- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 13, 2026 at 12:15 pm

Who among us is old enough to remember the heady days when sustained rate cuts were a key underlying investment thesis for stocks? “But wait,” you say, “that was only a few weeks ago.” Indeed, it was, but expectations for those cuts have plunged recently. While stocks haven’t exactly been roaring ahead, the perceived change in monetary policy is being treated as yet another minor inconvenience for equities.

Yesterday marked a sea change in fixed income traders’ attitudes toward the likelihood of cuts in the coming year. We alluded to this yesterday, when we noted (albeit only in the third-to-last paragraph) that Fed Funds futures were no longer pricing in a 100% likelihood for a 25-basis point rate cut in 2026. Just six weeks ago, traders were anticipating a rate cut by June, another by December, and a roughly 40% chance for a third sometime this year. As recently as Tuesday, there was still a cut priced in for December, with a 19% chance for an additional cut sometime this year. Those expectations have now plunged to about a 91% chance for a cut by December, with a >100% chance for a cut not seen until June 2027!

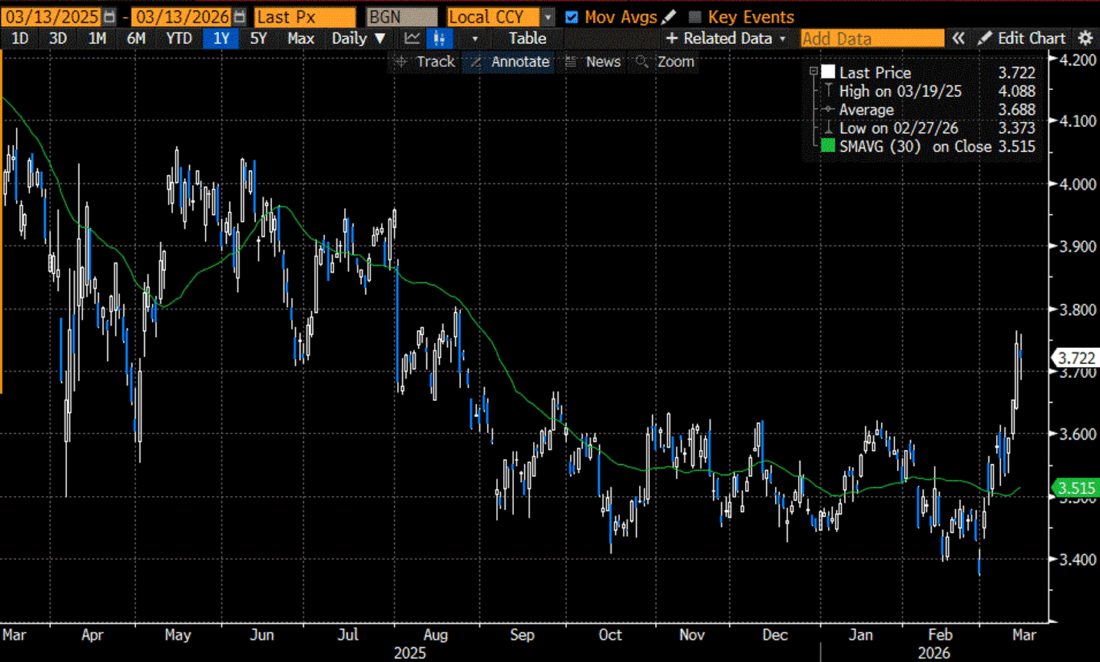

As a result, we saw 2-year Treasury yields rise by 9 bp yesterday, and by nearly 12 bp at their highest. Although they have improved by about 2 bp as I type this, we still only see a rate cut fully priced in for next March – a full year from now. A glance at a 1-year chart of 2-year rates shows that yesterday’s move represented a break above the trading range that had prevailed since September. This is despite an attempt to break below that range on February 27th, the day before hostilities began.

Source: Bloomberg

The rise in short-term rates is yet another in a series of relatively perplexing responses to the closure of the Strait of Hormuz. As we have discussed, this has long been one of the “black swan” events that risk managers feared. Conventional wisdom expected oil to rise to $150/barrel or more, a stock market correction of about 10%, and a flight to safety boosting the dollar and suppressing US Treasury yields. Although we can’t ignore oil near $100/barrel and the modest selling in global stocks, the magnitude of neither move is anywhere near the perceived worst-case scenarios. While the dollar has improved against a basket of major currencies, that too has been within normal trading parameters, leading us to be able to question how much can be attributed to safe haven buying versus how much it is because rates have risen.

Monetary policy can and should be fluid, responding to changes in credit markets, and of course to factors that influence the Federal Reserve’s dual mandate – stable prices and maximum sustainable employment. The problem for Fed watchers is that all those factors are murky at best and troublesome at worst. The spike in energy prices is obviously creating price pressures, even as Wednesday’s CPI and this morning’s Core PCE reports showed relatively tame inflation, albeit still above the Fed’s target. Last Friday’s employment report was unpleasant, to say the least, with a major shortfall in Nonfarm Payrolls and a rise in the Unemployment Rate despite lower Labor Force Participation, and today’s GDP revision showed annualized growth of a mere 0.7%. Fears of stagflation might be overblown, but nonetheless justifiable. Also, while credit continues to flow relatively normally through the system, concerns about private credit are beginning to resonate in financial conversations.

Bear in mind, there can be very positive reasons for rate cut expectations to fall. If the economy is robust, then there is little need for stimulative rate cuts. Unfortunately, “robust economy” does not appear to be the motivating factor behind the changing expectations. Instead, those reflect fears that price pressures are causing institutional paralysis. A Fed that is slow or unable to react to economic pressures becomes a headwind for markets. That may be why, despite everything that might justify a cautious approach from the FOMC, yesterday the President once again called upon Chair Powell (by name) to cut rates next week. I’m not holding my breath for that, either by next week’s meeting, or anytime soon.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!