- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 16, 2025 at 12:56 pm

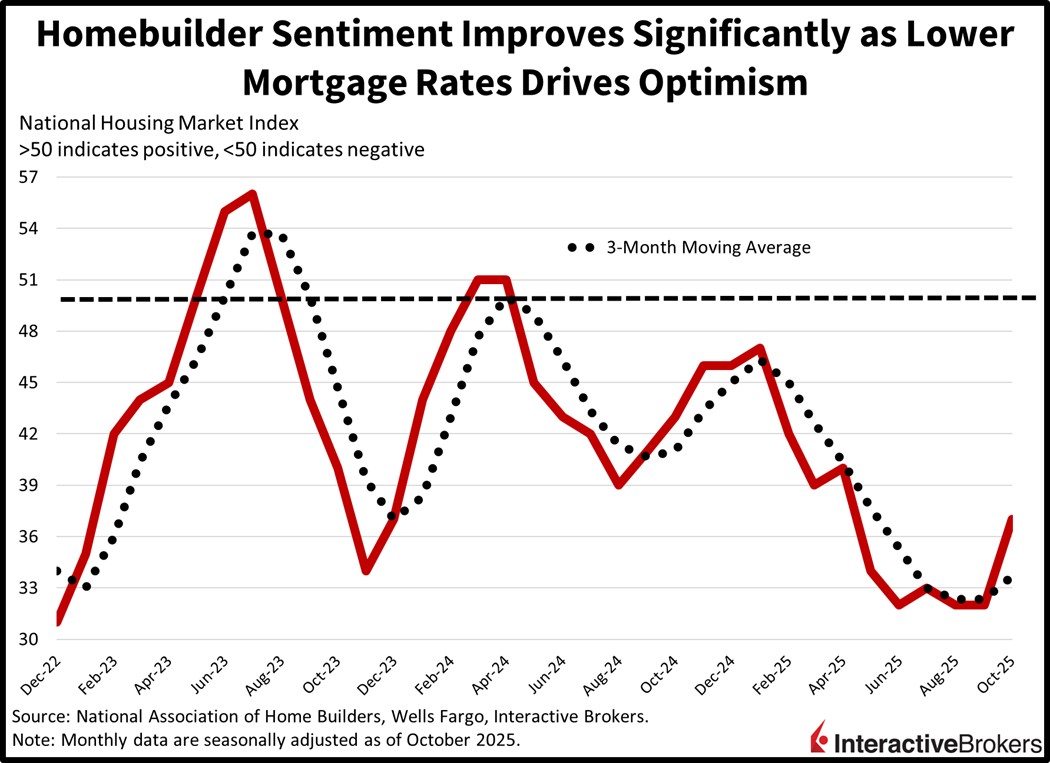

Market choppiness is continuing on Wall Street today as investors balance concerns about US-China trade tensions with satisfaction stemming from robust corporate earnings and the progression of AI. Participants are indeed considering the potential that cross-border commerce quarrels with Beijing could weigh on growth, but quarterly calls reporting buoyant profitability are hampering worries and supporting optimism. And it’s not only asset managers that were feeling generally upbeat before the afternoon selloff, as this morning’s homebuilder sentiment figure jumped to a six-month high thanks to lighter mortgage rates improving both affordability and prospective buyer traffic while bolstering the outlook for the industry. The NAHB/Wells Fargo print, on the 16th day of the government shutdown, adds to the growing list of evidence that the bottom is in for the real estate sector. Meanwhile, traders are indecisive again against the backdrop of turbulence in stocks. The strong climb following the opening bell has since reversed sharply, even as equity bulls were fighting to keep the gains alive, as they grappled with the bears at the flatline of the S&P 500 in NFL endzone fashion but failed to prevent a touchdown. Equities are retreating heavily at this juncture. In fixed-income, Treasuries are gaining, led by the short-end, as Fed Governors Waller and Miran have just claimed that imminent rate cuts are needed, although the former speaker prefers a cautious walk down the central bank’s stairs while the latter wants to jump lower, favoring a half-point reduction. Elsewhere, the greenback is flat, volatility protection instrument prices are higher on greater hedging demand, forecast contracts are catching bids and the commodity complex ex crude oil is rising, with gold notching another fresh record near level of $4,300. Conversely, Bitcoin remains in a malaise and is suffering losses; it’s now approximately 14% below its peak as it navigates correction territory.

Homebuilder sentiment hit a five-month high in October, leaping the most since January 2024 as lighter mortgage rates improved the number of potential purchasers, current conditions and the outlook for the sector. The National Association of Home Builders (NAHB) and Wells Fargo headline figure of 37 exceeded both the median estimate of 33 and the prior period’s 32. The index’s transactions in the present, prospective buyer traffic and closings in the next six months all posted gains, rising from 34, 21 and 45 to 38, 25 and 54. Furthermore, no regional declines existed, with the Northeast, South and West strengthening from 44, 29 and 26 to 46, 31 and 28. The Midwest was unchanged at 42, meanwhile.

The common pattern during the past few days of equities moving from green to red is increasing the possibility of near-term weakness in stocks, because it points to a lack of conviction amongst shareholders and potential buyers. But these dips are buyable, in my view, as the economic fundamentals supporting risk assets are supportive. Against this backdrop, however, I’m expecting that incoming monetary policy accommodation is going to support the more cyclically-oriented, rate-sensitive, aspects of the market and broaden the participation across sectors. Lower costs of capital would also help justify valuations of some of the frothier components, effectively raising the ceiling and permitting a further runway.

The UK’s gross domestic product expanded 0.1% month over month (m/m) and 1.3% year over year (y/y) in August. Both metrics met the economist consensus estimate after recording a 0.1% m/m drop and a 1.5% y/y gain in the preceding month. Among broad categories, industrial production grew 0.4% m/m after sinking by the same amount in July. Economists expected a 0.2% advancement. Relative to August 2024, out was lower by 0.7%, a more significant contraction than the 0.1% y/y fall in July and worse than the 0.6% descent anticipated by economists. Manufacturing, electricity, gas, steam and air conditioning were the largest contributors to the m/m positive change. Within manufacturing, a 4.8% gain in computer, electronic and optical products offset weak showings for chemicals, pharmaceuticals and various non-metal items, such as rubber and plastic. Conversely, construction in August fell 0.3% m/m but was up 1% y/y after recording no monthly change and a 1.8% gain in July.

The UK’s importing activity in August was roughly unchanged relative from July, but a 3.3% decline in goods exports contributed to country’s trade deficit expanding from £3.02 billion in July to £3.39 billion in August. On a positive note, increased demand for services from foreign customers helped dampen the export decline. The US trimmed its purchases of goods and services from £5.2 billion in July to £4.5 billion in August. Exports to other countries also slipped.

A jump in the number of individuals entering the job market caused Australia’s unemployment rate to climb from 4.3% in August to 4.5% last month, the highest print since November 2021. Economists estimated that the rate would remain unchanged. The nearly four-year peak occurred despite payrolls expanding by 14.9k, which missed the economist consensus estimate for 20.5k additions but nevertheless was a significant reversal from the 11.8k decline in August. Within the group of new employed workers, 8.7k are full-time. In August, the country’s payrolls lost 48.6k full-time positions. The loftier unemployment rate is attributable to more individuals entering the workforce, with the country’s labor participation rate climbing from 66.9% in August to 67%, slightly higher than the economist consensus forecast of 66.8. In a related matter, the number of hours worked increased by 0.5% last month.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!