- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 6, 2026 at 12:58 pm

A morning surge in stocks that propelled the S&P 500 close to touching fresh records was tempered about an hour after the opening bell as sellers came in and blocked the advance. But the Dow Jones Industrial Average marked a new peak in concentrated fashion, as a 4% climb in Amazon shares bolstered the benchmark. Overall, though, worries that geopolitical tensions could ignite volatility and trigger a reversal in equity appreciation motivated some investors to take some profits with equities near all-time highs in the other indices. Meanwhile, rising interest rates were another headwind, with Treasuries surrendering yesterday’s progress that was driven by a weaker-than-expected ISM-manufacturing print and lighter inflation expectations. Furthermore, an outlook of softening cost pressures is being supported by lessening probability of an energy price spike following US military operations in Caracas. With Washington exerting a heavy amount of influence in the oil-rich nation, the chances of scarce supplies have dropped meaningfully. Jumping yields are generating gains for the greenback on a day featuring a lack of economic data. In commodities, precious metals are surging, with silver and gold up 5.8% and 1% on safe-haven demand. Copper, furthermore, is up 1.3% on projections of limited available quantities, while crude oil, natural gas and lumber descend. Elsewhere, forecast contracts and Ethereum are catching bids even as Bitcoin takes losses.

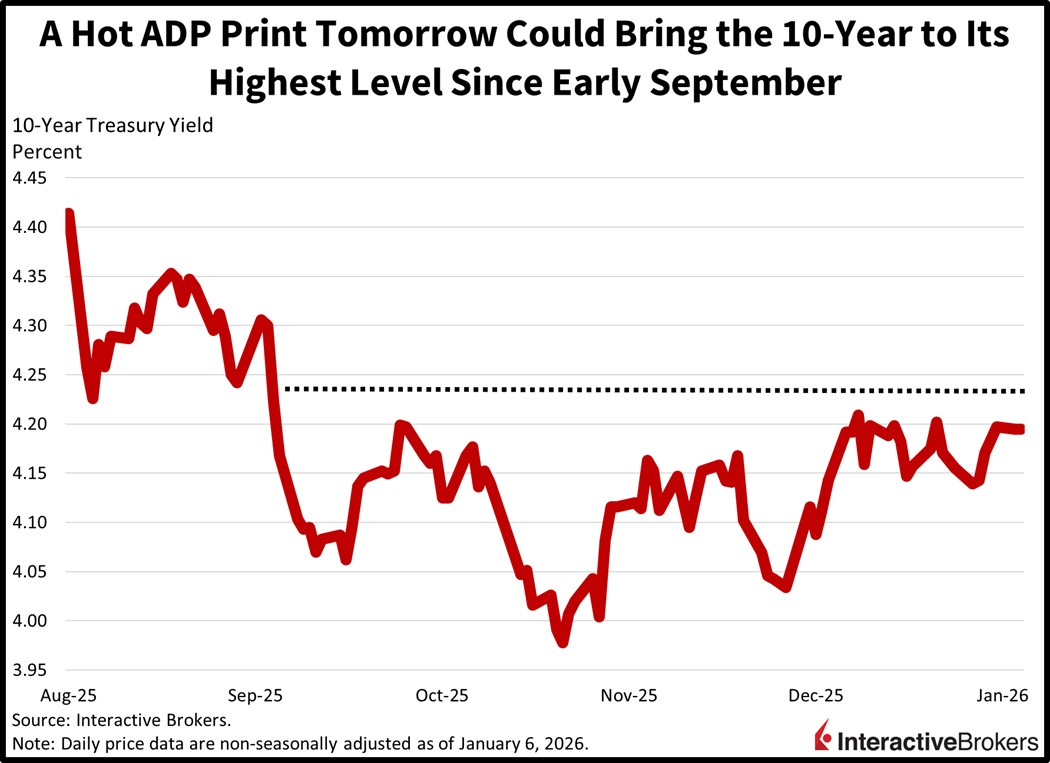

Investors are welcoming incoming economic data to justify positioning into 2026 and we have an eventful schedule tomorrow. The most impactful publication will be ADP’s monthly jobs report, as an uptick in unemployment is one of the significant risks in this new year alongside of heavy investments in AI potentially failing to deliver blockbuster returns. Participants will also closely watch job openings and ISM-services for additional labor market information as well details concerning the momentum of consumer demand. Fixed income and equity assets are likely to benefit from healthy numbers that are near expectations but not too strong, because the 10-year is on the brink of rising to its highest level since early September. Ultimately, I’m a Treasury bull at this juncture, considering fiscal improvements and softening inflation that together should counter a reacceleration in growth and bring duration about 25 basis points lower from current levels. Still, big beats beat on ADP and JOLTS could drive 10s to 4.25% and 30s to 4.90% while weighing on Fed easing enthusiasm. Meaningful misses, meanwhile, could raise slowdown concerns and weaken stock buying as traders opt for government debt instruments instead.

Business activity in Singapore slowed in December with the S&P Global PMI falling from 55.4 to 54.1 but stayed significantly above the contraction-expansion threshold of 50. The December reading was the lowest in four months. Nevertheless, it was the eleventh consecutive month of strengthening business conditions.

Growth of both new orders and output weakened slightly, and firms focused more on backlogs as a result. A slightly smaller workforce resulting from resignations and fewer part-time employees also contributed to reduced production. Input prices continued to rise due to higher expenses for materials, operations and labor, but the pressure softened slightly. Companies responded by increasing their gate prices, which helped support margins. In another matter, confidence improved with businesses feeling optimistic about new product launches, higher output and growth plans.

Hong Kong businesses reported a fifth consecutive month of improving conditions during December, but the pace of the rise in activity slowed, according to the S&P Global Hong Kong SAR PMI. The gauge fell from 52.9 in November to 51.9 last month. It was the fifth month of strengthening conditions as sales expanded at roughly the same pace as in recent months with loftier confidence among buyers supporting the trend. In this regard, revenues were supported by stronger orders from mainland China and other international markets. The ongoing strength contributed to growing work backlogs and larger volumes of input purchases, albeit at a slightly slower rate than during November. December was the first time backlogs expanded in 2025. Input costs, however, picked up with higher raw material costs and separately, labor outlays climbed at the fastest rate since June 2024. Businesses were able to pass the costs onto customers in the form of higher gate prices. Firms ended the year with lingering concerns about the global economy and the impacts of tariffs, but the degree of negative sentiment was the weakest in roughly 30 months.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

U.S. Spot Gold trading through IB LLC accounts is only available to legal residents of the United States that do not reside in Arizona, Montana, New Hampshire, and Rhode Island.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!