- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 11, 2026 at 12:40 pm

Oil has risen as expected, but the disruption is now spreading from transport bottlenecks in the Strait of Hormuz to energy production itself, reinforcing broader risk off dynamics ahead of any material improvement on the battlefield.

Our forecast last week assumed oil prices would remain below $100 provided production was not directly affected. That condition has now been breached, with Saudi and Bahraini refineries hit alongside Qatar’s gas liquefaction facility.

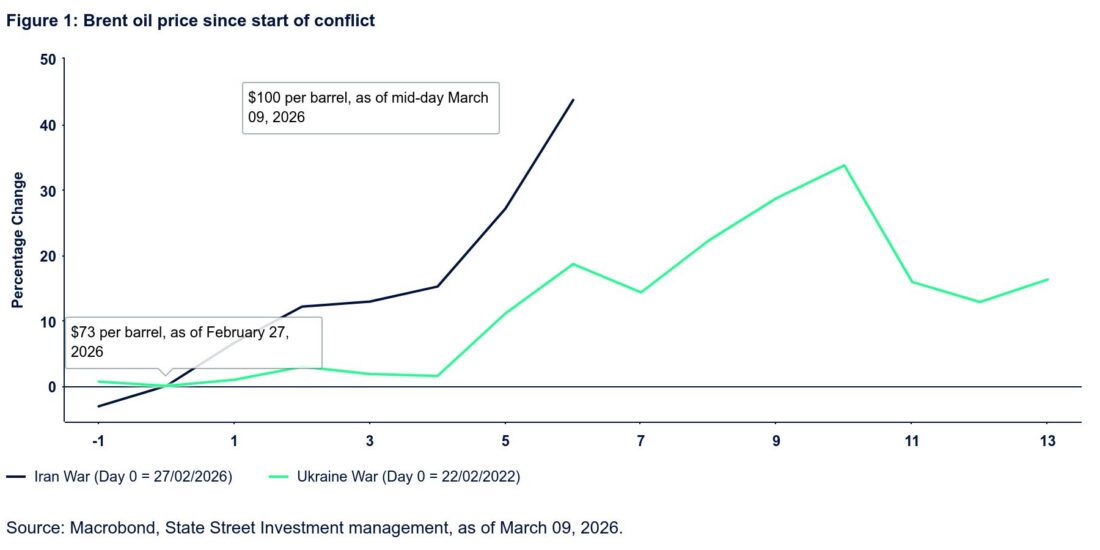

Brent was trading at around $100 per barrel as of 9 March, having briefly peaked at nearly $120. Figure 1 shows the percent change in the Brent oil price, following the outbreak of war in Ukraine in 2022 compared with what we are seeing today.

Four years ago, oil peaked at $130 and stayed above $100 for four months before gradually normalising by early 2023. Given market conditions being different, a rebased view here (not the USD price!) is helpful, showing a 35% jump thus far. Unsurprisingly, the pace has been faster, as the 2022 conflict touched 10% of global production, whereas the Gulf is home to close to 30%.

We are now closer to the equilibrium price for a regional conflict, with next leg up requiring further escalation or signs that Hormuz will remain shut for more than 2-3 weeks. Current levels of shipping trigger cascading problems after about two weeks of closure. That is when producers can no longer divert newly produced oil to either seaborne or onshore storage and then have to ‘shut in’ production.

To avoid shut-ins, producers will start throttling production in advance to buy more time. Iraq has already begun to do that—cutting production by 3mbd (about 75% of its daily output) in the hope that it can maintain production until transport reopens. Iraq is a special case with much lower storage capacity than other producers. However, the UAE and Kuwait have over the weekend announced that they are trimming production as well, in order to cope with a longer closure period of the Hormuz Strait.

