- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 12, 2024 at 11:00 am

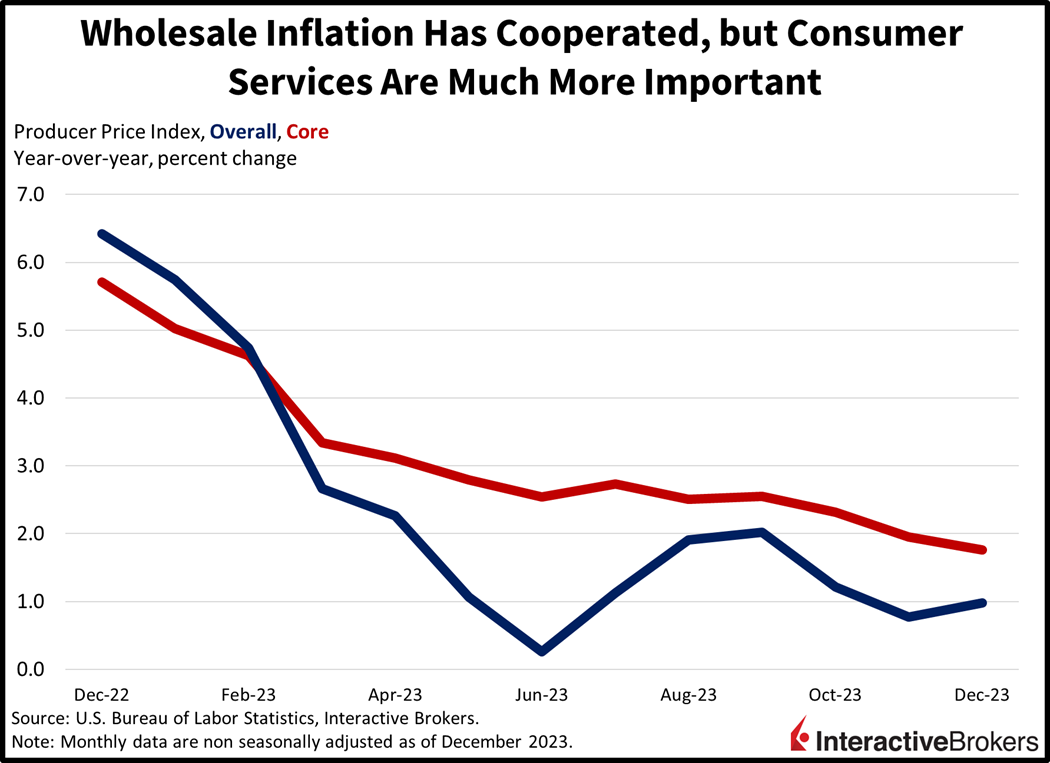

In yet another example of investors becoming increasingly choosy at the data buffet restaurant, players are ignoring yesterday’s hotter-than-expected Consumer Price Index in favor of this morning’s lighter-than-expected Producer Price Index. The problem is that the PPI is much more sensitive to goods and commodities, while the CPI weighs services and labor market dynamics much more heavily. Indeed, the US economy is services oriented and labor intensive, making the CPI a much more useful indicator of inflation trends. Similar to last week’s emphasis on ISM-Services employment while disregarding Job Openings, Unemployment Claims, ADP Jobs and BLS Jobs, the marketplace is placing their focus on yet another data point that supports a rate cut while ignoring a more significant one that bolsters a rate hold.

Wholesale prices experienced relief last month on the back of lighter manufacturing demand. The PPI fell 0.1% month-over-month (m/m) while rising 1% year-over-year (y/y), lighter than projections calling for increases of 0.1% and 1.3% and near November’s -0.1% and 0.8%. The core PPI, which excludes food and energy, was unchanged m/m while rising 1.8% y/y, less than expectations of 0.2% and 1.9% and close to the previous month’s 0% and 2%. Price relief was driven primarily by goods, whose prices dropped 0.4% m/m while services prices were unchanged. Prices for energy, foods, trade services, and transportation and warehousing services dropped 1.2%, 0.9%, 0.8% and 0.4% m/m, respectively. The other services category did increase 0.4% during the month, however, driven by a 3.3% m/m increase in prices for securities brokerage, dealing, and investment advice.

Congress is under considerable pressure as the looming threat of a government shutdown rapidly approaches. Speaker Mike Johnson might have to scratch his own bipartisan deal, as he’s under pressure from House budget hawks that don’t like it, adding to the uncertainty surrounding the path lawmakers will take to ensure government funding. The approaching January 19 deadline adds urgency to the situation, making it crucial for a resolution to be reached swiftly.

The US and the UK initiated attacks on Yemen in retaliation to maritime incidents in the Red Sea. The international community’s responses to the strikes on Houthi facilities in Yemen have varied, with Oman in the Middle East expressing disagreement, stating that the actions went against its advice. WTI crude oil was up 3% earlier but has pared most of its sharper gains on concerns of a wider economic slowdown and is now only up 0.3%, or $0.21, to $72.98 per barrel.

Special charges associated with the regional banking debacle have dinged earnings for some of the nation’s largest financial institutions, according to quarterly reports released this morning. At the same time, JPMorgan’s top executive has warned of a potentially challenging economy in the coming months. Highlight from the reports include the following:

Markets are mixed today with a light PPI report supporting optimism for a Fed rate cut and offsetting cautious earnings commentary from the banks amidst continued escalation in the Middle East conflict. Equities are generally lower while bond yields are shifting in bull-steepening fashion. For equities, the cyclically tilted Dow Jones Industrial and Russell 2000 indices are down 0.5% and 0.1%, respectively, while the Nasdaq Composite and S&P 500 are up 0.1% each. Sectoral breadth is split with communication services (+0.7%) and energy (+0.5%) leading the gainers while consumer discretionary (-0.8%) and health care (-0.4%) decline the most. In fixed-income land, the 2- and 10-year Treasuries are experiencing yield declines of 10 and 1 basis points (bps) as the instruments trade at 4.15% and 3.95%. The dollar is roughly unchanged with the US currency gaining against the yuan, pound sterling, and euro while declining relative to the franc, yen and Aussie and Canadian dollars.

With cyclicals and technology shares near all-time highs, earnings reports next week are likely to significantly impact investor sentiment. Today’s commentary from the banks intensified fears of a global economic slowdown, while the manufacturing sensitive PPI came in significantly below expectations. Furthermore, the sharp bull-steepening across the yield curve is narrowing the gap between the 2- and 10-year Treasury maturities, a pattern that is worrisome if it continues. The rapid de-inversion of the yield curve often precedes risk-off shifts in markets. The spread between the two instruments was as low as 108 bps in July, but it has increased to a mere 20 bps and may be signaling economic volatility ahead.

Visit Traders’ Academy to Learn More About the Producer Price Index and Other Economic Indicators.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

")

What does “de-inversion of the yield curve” mean? Thanks.

Hello, we appreciate your question. The 2-10 Treasury curve effectively becomes uninverted when yields on the instruments approach the same levels. That would require the 2-year yield to drop to where the 10-year is or the 10-year to rise to where the 2-year is. The former motion would be a bull-steepener while the latter would be a bear-steepener. We hope this helps!

I learn things here. Thank you.

We hope you continue to enjoy IBKR Campus!