- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 27, 2026 at 1:01 pm

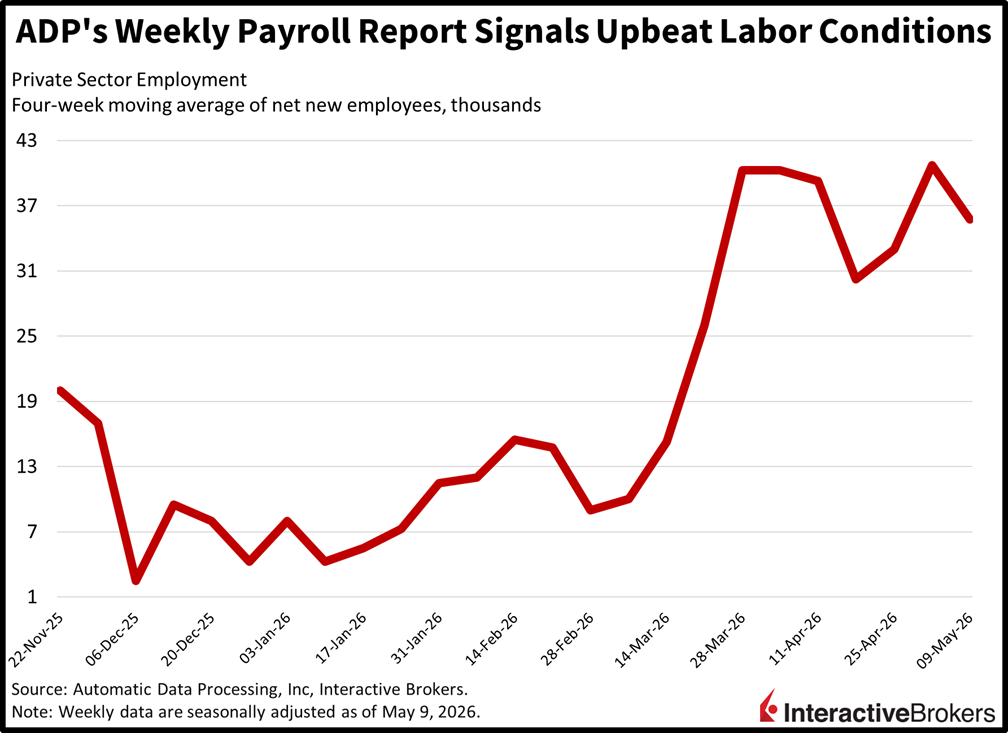

Geopolitical relief is continuing to bolster markets today as Tehran communicated that an agreement with Washington would normalize traffic across the Strait of Hormuz in a month. The Iranian statement is strengthening confidence on Wall Street that a deal could be around the corner and crude oil is plunging as a result, sending yields and the greenback further south along with it. The welcome news has stocks looking to close green for the fifth consecutive day as well as for the ninth week in a row as investors are gravitating to cyclical-oriented, rate-delicate equities this session with the Dow Jones and Russell 2000 reaching fresh records while outperforming. Additionally, healthy ADP-weekly jobs numbers underpinned the positive employment outlook while dismissing worries of softening labor conditions, propelling the consumer discretionary and staples categories to drive the train as it leads the other segments. The Nasdaq 100 touched an all-time high too in the very first minute following the opening bell, but it’s now retreating as participants take a break from fiery hot AI tech trades to pull the economically sensitive levers. Against this backdrop, 6 of the 11 major sectors are appreciating as sinking borrowing costs and fuel charges could spark a broadening within the benchmarks. Elsewhere, commodities and cryptocurrencies are lower, volatility protection instruments are flat and prediction markets are catching bids.

Private-sector hiring remained upbeat as employment growth decelerated only slightly from the fastest pace of payroll expansion this year. Indeed, employee headcounts increased by an average of 35.75k employees in each of the four weeks during the period that ended May 9, slower than the 40.75k figure from the prior print, according to ADP. Despite the modest softening, this morning’s report depicts payrolls rising at a rate of roughly 155k per month, which is consistent with cyclical strength and ongoing consumer spending capacity.

If the high-power AI trade is tired, cyclicals could potentially provide opportunities for investors seeking equities that can catch up to tech. It’s precisely the cyclical segments of the market that would benefit disproportionately from a US-Iran peace deal, as they’re increasingly levered to the consumer, rates, oil prices and the economy. A broadening rally would additionally be healthy in the longer run, because it would reduce heavy concentrations in the major stock benchmarks while widening the margin for error across individual companies. Furthermore, today’s significant outperformance from the Dow Jones Industrial Average could signal that the gains could begin expanding more materially to the non-tech sectors.

China’s strength in electronics manufacturing and the energy shock from the US-Iran war helped the country’s industrial sector post a 24.7% gain in profits despite production of consumer items falling as a result of households’ diminished spending power. April’s print was the strongest acceleration since late 2023 and follows the 15.8% y/y climb in March. For the first four months of 2026, industrial earnings were up 18.2% year over year (y/y), a stronger showing than the 15.5% y/y jump in the first quarter.

Earnings jumped in the computing and electronic equipment category. The oil and gas extraction category, the petroleum processing industry and mining also posted strong growth.

Services prices that businesses charge each other in Japan were up 3% y/y in April, according to the Corporate Services Prices Price Index (CSPI). While the rate points to businesses potentially passing higher labor wages on to customers, it was pushed upward by higher international shipping costs and it was cooler than the economist consensus estimate of 3.3%, which was also the March rate. When excluding transportation, the CSPI was up 2.5% y/y, a deceleration from 2.9% in March. After climbing 44.6% y/y in March, ocean freight transportation was 59.1% more costly last month when compared to the year-ago period, which pushed the broader transportation and postal activities category up 5.1%. International air freight, with a 40.6% y/y climb, also contributed to the overall category’s increase. The leasing and rental category also climbed, posting a 5.3% y/y increase, a result of leasing costs jumping 7.7%. Also in today’s print, a 9.5% gain in access charges pushed the information and communications category up 2.7%.

Australia’s Consumer Price Index (CPI) was up 4.2% y/y in April after climbing 4.6% in the preceding month. The gauge also depicted prices falling 0.1% m/m. Relative to the year-ago period, stickers for transport, housing, clothing and footwear, education and the food and non-alcoholic beverages groups were up 6.6%, 6.3%, 5.9%, 4.8% and 2.8%.

The value of completed construction in Australia rose 3.4% quarter over quarter (q/q) during the first three months of 2026, exceeding the consensus estimate for a slower 0.8% northward change, according to the Australian Bureau of Statistics. In the last quarter of 2025, construction was up only 0.2% q/q. Despite the stronger than anticipated report, residential construction dropped 0.6%. Non-residential work bucked the trend, climbing 2.5% while engineering was up 6.9%.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!