Figure 2 shows the one major positive development in the rapid decline in Iranian ballistic missile launches, though drone warfare remains relatively stable with over 100 daily drones directed at the UAE alone. For comparison, Russia shot an average of 156 Iranian-made Shahed drones every day at Ukraine for all of 2025—i.e., 57,000 in total. Iran’s estimated drone supplies are 30%-40% of that. Moreover, Russia launched from fixed installations unimpeded. Iran also relies on more skilled manpower for launches that cannot be easily replaced. Nonetheless, that still leaves Iran with the ability to launch 50-100 drones strikes daily for several weeks, impeding the return of full normality in the Gulf. Other developments at the political and economic levels are also suggesting near-term deterioration.

Week 2 assessment

| Positive(a faster end to the conflict and a more favorable outcome for risk assets) | Negative (a more prolonged conflict and a more negative backdrop for risk asse |

| Daily number of ballistic missiles declinedIncreased reliance on drones and cluster munitions | Hormuz traffic down 95%Qatar LNG (20% of global LNG production) paused for weeksIraq reduced output by 3mbd (75% of daily production); UAE and Kuwait following suit |

| Gulf air defenses largely perform well, preventing mass casualties, but there are concerns about remaining stockpiles | Hormuz outage also material for non-energy exports, notably sulfur (45% of global production), fertilizers (10%) and aluminum (10%) |

| Increased share of Israel’s targets directed at Iran’s internal repressive apparatus | Mojtaba Khamenei replacing his father shows Tehran digging in for longer conflict |

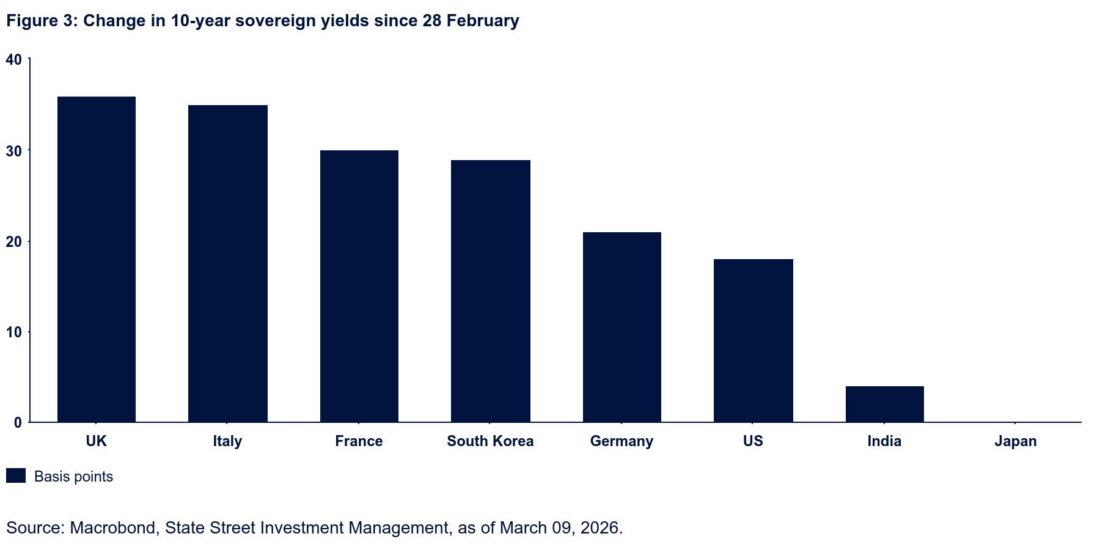

This is a classic stagflationary supply shock for energy importers, which will again require a fiscal counter-response. Using Bloomberg’s SHOK model, a $50 increase in oil prices (i.e. around $115) in one quarter would equate to nearly a 1% increase in US CPI over the following three quarters. Bond markets have sharply adjusted to this inflation dynamic for weaker European sovereigns, and to a lesser extent, for the US and Germany as well.

Notably, in 2022, bond yields did not rise until the third week of the war when the magnitude of Ukraine support and European rearmament costs came into vision. If the current crisis persists, we would assume upward pressure on bond yields to continue. Similarly, we would forecast continued USD strength to be maintained as a corollary of America’s energy profile. Both trends are vulnerable to a sharp reversal upon de-escalatory news.

