- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 18, 2025 at 10:15 am

Central banks face tough decisions amid mixed labor data and inflation risks. US, UK, and Australia show diverging trends, with rate cuts likely in December and ongoing uncertainty for 2026.

US: Small Business Optimism (Oct.): 98.2 – Tepid overall

US: NFIB Higher Prices (Oct.): 21 – Second lowest since 2021

US: NFIB Positions Unable to Fill (Oct.): 32 – Matched lowest since 2020

UK: GDP (Q3, QoQ, prelim.): 0.1% – Below expectations

UK: Unemployment Rate (Sep., 3M average): 5.0% – Higher than expectations

UK: Avg. Earnings Growth (Ex-bonuses; Sep., 3M YoY): 4.6% – Lower than expectations

JP: Goods PPI (Oct., YoY): 2.7% – Price pressures are alive

AU: Unemployment Rate (Oct.):4.3% – Below expectations

AU: Participation Rate (Oct.): 67.0% – Unchanged

The longest US government shutdown on record has finally ended, but it will take some time before the flow of statistical data releases resumes. When it does, it will initially be beset by unusual limitations. For instance, we should get the September employment report soon, but the one that we always said would matter more—the October one—may not be available at all. Or at least, the household survey portion of it, which would hold valuable information about the supply-demand dynamic in the labor market. Ever since the deferred DOGE layoffs in the spring, we penciled in a sizable negative print for October payrolls and an uptick in the unemployment rate. This should have left no doubt about a December Fed cut.

Instead, there are doubts aplenty, especially since the hawkish members of the FOMC (of which several are non-voters this year) have recently been out in force arguing against further cuts. From our vantage point, it feels that we’ve seen this scene not once, but twice before. First in the summer of 2024, when the FOMC turned quite hawkish on the basis of inflation fears before making a U-turn with 100 basis points of cuts on the basis of labor market concerns. The second time was this summer, when tariff/inflation concerns again delayed cuts until September. Given material relief in respect to tariff policy recently (China truce, Switzerland tariff reductions, seemingly imminent tariff reductions on key agricultural goods), one would presume that inflation concerns would be subsiding somewhat. And given the recent spike in private sector layoffs and multiplying headlines about further workforce reductions, one would simultaneously presume that labor market concerns should move up the priority list.

That doesn’t seem to necessarily be the case. Indeed, hawkish messaging from Fed officials drove market pricing for a December cut below 50% as of Friday the 14th. To some extent, it could be argued that a December and a January cut are interchangeable, so the Fed could wait till January. But if they are truly eyeing a January cut, then they might as well deliver it in December and recalibrate 2026 expectations in a more hawkish direction. Then, with three cuts under their belt, FOMC members can enter another extended pause to allow data to clarify the macro picture. This would be our preferred outcome, and we still believe this remains the most likely one. If new data in 2026 emphasize inflation concerns, the FOMC can blame the lack of data for the decision to cut in December. If instead it continues to emphasize labor market concerns, then the cut will be seen as that much more welcome and prescient. Seems like a win-win. Can the Chair convince the committee? We hope so.

Whatever little data is still trickling in is not offering decisive takeaways. But there are repeated reassurance about the lack of inflationary pressures stemming from the labor market, and that should be an important consideration for policymakers.

Weak labor market data and sluggish economic activity have raised the odds of a rate cut in December. Although further data are coming before the BoE’s meeting, the Budget may further limit growth, with labor market softness persisting. In addition, while inflation risks may remain, these must be substantial to change existing forecasts.

