- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 12, 2026 at 12:30 pm

Stocks were already selling off modestly before two significant statements about the Iran conflict hit the newswires and accelerated the declines. Neither President Trump’s nor the new Ayatollah’s comments could be viewed as market friendly, but while the latter was an angry threat to prolong and expand the conflict, it was pretty much what one might expect him to say. The President’s comments, on the other hand, challenged investors’ perceptions about a speedy end to hostilities and a fundamental tenet of US equities’ placid response to the crisis.

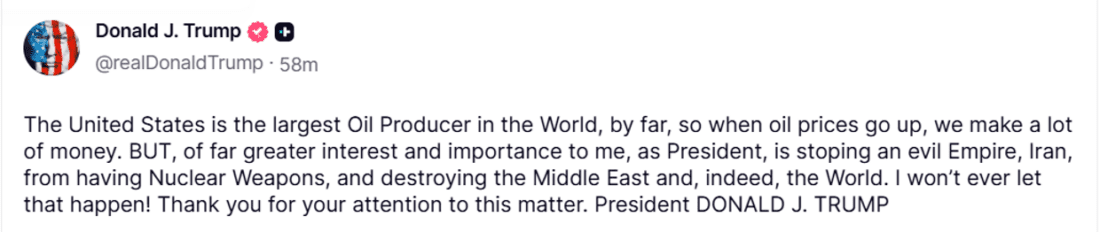

At 9:15 EDT, the following was posted on Truth Social:

Shortly thereafter, word reached global media from Iran’s state TV of the Ayatollah’s first message since assuming office. He said that the Strait of Hormuz would remain closed as a “tool of pressure”, and that Iran would continue to attack the Persian Gulf and open unspecified “other fronts” if the war continues. In the aftermath of both, crude futures rose by nearly 10%.

Neither of these can be considered favorable news by any means, but the latter is more of a reflection of the status quo. The theocracy in Iran remains defiant and unlikely to surrender in the short-term despite sustaining obvious catastrophic damage. The details are left to the imagination – including the Ayatollah’s condition, since he was neither seen nor heard – but it is an indication that their position remains firm for now.

The Truth Social statement, however, does challenge a fundamental perception that is rooted in equity investors’ psyches. Major equity indices’ relatively tepid responses have been predicated upon investors assuming a quick, relatively painless end to the actions. That assumption is reasonably rooted in precedent. Other US forays, such as the one in Venezuela, came to a rapid conclusion with virtually no lasting impact on stocks. The most significant market reaction to this administration’s policies came after the “Liberation Day” tariff announcement, and the initial tariffs were quickly amended after stocks flirted with a bear market.

The response to last April’s selloff led to two related concepts – the “TACO trade” and the “Trump Put”. Both refer to the President’s well-stated preference for solid stock market returns and his willingness to amend policies if markets appear to be voting against them. The Truth Social statement offered no reason to believe that the President had “chickened out”, as the TACO acronym implies, nor did it sound as though a change to a more market-friendly policy footing regarding the war was imminent.

Bear in mind, if we use the “Liberation Day” response as a precedent for the “Trump Put”, the “strike price” of that put was roughly -20% for SPX.

For perspective, US stocks have barely budged in response to a series of events that have been considered a major “black swan” for years. As I type this, the S&P 500 (SPX) is only down about 2.2% and above Monday morning’s intraday low of 6636.04. The same can be said for the Nasdaq 100 (NDX), though it is down by a slightly greater 3.5% margin. If you consider these to be major negative reactions to important global events – bearing in mind that crude oil is about 66% higher in that time frame (!) – then cash in your mattress might be a better investment vehicle for you.

Just because investors have considered themselves relatively impervious to risk does not imply its absence. Stocks’ generally blasé response so far is not a reason for investors to let their guard down.

One key pillar supporting stocks’ valuations has been steadily eroding as oil prices remain elevated. As I typed this, we learned that Fed Funds futures, according to CME FedWatch, were no longer fully pricing in a rate cut for the entirety of 2026. Current pricing now implies a 92% chance for a cut by December. Just six weeks ago, on February 5th, those traders were fully pricing in a rate cut by the June meeting, with a 14% probability for an additional cut, while two rate cuts plus a 42% probability for a third were priced in for December. Meanwhile, ForecastEx shows a 25% “YES” for “Will There be Exactly 1 rate cuts [sic] in 2026” and 24% for two cuts.

The changing perception about the potential for rate cuts is understandable, notwithstanding yesterday’s decent CPI report. A sustained rise in global energy prices will do nothing to ease FOMC members’ concerns about inflation and inflationary expectations. The committee tends to focus on core inflation, excluding food and energy, but they can’t be completely oblivious to pressures stemming from those factors. Nonetheless, stock traders still seem poised to pounce on opportunities to find tradeable rallies. Just before noon EDT, as I was finishing this piece, SPX had tried to bounce off its lows before fading once again. Despite everything, the prevailing sentiment still reflects a fair amount of FOMO.

While I don’t know what the opposite of a taco might be, it’s clear that FOMO is a key ingredient in Wall Street’s favorite TACO.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

Trump will never admit a mistake; a change in his behavior will be as close he will come to it. The low cost for Iran to close the Strait and the high cost to us for it’s closure, is an idea that obviously wasn’t contemplated by Trump or his advisors. It is hard to believe that the military didn’t think of it, but I’m guessing that they chose to keep their pay grade rather than offer a negative view. For sure he realizes that if they are still repatriating body bags in November, it will be curtains at the polls. I suspect that he will wish to be done and dusted by Labor Day at the worst. Will someone around him have the balls to tell him that Iran has no reason to adhere to that date? Meanwhile there will be more days like today. He may get a market reprieve by announcing “Victory” and a withdrawal of military assets from area, but that will only be lasting if he carries through. So I will be circumspect in selling puts in the meanwhile, unless I am eager to have the stock put to me at the strike price.

I will gladly pay a few more dollars at the pump in return for a disarmed and denuclearized terrorist regime.

i find it almost comical that you think the military dis not realize or plan for Iran trying to close the Straits. This conflict is being executed near flawlessly and they do NOTHING thats not well thiught out. They will open the straits when THEY determine its both safe and opportunistic. We are in solid hands with this military and its advisors, unlike the inept previous bumbling group.

Unfortunately, we aren’t paying a higher price only at the pump. Higher fuel costs for production and transport will be felt in everything, by everyone, world wide. And we don’t have the luxury of knowing the end date. This war has the potential of crippling global economies for years. I fear it may not be just a few more dollars at the pump. It’s criminal that this was not considered and planned for before deciding to start an “excursion”.

When can we declare independence from israel