- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 21, 2026 at 1:05 pm

Rebounding oil prices alongside stronger-than-expected economic data are driving investors to trim exposures to equity and fixed-income assets alike. Yesterday’s bullish recovery on Wall Street is failing to extend in today’s trading as earnings reports from AI juggernaut Nvidia and retail behemoth Walmart sent both names into losses amidst worries of intensifying competition for the former and cautious guidance for the latter, a result of softening consumer confidence tied to elevated fuel charges. Meanwhile, ongoing uncertainty related to the Middle East conflict and better-than-anticipated unemployment claims, housing starts, building permits and a 48-month high on the manufacturing PMI lifted yields across the Treasury curve in bear-flattening fashion led by the monetary policy sensitive shorter tenors. The jump in rates and the greenback is pressuring risk appetites, as all major stock sectors and subcategories are in the red minus the defensive utilities segment. Cryptocurrencies and non-energy commodities are also sinking in light of the session’s guarded mood; however, prediction markets are catching bids.

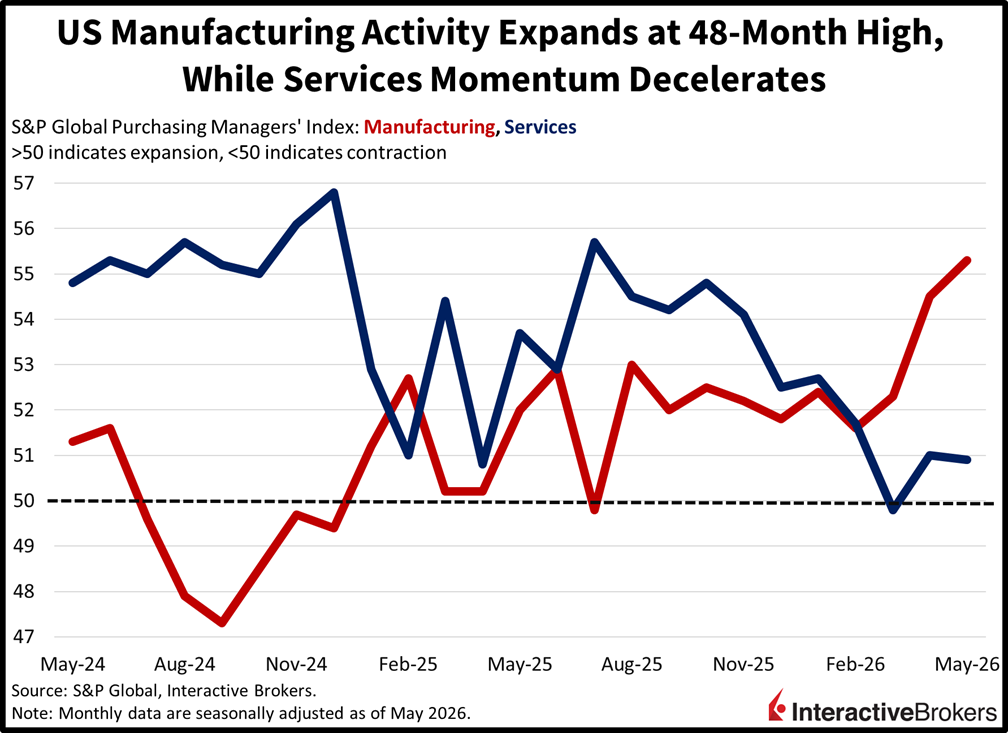

May’s economic growth is expanding at a similar pace as during April as an acceleration in goods production is offsetting a slowing services sector. The bifurcation across industries also exists in the sectors’ starkly different outlooks. S&P Global’s Flash Purchasing Managers’ Index (PMI) for manufacturing soared to a 48-month high of 55.3 this month, well ahead of the 53.8 median estimate and the previous print’s 54.5. Factories benefited from quickening output yields and rising inventories, which incentivized heavy hiring, even as sales remained subdued. Demand was especially soft in the international buyer category, in light of loftier prices and heavier financing charges. Conversely, services slowed as orders weakened on ascending inflation and firms trimmed payrolls as a result, with the segment coming in at 50.9, weaker than the 51.1 expected and the 51 from the prior publication.