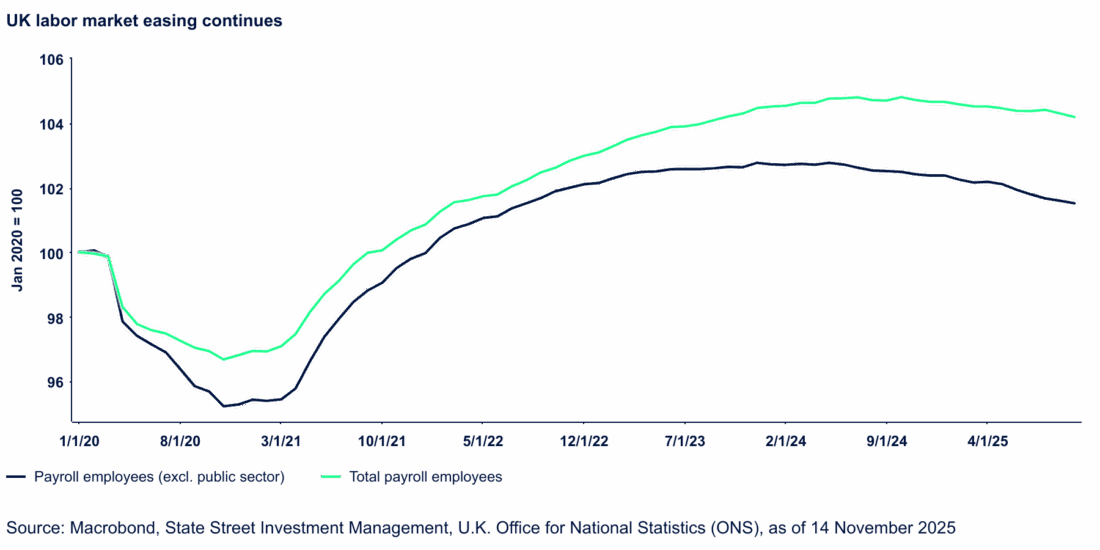

In October, payroll employment declined by 32k, representing the 11th consecutive monthly decrease, reflecting the impact of increases in payroll taxes and the minimum wage. The unemployment rate also rose from 4.8% to 5.0%, though these figures should be interpreted with caution due to uncertainties inherent in the Labor Force Survey.

Labor market weakness is contributing to a slowdown in wage growth. The three-month YoY increase in average earnings including bonuses decreased from 5.0% in August to 4.8% in September, while growth excluding bonuses softened to 4.6%. Regular private sector pay increases moderated to 4.2%, and PAYE median earnings growth fell significantly from 5.9% in September to 3.1% in October.

Economic activity was also below expectations, with GDP expanding by only 0.1% QoQ in Q3, impacted by temporary disruptions in the automotive sector. A recovery is expected for Q4. Domestic final demand increased by 0.5%, largely driven by household and government expenditure. Meanwhile, business investment, inventories, and net trade limited overall growth. Going forward, GDP growth will likely stay modest as earlier stimulus effects fade and further fiscal tightening is expected in the Autumn Budget.

In terms of inflation, we expect that recent declines in food inflation and indications that eurozone supermarket prices may have peaked suggest downside risks for the BoE’s inflation projections.

Regarding fiscal policy, recent media briefings suggest that the Office for Budget Responsibility (OBR) may issue less pronounced forecast downgrades than previously expected, potentially resulting in a fiscal gap of approximately £20 billion or less. It has been reported that the Chancellor does not plan to increase income tax rates and is evaluating measures to enhance fiscal headroom by £5–10 billion, with potential tax changes totaling around £25 billion. While increased fiscal headroom can alleviate short-term fiscal challenges, it is important to assess OBR’s more favorable forecasts with due caution. Currently, we expect that the upcoming tax changes will have a limited effect on inflation and the Bank of England’s interest rate decisions, with the Chancellor likely to refrain from implementing policies that could exacerbate inflationary pressures.

Overall, we continue to expect another rate cut in December, with two further reductions next year, which will bring the policy rate to 3.25% by mid 2026.

The unemployment rate eased back down to 4.3% in October, against our expectations of remaining at 4.5% and consensus’s 4.4%. The step down was supported by a strong 42.2k job additions and participation rate remaining at 67.0% and also rhyme with hours worked rising 0.5% MoM.

The data indicates that the labor market is on a strong footing, despite rising risks that we highlighted here

The data affirms the Reserve Bank of Australia’s (RBA) stance that the labor market remains strong, but we still think that the unemployment rate has some more room to run higher. Youth unemployment rate eased back to 9.6% as their participation rate remained stable, indicating that most of the young people who could not find employment last month could do so this month. We think that the labor market remains at an inflection point and needs more data to form a clearer view. As such, leading indicators point to some more wiggle room for the unemployment rate moving upward.

