- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 1, 2026 at 1:12 pm

After a week punctuated by hopeful talk, mostly on Tuesday and Thursday, about prospects for an extended ceasefire and/or peace deal in the Persian Gulf, oil and bond traders are expressing their disappointment at yet another lack of evident progress. Brent and WTI futures and bond yields were up modestly early this morning, but then took another leg higher when Iran said it would halt message exchanges with the US. Stocks once again yawned, only giving back some of their pre-market gains.

This type of behavior is nothing new. We’ve noted on multiple occasions that stocks, particularly those that are being boosted by aggressive AI spending, have been shrugging off inconvenient news about the Strait of Hormuz for several weeks now. The latest bout of enthusiasm that came to naught was on Friday afternoon. After reports on Thursday that a tentative agreement for a 60-day extension to the current ceasefire had been reached, the President said on Truth Social at 10:51 AM EDT that “I will be meeting now, in the Situation Room, to make a final determination” on the proposal. After a two-hour meeting, the President emerged from that Situation Room meeting with no update on whether a determination had been reached.

No determination, no matter. The S&P 500 (SPX) rose by 0.22% on Friday and the Nasdaq 100 (NDX) did even better with a 0.36% rise. Today, at noon EDT, we have SPX up 0.09% and NDX up by 0.46%, thanks to a 1.05% bounce in the Philadelphia Semiconductor Index (SOX). These modest bumps come despite roughly $6 jumps in both Brent (CO) and WTI (CL) futures and 7 basis point rises in 2- through 10-year Treasuries. There’s our ratchet.

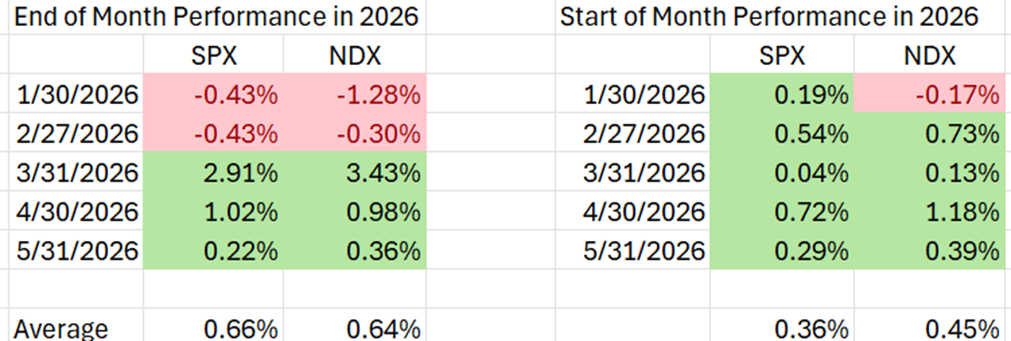

It is indeed possible that end-of- and start-of-month factors helped immunize stocks from the geopolitics. Stocks had a bit of a late pop just before the closing bell on Friday. We can see from the tables below that both SPX and NDX have risen on each of their last three month-end sessions, while SPX rose in each of the five prior starts to the month, with NDX only missing January.

