- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Latest Webinars

Posted August 20, 2025 at 10:45 am

July CPI, PPI, and Retail Sales are in the rearview mirror, and investors now look ahead to a trio of key potential macro volatility catalysts this week.

According to our Economic Calendar, with data licensed from Econoday Inc., minutes from the Federal Reserve’s July 29-30 meeting cross the wires at 2 p.m. ET today, August 20th. It doesn’t always move stocks and bonds, but last month’s FOMC gathering (which resulted in no change to the policy rate) was the first in 32 years to feature two dissenters. What’s more, former Fed governor Adriana Kugler did not cast a vote in the 9-2 decision.1

Today’s minutes could include nuggets from Governor Chris Waller, seen as a leading contender to succeed Chair Powell. His dovish stance, calling for an immediate interest rate cut, was said to be vindicated by some Fed watchers in the wake of the July nonfarm payrolls report that came in much weaker than expected. After last week’s CPI data was absorbed, investors largely shifted from hoping for a resumption in Fed easing to expecting easing, and that has key impacts for both stock prices and capital markets activity. More on that to come.

Thursday’s data slate is busy. Our Economic Calendar shows that weekly jobless claims hit the tape in the premarket, along with the Philadelphia Federal Reserve’s Manufacturing Index. Initial and Continuing claims are “hard” data, while the Philly Fed gauge is “soft” survey data—both help investors suss out signal from noise. But what could be more market-moving is the S&P Global Manufacturing and Services Purchasing Managers Index (PMI) readings.

This is a first look at August PMIs, and they come amid record-high stock prices but also steeper tariff rates. The latter could be more impactful to business executives as they navigate what’s now an 18.6% US effective tariff rate, according to The Budget Lab from Yale University.2 Keep in mind that we don’t get the Institute for Supply Management’s (ISM) version of the PMIs until early September.

We buried the lead. This week is all about Fed Chair Powell’s speech in the shadows of the mountains of the Grand Teton National Park. Yes, it’s Jackson Hole time. Finance data junkies and macro mavens will parse Powell’s missive, and this one could be a dovish pivot from his more balanced press conference back on July 30.

While below last week’s peak, the odds of a September rate cut are elevated at 85%.3 Assuming the outgoing Fed chief is in line with bond traders, Friday morning’s speech should open the door to the FOMC’s first quarter-point ease of the year. The inflation backdrop is still concerning–look no further than the July PPI data–so Powell may avoid offering direct rate-cut signals.

Powell’s speech on the economic outlook is scheduled for 10 a.m. ET on August 22nd.4 Recall it was three years ago when he warned Americans that a period of “pain” was in store as the Fed combatted what had been a 40-year high in CPI inflation.5 Stocks plunged even before his eight-minute address finished, ultimately leading to a bear-market bottom in the S&P 500 two months later.

The vibes are different today. The S&P 500 has returned 60%, dividends included, since Jackson Hole three years ago.6 While it’s true that investors remain skeptical, they are also a lot wealthier, thanks to the AI-fueled bull market and record-high corporate earnings.

Yes, we’ve come a long way, but what does the future hold? Nobody knows, but we can make some educated guesses based on monetary policy’s path.

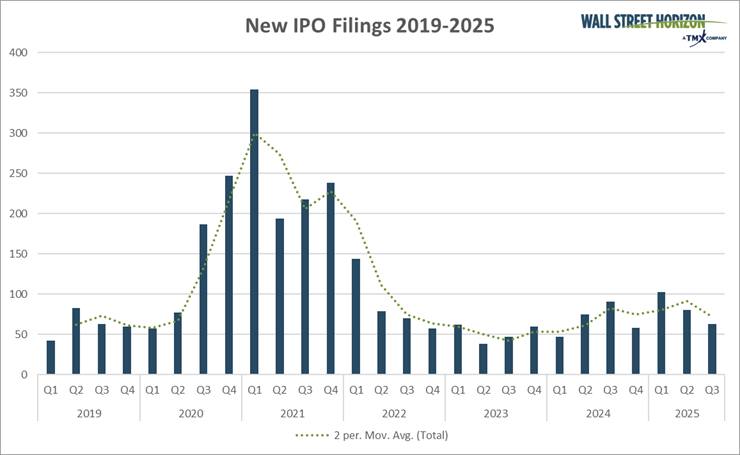

First, according to our IPO data, licensed from IPOScoop, the IPO market is booming—even during what’s often a slow summer for equity unlocks. It’s possible that a pickup in go-public activity sparks after Labor Day, and names like SpaceX, OpenAI, and Anthropic could land on the NYSE or Nasdaq before long.