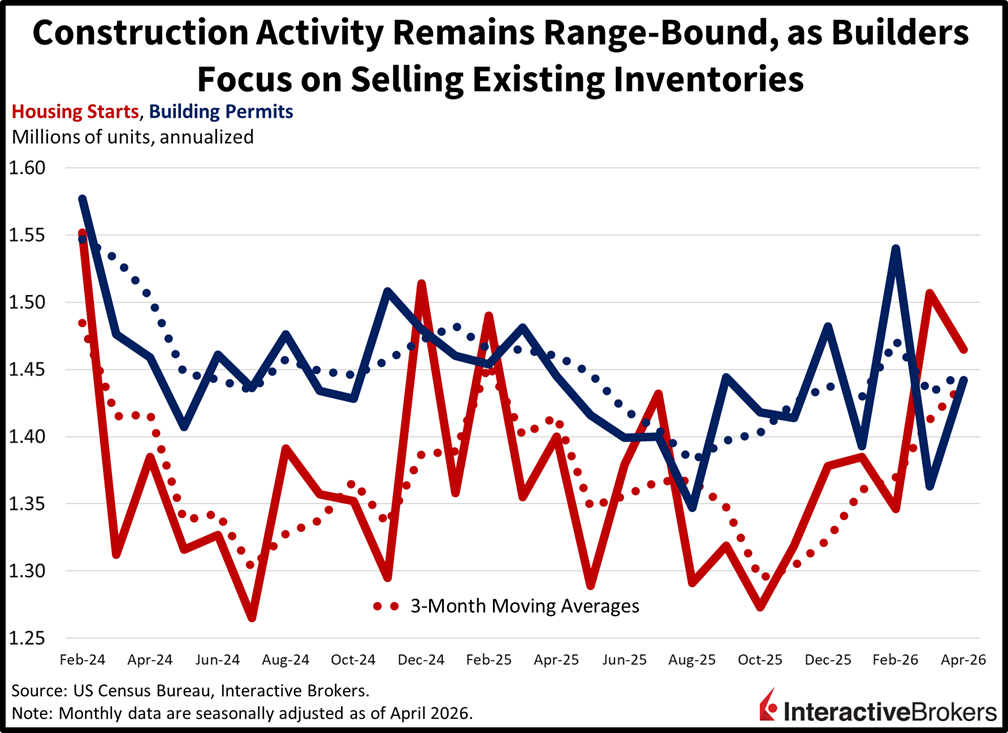

Construction activity remained rangebound last month as rising mortgage rates, expanding valuations, worsening affordability and growing inventories incentivized builders to focus on reducing their existing supply of single-family residences while starting fresh apartment unit rental projects. Still, April housing starts and building permits beat expectations, coming in at 1.465 million and 1.442 million seasonally adjusted annualized units (SAAU), ahead of the 1.41 million and 1.39 million anticipated. The results compare to March’s 1.507 million and 1.363 million. Dwellings with five units or more grew across both segments, with momentum quickening at 14.3% and 22.7% month over month (m/m) rates; however, singles fell 9% and 2.6% m/m. Geographical performance was evenly positive, generally speaking, although the tempo of the South’s starts and the West’s permits decreased 11% and 5% m/m, respectively.

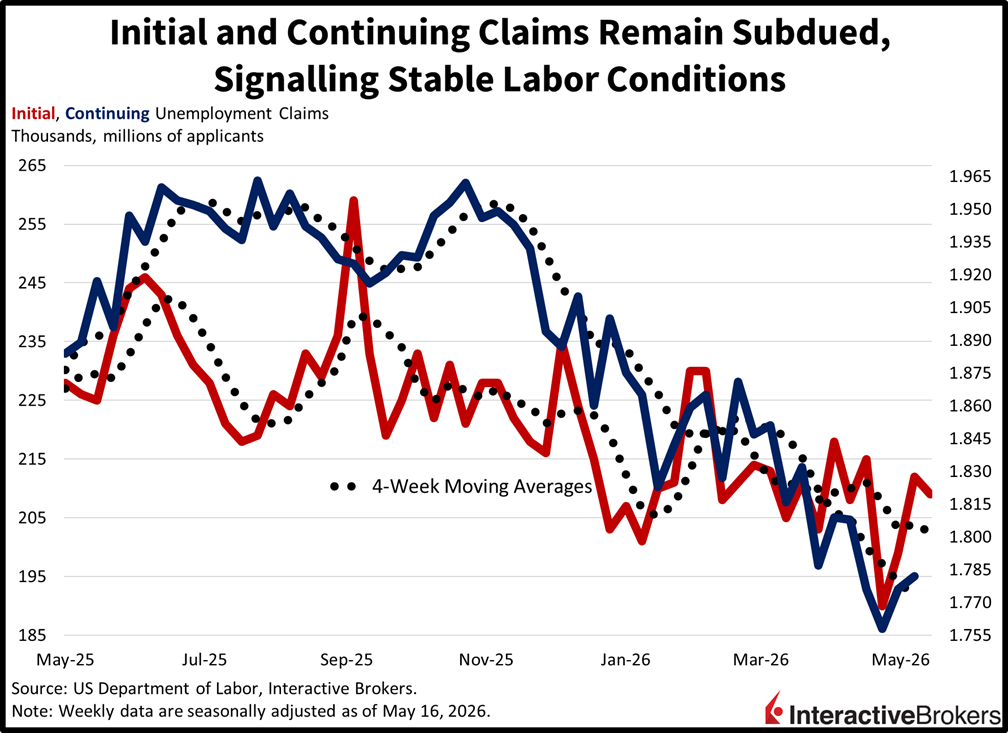

Unemployment claims were little changed in the past two weeks, but nevertheless they were lower than expected as labor reports continue to reflect employment stability. Initial filings dropped to 209k during the week ended May 16, under the 210k projected and the 212k from the prior period. Continuing applications for the seven-day interval culminating on May 9, meanwhile, depicted a modest increase to 1.782 million from 1.776 million, although the print arrived beneath the anticipated 1.790 million. Four-week moving averages were virtually flat at 202.5k and 1.773 million.