Source: Interactive Brokers

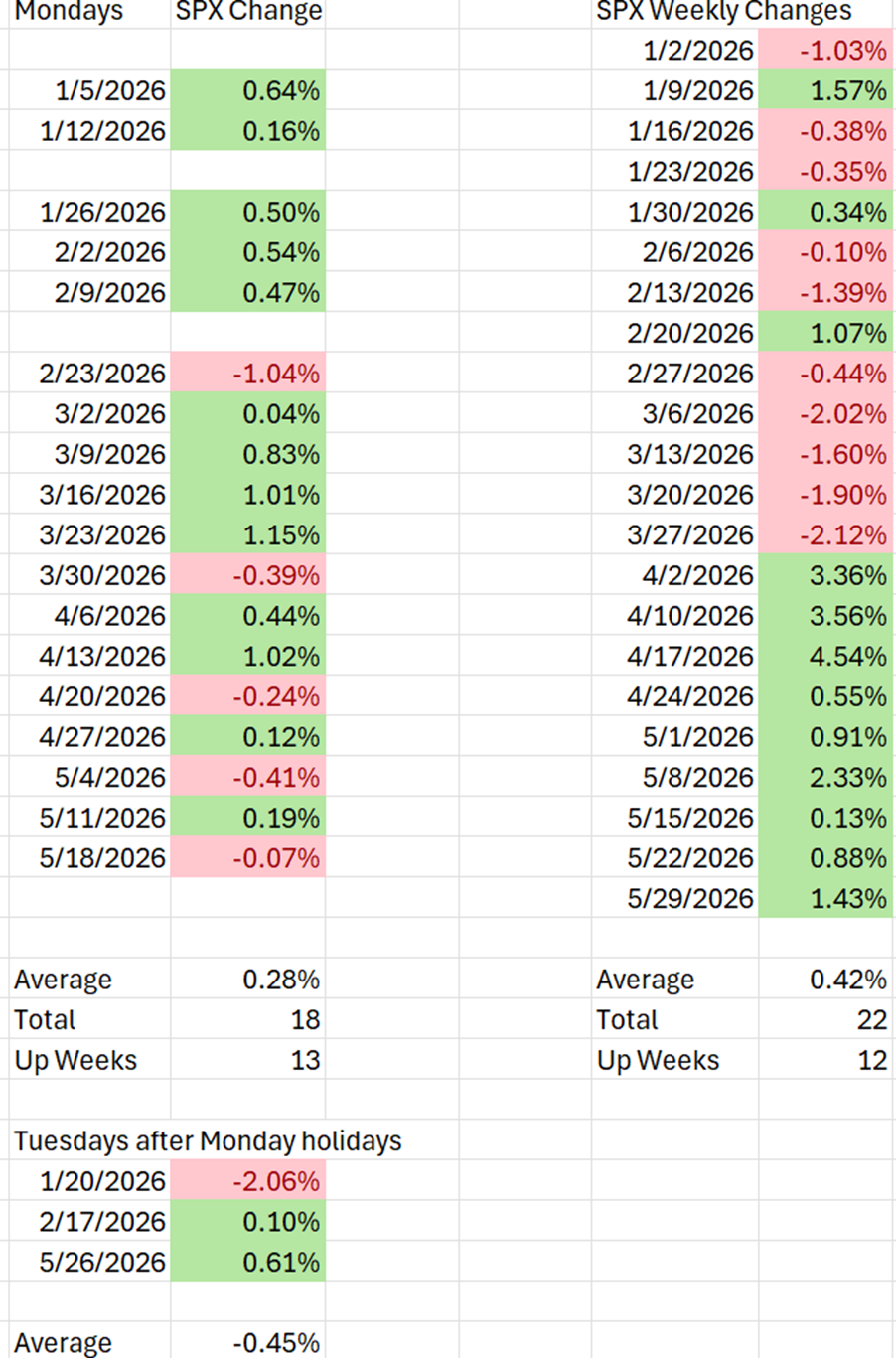

We have previously discussed the stock market’s predilection for Mondays, though that has not been quite as reliable – and certainly not as reliable as its recent streak of 9 straight weekly advances.

Source: Interactive Brokers

There is a fascinating but subtle data point in the table above. Of the 22 weeks that have been completed so far this year, SPX has risen in 12 of them. That’s not too shabby, even if it is a lower percentage than the 13 for 18 prior up Mondays that have occurred in 2026. But if I had asked you whether more than half of the weeks this year had seen a fall in SPX, I doubt that many of you would have thought that the benchmark was batting less than .500 on that measure. Even more interestingly, when we remove the current 9-week streak, it means that only three, yes, three, of the prior weeks have seen a gain in SPX. Not only can it be asserted that the current market advance is relatively tech-heavy, it is also very recent.

Equity investors have proven once again that they can put aside geopolitical concerns in favor of their unyielding focus on the earnings and guidance boosts that have bolstered tech stocks in recent weeks. We can debate whether they have extrapolated near-term guidance too far into the future, but for now, the combination of positive thinking and unyielding momentum has led to stock traders’ remarkable ability to shrug off the global factors that spook their bond and commodity counterparts.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!