Elsewhere, StubHub may IPO under the ticker STUB this quarter after its early-year delay. And rumors now swirl that Fannie Mae and Freddie Mac could relaunch as IPOs. A trend lower in borrowing costs (so long as economic growth hangs in there) would be a tailwind.

Source: IPOScoop via Wall Street Horizon

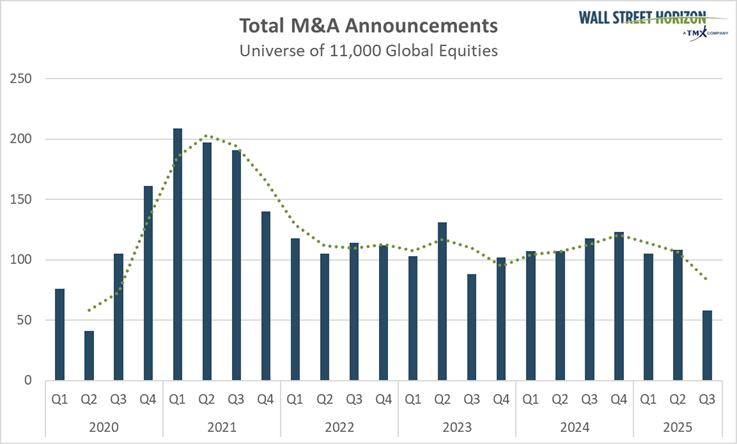

Cheaper interest rates might also fuel the M&A arena, which has had a decent summer but has not captured the awe of investors like 2025’s IPO winners. Equity or cash financing is, of course, an option for today’s large-cap companies that boast strong balance sheets and lofty stock prices. Additionally, modest Treasury rates and tight credit spreads are conducive to deals inked with debt.

The upshot? Bankers could be busy when they get back from August holiday.

Source: Wall Street Horizon

Multinational corporations might simply decide to tap capital markets for debt and equity to invest in long-term projects. The One Big, Beautiful Bill Act’s (OBBBA) full-expensing provision incentivizes companies to boost their capex, which bodes well for US GDP growth over the balance of the year and beyond.

There’s no free lunch, though, and a sudden adrenaline rush from capital investment may stoke inflation. So, it all comes back to Fed policy.

Jay (Powell) is the focus this week, but Jensen (Huang) takes center stage next Wednesday night when NVIDIA (NVDA) reports Q2 results. Shares may swing significantly after the earnings print…and before it.

On the conference front, NVIDIA, Microsoft (MSFT), Alphabet (GOOGL), Meta Platforms (META), and Broadcom (AVGO) are slated to present at the Hot Chips 2025 conference in Palo Alto, CA, from August 24 to 26; tech investors should be on watch for potential volatility early next prior to the NVIDIA release.

There’s plenty of macro data on tap over this week’s final three trading days, culminating with Powell’s annual address from the Federal Reserve Bank of Kansas City’s Jackson Hole Economic Symposium. The prospect of lower interest rates has reinvigorated the stock market lately, but the next move may hinge on what Jay delivers.

—

Originally Posted August 20, 2025 – Jackson Hole and Other Macro Data On Tap: Key Takeaways for Investors

1 Trump says he will pick a ‘temp’ replacement for Fed’s Kugler in days, Reuters, Andrea Shalal, Jeff Mason, August 6, 2025, https://www.reuters.com

2 State of U.S. Tariffs: August 7, 2025, The Budget Lab, August 7, 2025, https://budgetlab.yale.edu

3 FedWatch, CME Group, August 19, 2025, https://www.cmegroup.com

4 Calendar, The Federal Reserve, August 19, 2025, https://www.federalreserve.gov/

5 Powell warns of ‘some pain’ ahead as the Fed fights to bring down inflation, CNBC, Jeff Cox, August 26, 2022, https://www.cnbc.com

6 SPXTR, StockCharts, August 19, 2025, https://schrts.co

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!