Despite the substantial lift in interest rates and slowing tech-sector momentum, stocks are only 1.3% off their record high reached seven days ago. Equity bulls continue to have a multitude of levers to pull as virtually every dip in the major indices gets bought, and today’s rate hike anxiety and Middle East concerns are being countered by optimism about economic growth driven by the ongoing AI buildout. Meanwhile, the potential for turbulence will be subdued in the next few sessions, with a lack of significant earnings calls or high-impact market-moving data scheduled prior to the Fed’s preferred inflation gauge hitting the wire near the end of the month. A VIX looking to break below 17 is emblematic of the relative complacency on Wall Street as there seems to generally be no bears left.

The euro area’s economy is on track to sink by 0.2% this quarter with the region experiencing an increasingly severe toll from the Middle East crisis, according to S&P Global. The organization also believes that inflation is likely to climb to 4%, creating a challenging scenario for policymakers. S&P reached the conclusions based on the May Flash Eurozone PMI Composite Output Index, which fell from 48.8 to 47.5, a 31-month low and missed the economist consensus for a repeat of April’s print. A reading of 50 is the contraction-expansion threshold.

The services and manufacturing sectors both contributed to the weakness. Perhaps most significant, the services PMI sank 1.2 points to 46.4, the lowest level in 63 months and below the economist consensus estimate of 47.8. In this sector, higher energy costs have caused consumers to curtail spending. The manufacturing PMI also weakened, slowing from 52.2 to 51.4, a three-month low. Economists anticipated a decline to only 51.7.

Manufacturing output slipped, falling from 52.3 to 51, a four-month low. During the month, intensification of cost pressures pushed input prices higher at the fastest rate in three-and-a-half years while the ascent of output stickers also accelerated. The US-Iran war has triggered supply chain delays, which S&P Global described as severe. The problem caused stocks of input items to decline despite firms trying to build inventory to provide safety against growing economic and geopolitical risks. Demand resulting from precautionary inventory building, however, is already starting to fade. The ongoing declines in output, new orders and employment, furthermore, accelerated and business sentiment continued to fall.

Consumer confidence in the euro area climbed this month but is still below the long-term average and levels that existed prior to the Middle East crisis, according to the European Commission. The organization’s Flash Consumer Confidence Index went from -20.6 to -19, a stronger showing than the economist consensus estimate of -21. In a related manner, the Economic Sentiment Indicator (ESI), which includes data from surveys of consumers and businesses, slipped from 96.3 in March of 91.7 last month. Also in April, businesses’ hiring plans fell with the Employment Expectations Indictor (EEI) decreasing 4.6 points. Both gauges depict their long-term averages with a score of 100.

Japan’s trade last month defied expectations for a deficit of ¥29.7 billion with exports exceeding imports by ¥301.9 billion, or roughly $1.9 billion. In March, the country produced a ¥643 billion surplus, but last month, higher energy prices caused the nation to curtail its imports of oil and natural gas by 50%. The drop in energy commodities shipped into the country resulted in imports climbing only 9.7% y/y while exports grew 14.8%. Growing demand from foreign markets for AI technology accounting for most of the increase in items sent abroad. During the month, the value of computer chips sent to foreign markets climbed 44%.

Japan’s S&P Global Flash Japan Composite sank 1.10 points to 51 this month with the services industry nearly falling into contraction. The composite result was the lowest print since May. The services PMI descended from 51 to 50, which is the expansion/contraction threshold.

Manufacturing stayed solidly in expansion territory with the 54.5 result matching the economist consensus estimate despite weakening from 55.1 in April. Services, however, fell from 51 to 50, which is the expansion/contraction threshold. For the composite index, price pressure was intense across the country with the Midde East war disrupting supply chains. Businesses jacked up their gate prices at the sharpest pace in 19 years, but the change was less dramatic than the increase in input costs.

Factory output inflation in South Korea climbed 6.9% y/y and 2.5% m/m during April, according to the Producer Price Index. The ascents follow March’s 4.1% and 1.7% jumps. April was the eighth consecutive month of pressures intensifying with higher energy costs pushing up charges.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!