- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 8, 2026 at 1:30 pm

They’re back. Tomorrow morning, we get the release of the December employment report on their normal schedule. Monthly jobs data typically arrive on the first Friday of the following month, but considering that last Friday followed New Year’s Day, this is indeed typical. It’s nice to get back to a regular schedule after the shutdown-induced hiatus. Let’s see how options markets are pricing in the likely reaction to the report.

Economists are predicting tepid data. According to Bloomberg data, consensus estimates for Nonfarm Payrolls and the Unemployment Rate are 70,000 (up from 64,000) and 4.5% (down from 4.6%), respectively. Both of these would of course be slight improvements over the prior month, but hardly sufficient to declare victory on the “maximum employment” portion of the Fed’s dual mandate. The IBKR ForecastTrader broadly agrees with those assessments, with a 51% “Yes” for Nonfarm Payrolls above 50,000 and a 45% “Yes” for an Unemployment Rate above 4.5%.

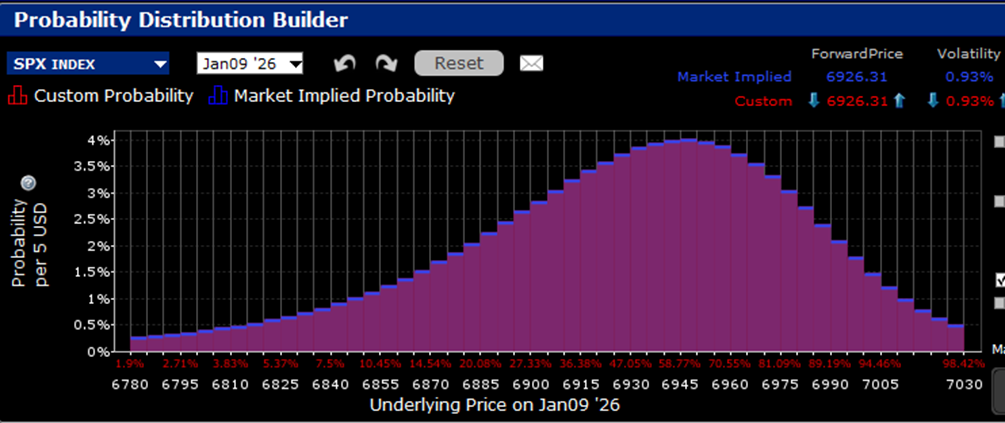

Coming into the report on the heels of an up week through Thursday morning, options traders are generally sanguine about its outcome. The IBKR Probability Lab is showing its now usual upside bias for S&P 500 (SPX) options expiring tomorrow, with a peak probability in the 6945-6950 range, about 0.3% above the current index level.

IBKR Probability Lab for SPX Options Expiring January 9, 2026

Source: Interactive Brokers

We have frequently noted short-term SPX options’ tendency to price in an index bump, most recently when we pointed out how a “Santa Claus Rally” was being priced into year-end expirations. We asserted at the time that:

It has become customary to see traders assign higher probabilities to above-market outcomes for the S&P 500 (SPX). We have posited that it might represent “FOMO insurance”, where skeptical or underinvested institutional investors utilize upside calls to hedge their risk of underperformance. Of course, it could simply be that after a three-year bull market traders simply expect that the market is more likely to rise than fall on any given day and over any given period. I suspect that both factors are at work.

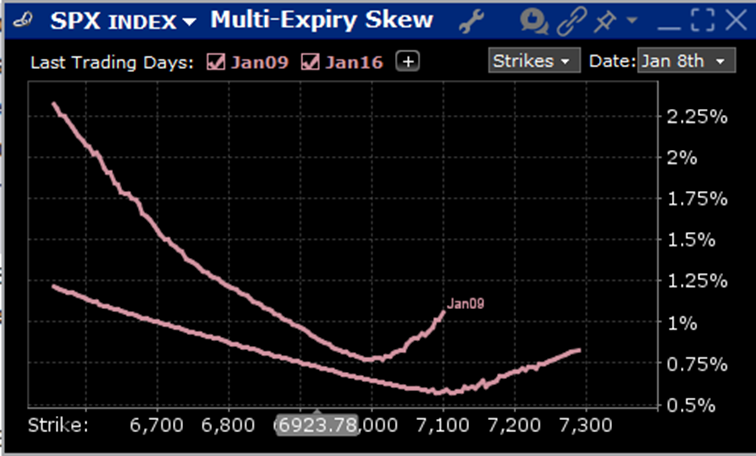

Thus, even with the distinct possibility that a disappointing report could upset the market’s mood, options traders’ relatively complacent mood extends to the relatively modest bump to implied volatilities on near-term, at-money options. We see an at-money implied daily volatility of 0.93%, only a modest bump from next week’s 0.78%. However, the relatively steep skew on tomorrow’s options does indicate at least a fair amount of risk aversion.

Skews for SPX Options Expiring January 9th (top) and 16th, 2026 (bottom)

Source: Interactive Brokers

A relatively complacent options market implies that there is a bit of room for surprises. Rate cut probabilities for the FOMC meeting on January 28th remain quite low, about 12% according to both the CME FedWatch and ForecastEx. A significant negative surprise would likely be required for a dramatic improvement in those odds, but that would then bring up the notion of “careful what you wish for.” Thus, if anything remotely in line is unlikely to sway the Fed, it is understandable why traders might be willing to overlook the risks in tomorrow’s report. We’ll know tomorrow if it sways the institutional mindset that has supported stocks in the past few days.

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!