Iran’s success in maintaining sufficient firepower into the Gulf means the war is now morphing into a negative global macro shock (supportive for the USD, gold, and commodities; negative for bonds and equities). That said, it is difficult to envisage the duration of this shock exceeding one to two months. Even in a more prolonged conflict, a partial normalization of oil prices would be likely.

For more such insights, please visit.

—

Originally Posted on March 10, 2026 – The Gulf shock: Energy supply, markets, and macro spillovers

Do not reproduce or reprint without the written permission of SSGA.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

State Street Global Advisors and its affiliates (“SSGA”) have not taken into consideration the circumstances of any particular investor in producing this material and are not making an investment recommendation or acting in fiduciary capacity in connection with the provision of the information contained herein.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

COPYRIGHT AND OTHER RIGHTS

Other third party content is the intellectual property of the respective third party and all rights are reserved to them. All rights reserved. No organization or individual is permitted to reproduce, distribute or otherwise use the statistics and information in this report without the written agreement of the copyright owners.

Definition:

Arbitrage: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

Fund Objectives:

SPY: The investment seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index. The Trust seeks to achieve its investment objective by holding a portfolio of the common stocks that are included in the index (the “Portfolio”), with the weight of each stock in the Portfolio substantially corresponding to the weight of such stock in the index.

VOO: The investment seeks to track the performance of a benchmark index that measures the investment return of large-capitalization stocks. The fund employs an indexing investment approach designed to track the performance of the Standard & Poor’s 500 Index, a widely recognized benchmark of U.S. stock market performance that is dominated by the stocks of large U.S. companies. The advisor attempts to replicate the target index by investing all, or substantially all, of its assets in the stocks that make up the index, holding each stock in approximately the same proportion as its weighting in the index.

IVV: The investment seeks to track the investment results of the S&P 500 (the “underlying index”), which measures the performance of the large-capitalization sector of the U.S. equity market. The fund generally invests at least 90% of its assets in securities of the underlying index and in depositary receipts representing securities of the underlying index. It may invest the remainder of its assets in certain futures, options and swap contracts, cash and cash equivalents, as well as in securities not included in the underlying index, but which the advisor believes will help the fund track the underlying index.

The funds presented herein have different investment objectives, costs and expenses. Each fund is managed by a different investment firm, and the performance of each fund will necessarily depend on the ability of their respective managers to select portfolio investments. These differences, among others, may result in significant disparity in the funds’ portfolio assets and performance. For further information on the funds, please review their respective prospectuses.

Entity Disclosures:

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

SSGA Funds Management, Inc. serves as the investment advisor to the SPDR ETFs that are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. SSGA Funds Management, Inc. is an affiliate of State Street Global Advisors Limited.

Intellectual Property Disclosures:

Standard & Poor’s®, S&P® and SPDR® are registered trademarks of Standard & Poor’s® Financial Services LLC (S&P); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by S&P Dow Jones Indices LLC (SPDJI) and sublicensed for certain purposes by State Street Corporation. State Street Corporation’s financial products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and third party licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability in relation thereto, including for any errors, omissions, or interruptions of any index.

BLOOMBERG®, a trademark and service mark of Bloomberg Finance, L.P. and its affiliates, and BARCLAYS®, a trademark and service mark of Barclays Bank Plc., have each been licensed for use in connection with the listing and trading of the SPDR Bloomberg Barclays ETFs.

Distributor: State Street Global Advisors Funds Distributors, LLC, member FINRA, SIPC, an indirect wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. Certain State Street affiliates provide services and receive fees from the SPDR ETFs.

ALPS Distributors, Inc., member FINRA, is distributor for SPDR® S&P 500®, SPDR® S&P MidCap 400® and SPDR® Dow Jones Industrial Average, all unit investment trusts. ALPS Distributors, Inc. is not affiliated with State Street Global Advisors Funds Distributors, LLC.

Before investing, consider the funds’ investment objectives, risks, charges, and expenses. For SPDR funds, you may obtain a prospectus or summary prospectus containing this and other information by calling 1‐866‐787‐2257 or visiting www.spdrs.com. Please read the prospectus carefully before investing.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from State Street Global Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!