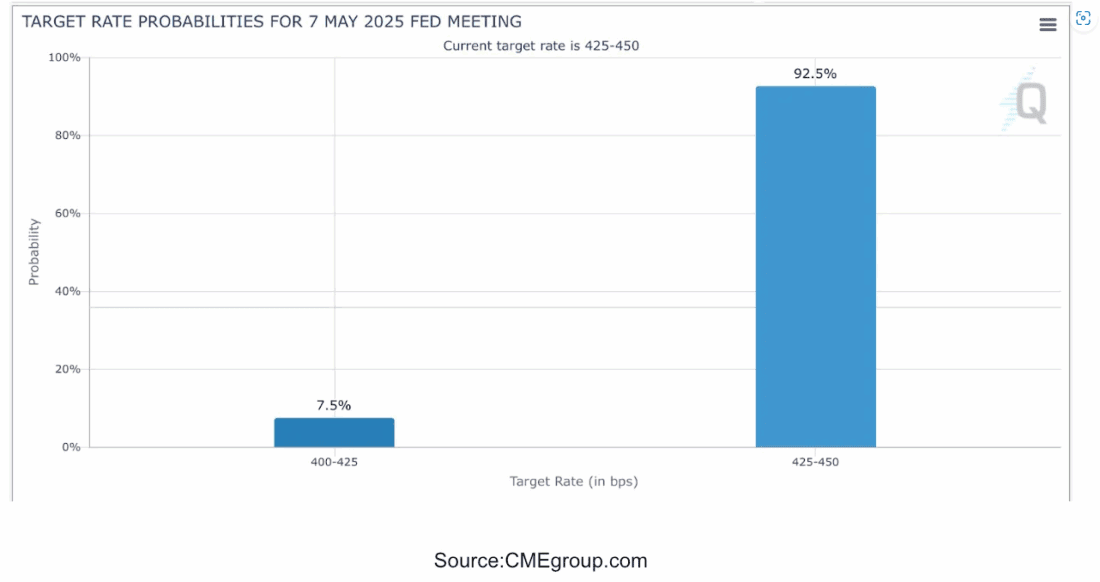

The expected data is still predicted to be quite sanguine. Currently, the odds of a cut, as seen above, show an extremely low probability of happening. The discussion for a cut could grow louder if the numbers come in surprisingly soft. Many of those cries are likely to come from the White House and that begs the question, would the Fed cave?

It could be a bad move for the Fed to give in and possibly destroy its integrity by cutting after the recent back-and-forth. We will do a deeper dive on this topic next week once we parse the data. It could set up for an interesting week and sadly, the Fed can’t comment.

Continue Reading on Freedom Capital Markets…

—

Originally posted 28th April 2025

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!