- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 9, 2026 at 2:20 pm

Wall Street was taking a breather from an extended stretch of gains on mounting doubts concerning the US-Iran ceasefire until equity and fixed income assets pulled an intense, bullish, intraday reversal after Israel agreed to negotiate with Lebanon. It was precisely the hostilities between those two nations that raised concerns about the durability of the deal. Additionally, the Strait of Hormuz remains inaccessible to most vessels and as result, American troops are staying in the region on President Trump’s orders. The dramatic shift in events has investors enjoying the seventh consecutive day of progress for stocks and economic data has been supportive too, as continuing unemployment claims fell to almost a two-year low while initial filings arrived generally in-line, strengthening confidence that labor conditions, which underpin the cycle, are stable. PCE inflation numbers were elevated as expected, but they failed to move the needle much as those statistics are stale from February. Besides, market participants are growing accustomed to managing lofty price pressure figures and heavy interest rates, although tomorrow’s March CPI will offer a substantial test for the bulls. Meanwhile, yields joined the U-turn and are now dropping relatively evenly across the curve and bringing the greenback south with them. All major equity benchmarks are advancing amidst robust sector breadth alongside the overall commodity complex. Elsewhere, cryptocurrencies are joining the party while prediction markets catch bids.

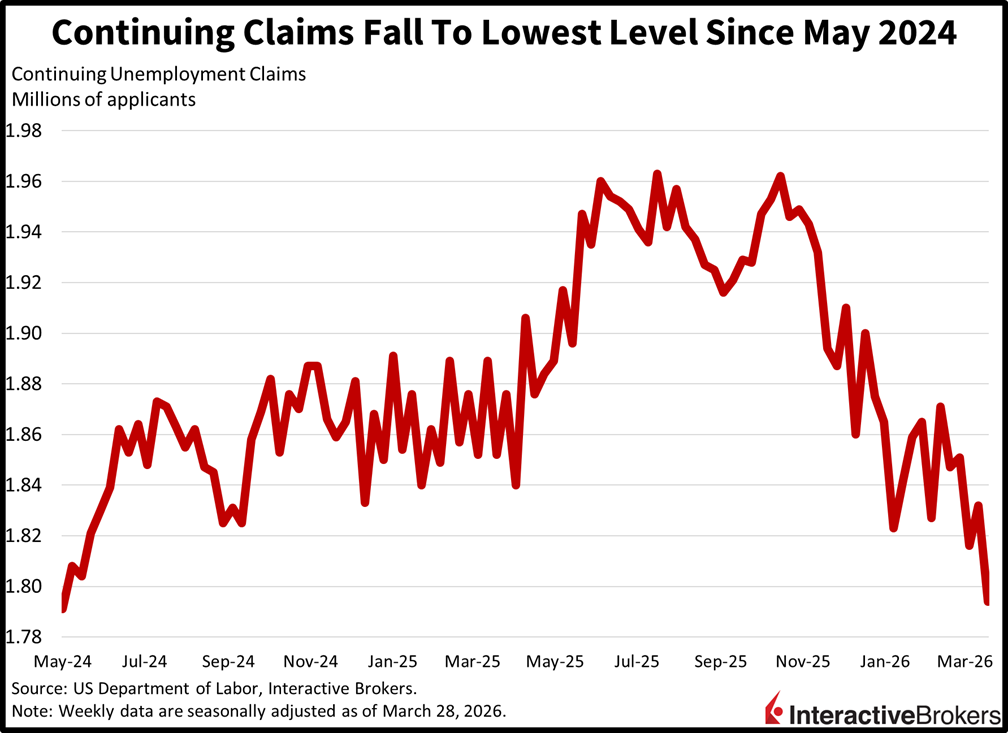

Claims Signal Labor Market Stability

Continuing unemployment claims fell to their lowest point since May 2024, as the labor market continues to reflect stability in light of elevated economic risks. The 1.794 million reported for the week ended March 28 was well below the median estimate of 1.840 million and the prior print’s 1.832 million. Initial applications for the following seven-day period, meanwhile, rose to 219k, arriving above the expected 210k and the previous interval’s 203k. Despite the increase, layoffs remain subdued by historical standards. Four-week moving average signaled sturdy workforce counts, with the 209.5k and 1.823 million figures remaining in the safe zone.

Tomorrow’s CPI Could Disrupt the Rebound

Despite the reprieve in crude today, which traded from a high of $102.70 per barrel to a low of $95.25, the critical commodity remains 64% higher than it was 12 months ago. For precisely this reason, the upcoming Consumer Price Index is almost certainly going to exceed 3% for the first time since May 2024, and if oil doesn’t drop beneath $80 soon, the indicator will carry a four-handle by this summer. Meanwhile, heading into this year, a substantial part of the bullish narrative included subdued energy costs and interest rate cuts, but those conditions are significantly unlikely to occur due to impaired production facilities, a lack of clarity concerning the Middle East conflict and uncertainty regarding reduced trade flows through the Strait of Hormuz. The deteriorating supply outlook alongside accelerating cost forces makes it incredibly difficult to envision WTI below $70 or the next move from the Fed being a reduction. Tomorrow’s CPI could certainly disrupt the ferocious market rebound we’ve experienced with equities bouncing more than 8% in 10 calendar days from the lows on March 30; however, fiscal stimulus, stable employment and rising corporate earnings estimates serve as offsetting factors for the bulls.

International Roundup

Japan Household Confidence Falls Below Expectation

Japan’s Household Confidence gauge last month plunged from 39.7 in February to 33.3, significantly underperforming the 38.3 forecast from a consensus of economists. The decline—the largest since the Covid-19 panic—points to consumer concerns regarding the Middle East crisis with Japan heavily reliant on oil imports. According to the country’s Cabinet Office, sentiment weakened across the gauge’s categories as follows:

In other areas, the percentage of survey respondents expecting prices to go up climbed 7.5 percentage points to 93.1%. The portion of respondents that anticipate stable prices, furthermore, fell from 6.1% to 2.7%. When asked if prices will decline, only 2.5% said yes compared to 6.1% in February.

But Machine Tool Orders Jump

Orders for machine tools were 28.1% higher in February than in the year-ago period, according to preliminary data from the Japan Machine Tool Builders’ Association. The print reflects an acceleration following January’s 24.2% year-over-year growth.

UK Household Loan Defaults Increase Modestly

Defaults on unsecured lending increased during the first quarter and are expected to increase in the subsequent three-month period with the outlook weighed down by expectations for credit card problems, according to the Bank of England’s quarterly survey of credit conditions. Defaults on secured loans to households also increased but to a much lower extent. In the corporate sector, demand for lending from small and large businesses grew but was flat in the mid-size segment.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!