- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 9, 2026 at 11:15 am

Global agriculture is running into a cost problem that is coming from multiple directions at once. Input prices are rising. Trade flows are becoming less efficient. Energy costs are feeding directly into production decisions. The unfortunate result is a global system that still produces, but with thinner margins, more sensitivity to shocks, and added strain to the farmers and consumers alike.

Farm-level inflation is broad, persistent, and hard to offset. Farmers are seeing higher costs across:

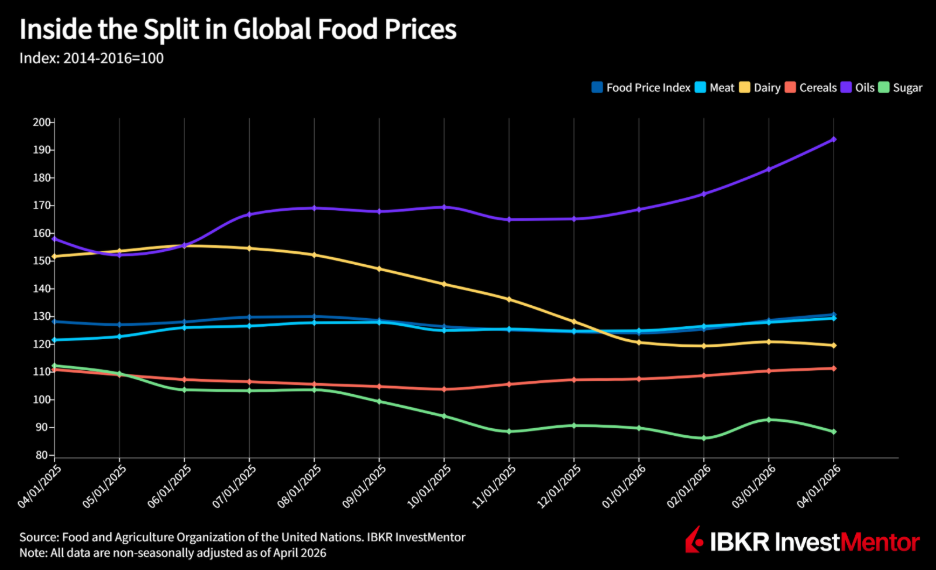

The FAO Food Price Index averaged 130.7 in April 2026, up 1.6% from March and marking the third straight monthly increase. That level is well below the 2022 peak above 160, when the Russia-Ukraine shock pushed markets to extremes. But it is still materially above the pre-2020 range of 90–100, when global food markets were relatively stable.

Fertilizer prices highlight the trend:

When input prices rise faster than crop prices, margins tighten. That leads to slower investment and more cautious production decisions.

Agriculture depends on global trade channels that balance production and demand across regions. Tariffs tend to disrupt that balance. The most recent data suggests that trade has continued, but with a lot more friction:

As I discussed in my piece about US CPI, energy prices are surging. This adds more strain as it’s used a lot in modern agriculture. Fuel powers equipment and transport. Natural gas is critical for fertilizer production, accounting for 70% to 90% of ammonia costs.

Recent moves in energy markets have fed directly into agriculture:

Albeit, fuel is a relatively small share of total farm costs, but it moves quickly when prices shift. A 30% jump in diesel can still push overall production costs higher, especially once transportation and field operations are factored in.

The bigger impact runs through fertilizer. Its cost is closely tied to natural gas, so when energy prices rise, fertilizer becomes more expensive. Farmers often respond by scaling back usage or switching crops, which can lower yields in later growing cycles and tighten supply.

The effects of these pressures do not stay on the farm, like everything else; they move through the supply chain and show up at the checkout counter. Higher input costs lead to higher production costs. Less efficient trade raises transportation and sourcing costs. Energy prices add pressure at every step, from planting to packaging.

That combination feeds directly into food prices:

This is where it starts to show up for consumers:

There is also a lag effect. When farmers reduce fertilizer use or shift planting decisions today, the impact shows up in the following years harvest in the form of tighter supply. That can keep prices elevated even if demand remains stable. For lower-income households, where food takes up a larger share of spending, these cost increases are cutting deeper and stretching already thin budgets.

To learn more about commodities, download the IBKR InvestMentor app.

Learn more about InvestMentor

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR InvestMentor, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR InvestMentor and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

IBKR InvestMentorSM is a service of Interactive Academy LLC, an affiliate of IB LLC and majority-owned by IBG LLC. All content provided by IBKR InvestMentorSM is for informational and educational purposes only and should not be interpreted as implying any sponsorship, partnership, endorsement, recommendation, or approval by IB LLC or its affiliates.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

No mention of climate change bringing more extreme weather — flooding, droughts, etc. — reducing crop yields. Or rising temperatures increasing the threat of marginally productive land turning into deserts in dry areas. This megatrend is a growing threat to the world’s food supply, and there’s no sign it will reverse any time soon.

No mention of climate change causing more extreme weather, such as floods and drought? Or the increased risk of marginally productive land in dry areas turning into deserts? This megatrend is a growing threat to the world’s food supply, and the prospects aren’t great for it to reverse any time soon.