- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 30, 2025 at 1:07 pm

Yesterday afternoon featured a much-anticipated White House meeting between Congressional leaders and the President that was intended to avert a government shutdown. When Vice President Vance emerged saying, “I think we’re headed to a shutdown,” that seemed to have sealed the negotiations’ fate. As I type this, there are still more than 12 hours remaining before one occurs, but with the “US Government Shutdown” contract on IBKR ForecastTrader showing a roughly 90% probability of a shutdown, it seems increasingly inevitable. Yet investors don’t seem to mind. Should they?

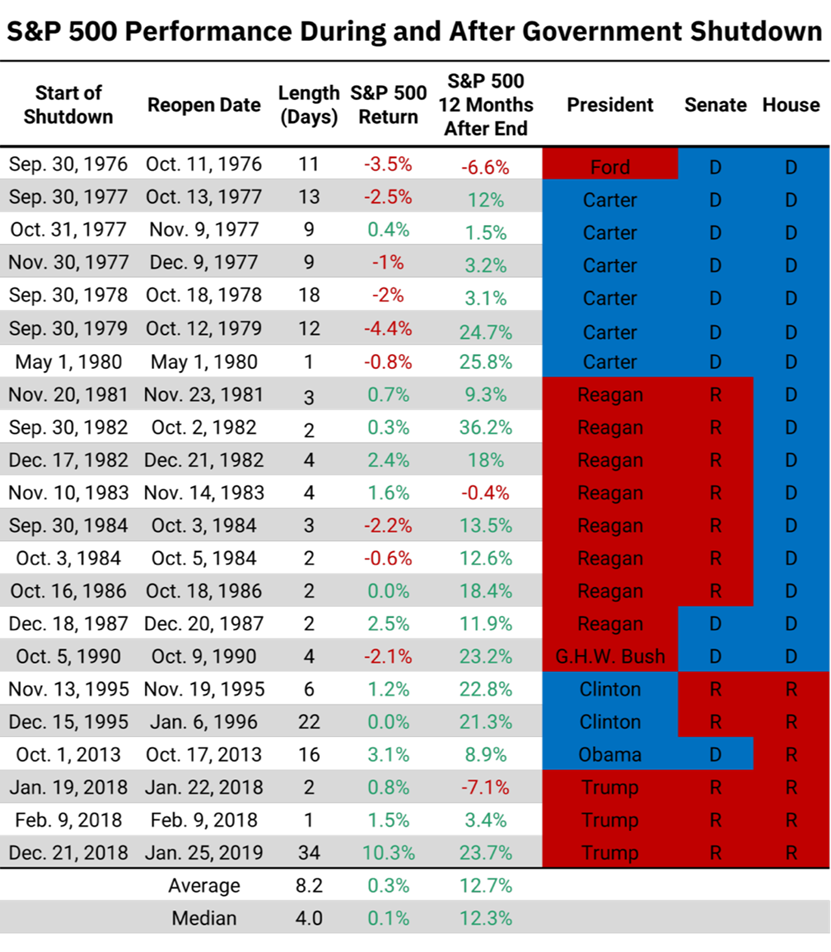

The short answer is not really, at least not for now. While it is difficult to spin a shutdown as a positive, it is not an obvious negative – at least for now. Shutdowns tend to be short-lived and ultimately don’t lead to much lasting damage to the economy or specific companies. They occur regardless of who controls the Presidency, the Senate or the House, and history shows that they neither offer much of an impact to stocks in either the short- or long-term. I offer the following chart, courtesy of my friend Steve Wyett at BOK Financial:

Source: BOK Financial

Over the past 40 years, we’ve had 22 shutdowns, though the bulk of them occurred during the Carter and Reagan administrations. The average length of a shutdown is 8.2 days, with a median of 4 days. That is not enough time to significantly impair an economy or market. We also see that both the mean and the median return over those events is just above zero.

The results actually look better if we constrain ourselves to the current century. We had four shutdowns so far, with one under Obama in 2013, and three under Trump in 2018. The first two in the first Trump administration lasted only 1 and 2 days, respectively. The Obama shutdown was a more substantial 16 days, and third Trump shutdown stretched 34 days, from just before Christmas 2018 through most of January 2019. All showed positive returns over those periods, with a double-digit bump in the most recent event.