The consumer sentiment meanwhile showed a surprisingly sharp increase to a four year high in November. The Westpac Consumer Sentiment rose 12.8% MoM, but the recovery was broad based, but a notable exception was the views on labor market, which worsened. Furthermore, the NAB Business Survey showed improvement in conditions to the highest level since March 2024.

All these data developments support the RBA to remain on hold not just in December but for an extended period of time. But we reiterate that labor market developments over the next few months will be crucial and need monitoring.

—

Originally Posted on November 17, 2025 – US rate cut likely despite growing doubts

Do not reproduce or reprint without the written permission of SSGA.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

State Street Global Advisors and its affiliates (“SSGA”) have not taken into consideration the circumstances of any particular investor in producing this material and are not making an investment recommendation or acting in fiduciary capacity in connection with the provision of the information contained herein.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

COPYRIGHT AND OTHER RIGHTS

Other third party content is the intellectual property of the respective third party and all rights are reserved to them. All rights reserved. No organization or individual is permitted to reproduce, distribute or otherwise use the statistics and information in this report without the written agreement of the copyright owners.

Definition:

Arbitrage: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

Fund Objectives:

SPY: The investment seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index. The Trust seeks to achieve its investment objective by holding a portfolio of the common stocks that are included in the index (the “Portfolio”), with the weight of each stock in the Portfolio substantially corresponding to the weight of such stock in the index.

VOO: The investment seeks to track the performance of a benchmark index that measures the investment return of large-capitalization stocks. The fund employs an indexing investment approach designed to track the performance of the Standard & Poor’s 500 Index, a widely recognized benchmark of U.S. stock market performance that is dominated by the stocks of large U.S. companies. The advisor attempts to replicate the target index by investing all, or substantially all, of its assets in the stocks that make up the index, holding each stock in approximately the same proportion as its weighting in the index.

IVV: The investment seeks to track the investment results of the S&P 500 (the “underlying index”), which measures the performance of the large-capitalization sector of the U.S. equity market. The fund generally invests at least 90% of its assets in securities of the underlying index and in depositary receipts representing securities of the underlying index. It may invest the remainder of its assets in certain futures, options and swap contracts, cash and cash equivalents, as well as in securities not included in the underlying index, but which the advisor believes will help the fund track the underlying index.

The funds presented herein have different investment objectives, costs and expenses. Each fund is managed by a different investment firm, and the performance of each fund will necessarily depend on the ability of their respective managers to select portfolio investments. These differences, among others, may result in significant disparity in the funds’ portfolio assets and performance. For further information on the funds, please review their respective prospectuses.

Entity Disclosures:

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

SSGA Funds Management, Inc. serves as the investment advisor to the SPDR ETFs that are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. SSGA Funds Management, Inc. is an affiliate of State Street Global Advisors Limited.

Intellectual Property Disclosures:

Standard & Poor’s®, S&P® and SPDR® are registered trademarks of Standard & Poor’s® Financial Services LLC (S&P); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by S&P Dow Jones Indices LLC (SPDJI) and sublicensed for certain purposes by State Street Corporation. State Street Corporation’s financial products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and third party licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability in relation thereto, including for any errors, omissions, or interruptions of any index.

BLOOMBERG®, a trademark and service mark of Bloomberg Finance, L.P. and its affiliates, and BARCLAYS®, a trademark and service mark of Barclays Bank Plc., have each been licensed for use in connection with the listing and trading of the SPDR Bloomberg Barclays ETFs.

Distributor: State Street Global Advisors Funds Distributors, LLC, member FINRA, SIPC, an indirect wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. Certain State Street affiliates provide services and receive fees from the SPDR ETFs.

ALPS Distributors, Inc., member FINRA, is distributor for SPDR® S&P 500®, SPDR® S&P MidCap 400® and SPDR® Dow Jones Industrial Average, all unit investment trusts. ALPS Distributors, Inc. is not affiliated with State Street Global Advisors Funds Distributors, LLC.

Before investing, consider the funds’ investment objectives, risks, charges, and expenses. For SPDR funds, you may obtain a prospectus or summary prospectus containing this and other information by calling 1‐866‐787‐2257 or visiting www.spdrs.com. Please read the prospectus carefully before investing.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from State Street Global Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!