- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 15, 2026 at 12:00 pm

Agricultural commodity markets are experiencing a significant re-rating in 2026. The Bloomberg Commodity Agriculture Index has returned 13.4% Year to Date1, driven by a confluence of supply side shocks – a rising probability of an El Niño event disrupting growing conditions across three continents and the Iran war’s disruption to shipping through the Strait of Hormuz. These forces are not independent; they interact and reinforce each other and together they are reshaping the near term supply outlook across the agricultural commodity complex.

Agricultural commodities can be highly volatile and may be affected by weather events, geopolitical developments, currency movements, regulatory changes and fluctuations in global demand. Commodity ETCs may experience significant price swings and investors may lose some or all of their investment.

The Strait of Hormuz: A Key Chokepoint for Fertilizer Trade

Discussion of the Strait of Hormuz typically centres on oil. Less well understood is its parallel role in global fertilizer supply. The Persian Gulf nations — Iran, Qatar, Saudi Arabia, and the UAE — collectively represent one of the largest regional exporter of nitrogen fertilizers globally, a position reinforced after Russia’s partial exit from normal trading channels following 2022. The Strait is the sole maritime exit for all of them. The scale of fertilizer exposure through the Strait is material:

Transmission to Agricultural Commodity Markets

The Food Agricultural Organisation (FAO) has confirmed a developing fertilizer shortage across Asia and the Global South, with India, Bangladesh, Egypt, Sudan, and parts of Sub-Saharan Africa among the most affected regions. The key analytical point is the lag between the disruption and its harvest impact. Shipping delays from the Gulf to the Indian subcontinent run approximately 30 days, meaning supply shortfalls in March affected April and May planting windows, with the full harvest consequences not expected to become visible in production data until Q3–Q4 2026.

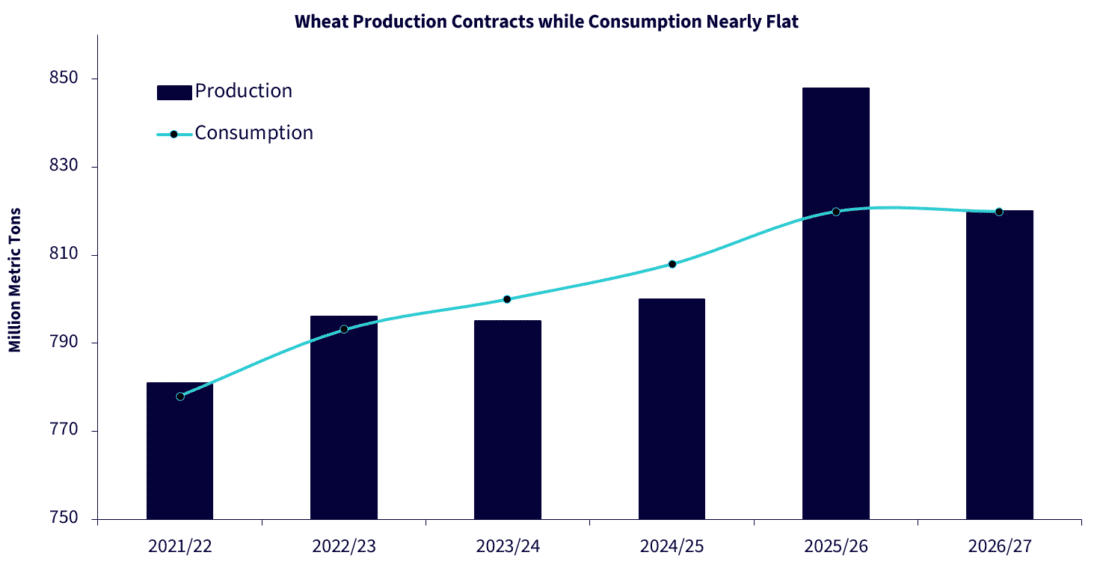

Figure 1:

Source: USDA Grain: World Markets and Trade report as of May 2026.