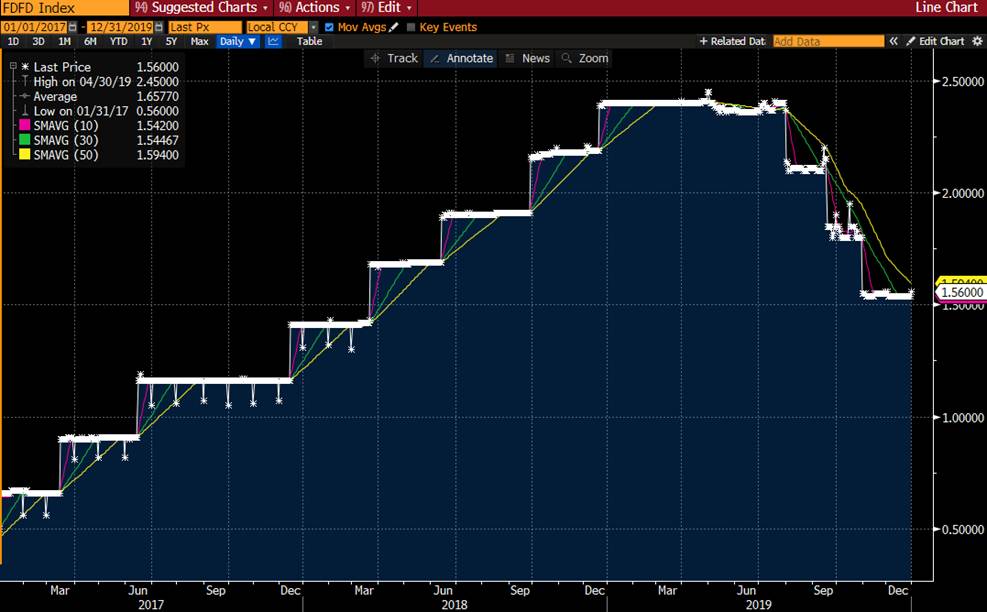

At this point, it is important to remember the nature of markets. If an unpleasant event is widely expected – and government shutdowns are certainly well-reported and widely anticipated – it often results in “sell the rumor, buy the news.” In 2013, the S&P 500 (SPX) was moving sideways to lower as the shutdown loomed. We then saw a modest selloff in the midst of the shutdown, and stocks resumed their upward path afterwards.

Source: Bloomberg

The situation in December 2018 was far different. The Federal Reserve had been raising rates throughout the year, and stocks fell in response. We had “Volmaggedon” in February, recovered to fresh highs in September, and sank 10% again in October. An attempted recovery stalled at the end of November, and stocks began to sink further before the shutdown. The FOMC met on December 19th and raised rates for the final time in that cycle. In hindsight, it is difficult to disentangle how much of the 10.3% rally that occurred during that shutdown was the result of a changing Fed rate cycle, the January effect, and easing governmental tensions. The big bounce only recouped the levels that prevailed during the shutdown, though the rate cutting cycle boosted stocks in the ensuing year.

Source: Bloomberg

It would seem as though the 2013 scenario would be better precedent for the current situation, even if the current political lineup is identical to that of 2018. The earlier example was a relatively low volatility environment with stock prices modestly reflecting the impending news. The 2018-2019 scenario was a high volatility environment coming at the culmination of a difficult year for stock investors. That is hardly the case now. Hence, investors are not necessarily wrong to be relatively sanguine ahead of another government shutdown.

Source: Bloomberg

Source: Bloomberg

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Related Articles

If there is a difference this time it seems to be this;- There is little reason for either side to negotiate. The Republicans will follow the lead of Trump, and he has the attitude that he can do as he pleases without regard to the desires of the Democrats. The Democrats in turn have no reason to think that a deal with the Republicans will mean anything since Trump has shown that he is willing to ignore any congressional authorization from congress. Both sides demand that the other “go first” and both sides have no trust that the other will honor any agreement. The stalemate will only be eased if the public fines the pain too much and forces some resolution. If history is any example, it took quite some time for the public to force an end to the VietNam war.