- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 19, 2025 at 12:15 pm

If you slept late this morning, you missed most of it. Pre-market ES futures, which were down about -1.5% when I first checked this morning, seemed once again to wake up when US-based traders did the same. And now, about 90 minutes after the open, we’ve recouped almost all the early losses. Buy-the-dip strikes again.

The dip buying was not only seen in equities, but also in bonds. The latter part is more significant. The Moody’s downgrade, which removed the last AAA rating from US Treasuries after Friday’s close, directly addresses interest rate risks, not the stock market. That said, something that could negatively affect the creditworthiness of the USA has ramifications throughout the economy. If the “risk-free” rate is no longer quite as risk-free, that raises the cost of capital for everyone, which of course is a negative for all financial assets. Then late last night, the House budget bill, which has the potential to further expand the deficits that concerned Moody’s, passed through a committee vote that had previously failed.

Thus, a negative start for index futures. But the pattern of dip buying in stocks is quite well established at this point:

I’m of course being facetious, but it is not necessarily that far off from the now-routine behavior patterns we see. And the more a pattern works, the more it gets reinforced.

Yet we do have the aforementioned improvement in the bond market to thank for the sustainability of this morning’s bounce. Earlier today we saw yields higher across the curve, with notable steepening at the long end. At their worst, around 9:00 EDT, 10- and 30-year yields were about 10 basis points higher, while 2-years were up about 4bp. All three were breaching some key psychological levels — 2-yr > 4%, 10-yr > 4.5%, 30-yr > 5% — but they had all retreated below those points by about 10am. That justifiably bolstered the move in stocks.

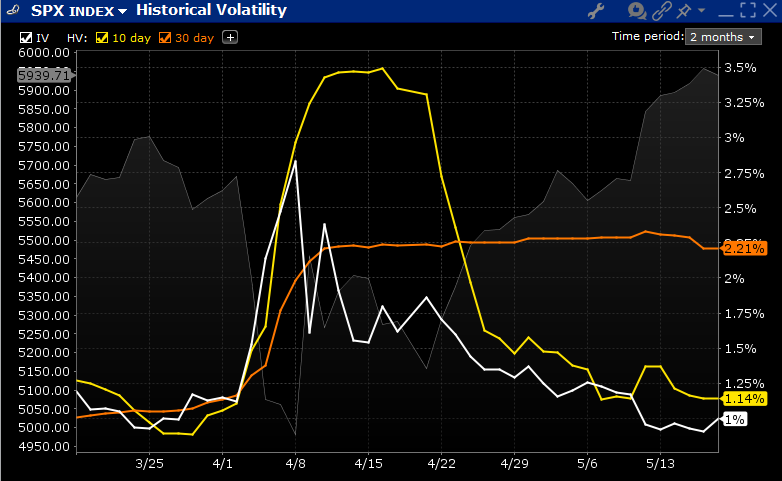

Despite the overnight jitters, VIX never cracked 20. Traders are pricing in a bit more volatility, but there is still not significant demand for hedges. Remember, despite the past volatility, VIX, which is a 30-day lookahead, has only moved from portraying relative complacency to very slight jitters. Traders are focused much more upon the recent plunge in short-term volatility than on the medium-term, as shown in the graph below:

Source: Interactive Brokers

Traders are going to keep doing what works for them until it no longer does. And apparently, with bond traders’ help, a downgrade was not enough to seriously disturb the usual patterns.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

If you were all in at the beginning of the year and went short after January, then reversed at the tariff pronouncement and bought again last month, you might be up 20-30% for the year. But only a 30 something thinks that they can time the market that well. Those of us who have more than a few thousand in the market, who believe in the virtue of diversification, who measure their performance in terms of years rather than daily or weekly, know going all in on the short term basis is a road to ruin. I may use option (selling) to express an option about the short term fate on a small portion of a position, but no individual option position will make or break me. As a whole, options may add 2-5% to my yearly return (which makes an appreciable difference when measured over decades) but the capital gains on the underlying positions is much more critical to portfolio performance.