Figure 2:

Source: USDA Oilseeds: World Markets and Trade report as of May 2026.

Super El Niño: Compounding the Fertilizer Supply Picture

An El Niño event is widely expected to develop during mid-2026. An El Niño weather event is triggered by a warming of a region in the Pacific Ocean, which drives a change in trade wind patterns around the world. Some places become hotter than normal. Other places become cooler than normal. Some places become wetter than normal, while others become drier. The key issue is that a weather deviation from normal has the potential to adversely affect crop yields. The World Meteorological Organisation’s (WMO) April 2026 Global Seasonal Climate Update signals rapidly rising sea-surface temperatures in the Equatorial Pacific, with National Oceanic and Atmospheric Administration’s (NOAA) Climate Prediction Centre assigning a 82% probability to El Niño onset during May–July 2026 (vs 61% probability in their April report). Its significance in the current context is that it has the potential to reduce agricultural crop yields in the same producing regions that would otherwise have helped offset the input cost pressures arising from the Hormuz disruption. Both forces are pulling in the same direction at the same time.

What matters more is the timing and the baseline from which this event is developing. 2025 was cooler than 2024 due to a La Nina phase, despite being one of the warmest years on record overall. That La Niña induced cooling was always temporary. 2024 was the hottest year on record9 with global average surface temperatures 1.55 degrees above the 1850-1900 average, characterised by exceptional land and sea surface temperatures and ocean heat. Agricultural systems are already operating under stress from that elevated baseline and the return of El Niño layered on top of it compounds the risk materially.

Critically, the weather effects of El Niño tend to peak during December, but the impact typically takes time to spread across the globe. Much of the agricultural damage from an event that peaks in the northern hemisphere winter manifests in the following growing season, meaning stress that is already appearing in agricultural systems today is likely to intensify before it eases. Historical data shows there is typically a 6–12-month lag between the peak of an El Niño event and the peak of the production impact. Historically, agricultural commodity markets have often repriced ahead of confirmed production impacts, as markets tend to react in anticipation of tightening supply conditions.

Historically, soft commodities have often shown heightened sensitivity. Soft commodities have consistently been the strongest performers during El Niño episodes, three of the five soft commodities (cotton, coffee, and sugar) moved to multi-year highs in 2022–23, and in late 2024 orange juice and cocoa reached record highs while coffee reached a record high in 202510. Every strong El Niño in the past 55 years has reduced global cocoa production, with Ecuador and Indonesia the most exposed origins and significant risks in West Africa (where most of the world’s production is now concentrated).

Conclusion

The agricultural commodity complex in 2026 is being shaped by two supply-side forces that are unusual both in their scale and in the way they interact. The Hormuz fertilizer disruption is affecting input costs and planting decisions in real time, with consequences that will continue to emerge in harvest data through Q3–Q4 2026 and into 2027. The developing El Niño is adding a climate layer on top of a temperature baseline that is structurally higher than any previous episode — and its production impact, when it arrives, will follow with a 6–12-month lag from peak.

—

Originally Posted May 15, 2026 – Two Shocks, One Direction: The Case for Agricultural Commodities in 2026

1Bloomberg Finance L.P. from 31 December 2025 to 13 May 2026

2Bloomberg Finance L.P. from 31 December 2025 to 13 May 2026

3CRU as of 15 March 2026

4Argus Media as of 31 March 2026

5Energy Information Administration, June 2025

6United States Department of Agriculture (USDA) May World Agriculture Supply and Demand Estimates (WASDE) Report as of 12 May 2026

7United Stated Department of Agriculture as of May 2026

8Bloomberg Finance L.P. from 31 December 2025 to 13 May 2026

9World Meteorological Organization (WMO)

10Bloomberg Finance L.P. as of 31 March 2024

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Exchange Traded Commodities (ETCs) are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong and IBKR Singapore entities.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!