- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 18, 2022 at 9:00 am

AMC Entertainment (NYSE: AMC) managed to sell new high-yield notes at a price to yield 15%, amid uncertainties over interest-rate hikes, rising economic and geopolitical concerns, as well as industry-specific risks.

AMC, the world’s largest movie theater chain, recently sold US$400 million worth of 12.75%, 5-year senior notes at a price to yield 15% through its subsidiary Odeon Cinemas Group Ltd (OCGL). The company said it intends to use net proceeds from the sale, which is expected to close on or around October 20, to help refinance US$505.6 million of certain of OCGL’s term loans.

Prospective buyers of AMC’s debt likely waxed cautious about the deal, as initial price talk of about 14% was ultimately raised, and the price lowered from around US$95 to US$92 over the course of the offering.

The deal falls against a backdrop of rising pressure in the high-yield corporate bond market, amid the Federal Reserve’s continued efforts to combat stubbornly high levels of inflation with an aggressive monetary policy tightening regime.

At the conclusion to its two-day meeting in September, the Federal Open Market Committee (FOMC) – the policymaking arm of the Federal Reserve – decided to raise the target range for its federal funds rate to 3.0% to 3.25%, and said it anticipates that ongoing increases in the target range will be “appropriate” to returning inflation to its 2% objective.

They appear to have a long way to go to meet that objective after the Consumer Price Index (CPI) registered for September a hotter-than-expected 8.2% year-over-year increase.

To help fight inflation, the central bank effectively increased its policy rate by 75 basis points (bps) for the past three consecutive meetings and foresees rates climbing to a range in the area of 4.25% to 4.50% by December, and perhaps even a bit higher in 2023.

Moreover, the FOMC added that Russia’s war against Ukraine is not only “causing tremendous human and economic hardship”, but it, and related events, “are creating additional upward pressure on inflation and are weighing on global economic activity.”

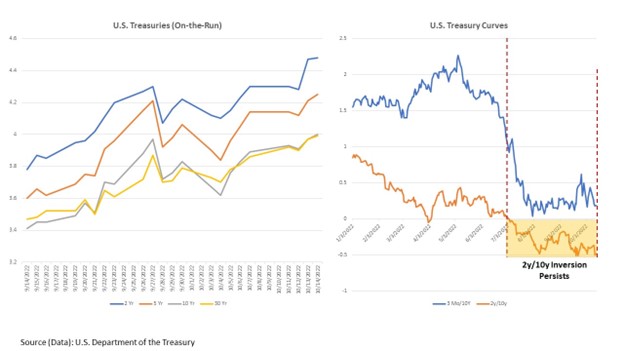

Over the past month to October 14, the yield on the 10-year U.S. Treasury note has risen nearly 60 bps, while an inversion in the 2-year/10-year part of the yield curve has been firmly in place since at least July 6 – a potential sign of a prolonged recession.

Meanwhile, junk bond spreads have been generally widening.

Other AMC bonds, for instance, have cratered in value, including its 7.5% notes due February 15, 2029, which fell almost 7% intraday Monday to US$71.75.

Some market analysts also point to the likelihood that fewer-than-anticipated debt sales will be offered in 2022, amid rising borrowing costs, and as issuers seem to face a fast-closing window for getting deals done.

Oleg Melentyev, Bank of America Merrill Lynch’s head of high yield credit strategy, recently noted, according to Bloomberg, that with “the junk bond primary market practically frozen,

liquidity has deteriorated rapidly in recent weeks”.

By some measures, high yield debt recorded a loss of more than 1.1% for the week-ended October 14, following steady declines in three of the four sessions. The carnage encompassed the spectrum of junk bonds ratings, with ‘CCC’s down over 1.25% to a yield that neared 16% – an increase of almost 75 bps.

Bloomberg further cited that BofA Merrill Lynch, Goldman Sachs, and Citi each lowered their outlooks on high-yield corporate bond issuance in 2022 by US$55 billion, US$100 billion, and US$250 billion, respectively.

Year-to-date, the primary market has suffered a drop of almost 28% year-on-year as of September to US$1.14 trillion, according to data compiled by the Securities Industry and Financial Markets Association (SIFMA).

In the meantime, a host of headwinds have been rattling the cinema ecosystem, including weak content, increasing streaming video on demand (SVoD) competition, and shifting consumer behaviors.

The discount on AMC’s latest debt sale, for example, is likely not merely a reflection of the recent volatility within the financial markets and across the macro landscape, but also an indication of industry-specific issues within the theater exhibition business.

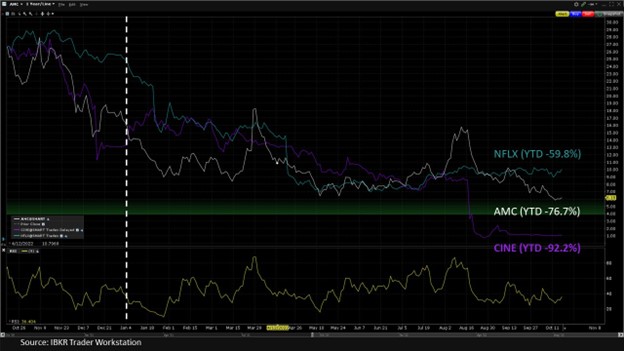

To date in 2022, AMC Entertainment’s stock has fallen roughly 76.7%, Cineworld Group – now undergoing restructuring in bankruptcy – has seen its shares plummet 92.2%, while Netflix has shaved-off almost 60% of its value, as the company navigates intensifying competition, subscriber loss, and likely consumer cutbacks.

IBKR Traders’ Academy – Introduction to U.S. Corporate Bonds

IBKR Podcasts – Episode 20: Inflation, Rates & Recession – What’s the Worst that Could Happen?

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!